Harsh Batra

Harsh Batra

Hello,

This week, Blackstone led a $1 billion financing for Neysa, backing one of India’s most significant AI-infrastructure platforms and sending a strong signal for private capital moving into computers.

But it was not the only deal that stood out this week:

- At the same time, Adani Group outlined plans to invest $100 billion in AI data centres by 2035, a staggering capex ambition that reframes India’s AI race and possible long term infrastructure demand.

- Meanwhile, RBI’s new capital market exposure norms could revive bank-led acquisition financing, with implications for leveraged buyouts as much as sponsor-backed deals.

- In public markets, Fractal Analytics shares fell on debut after its $313 million IPO. reinforcing the narrative of fragile pricing power in public markets and tougher exit conditions.

- And finally, Yotta Data Services committed $2 billion to deploy Nvidia’s latest chips, underscoring both India’s AI arms-race dynamic and the capital intensity now embedded in the ecosystem.

I hope you enjoy this week’s roundup. And if you’re looking to take your M&A deals to the next level, connect with me on LinkedIn to discuss how Ideals VDR can help with your next strategy.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

Big Debt

Source: Press Information Bureau, Government of India

Over the past decade, India has built up substantial government debt as a strategy. The question now is whether that debt remains sustainable.

India’s total general debt, including both internal and external obligations, has remained broadly stable around 80-82% of GDP in recent years. The majority is domestically held, rupee-denominated and long-term in nature, which significantly limits FX risks and rollover pressure.

- Although this level may appear elevated, it remains broadly in line with advanced economies such as Austria (82.4%) and China (94.1%), and even below some smaller economies including Bolivia (90.4%) or Bhutan (105.6%).

External debt remains far smaller in relative terms. India’s external debt has been around 19-20% of GDP (about $765 billion in recent prints), a manageable ratio by emerging-market standards.

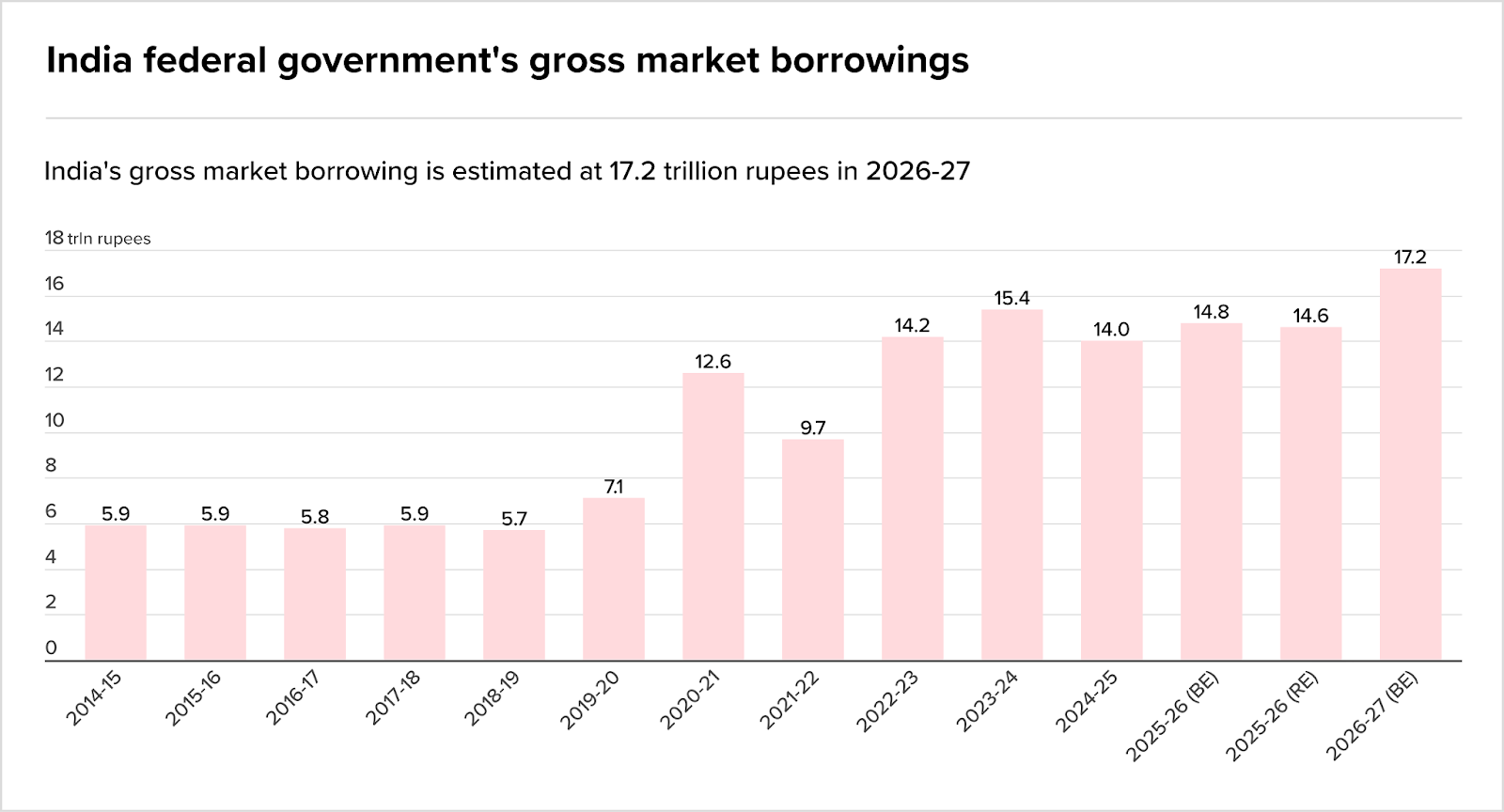

Caption: India’s central government‘s gross market borrowings

Source: Reuters

The 2026-27 Union Budget projects record gross borrowing of ₹17.2 trillion (about $207 billion; @1 USD = ₹83). That borrowing funds both capital expenditure (asset-building) and revenue expenditure (day-to-day spending that does not directly create future productive capacity).

Borrowing, by itself, is not necessarily the problem. What matters is the trajectory: a record gross number can still be consistent with a stable (or falling) debt ratio if nominal GDP growth remains strong and the fiscal deficit continues to narrow.

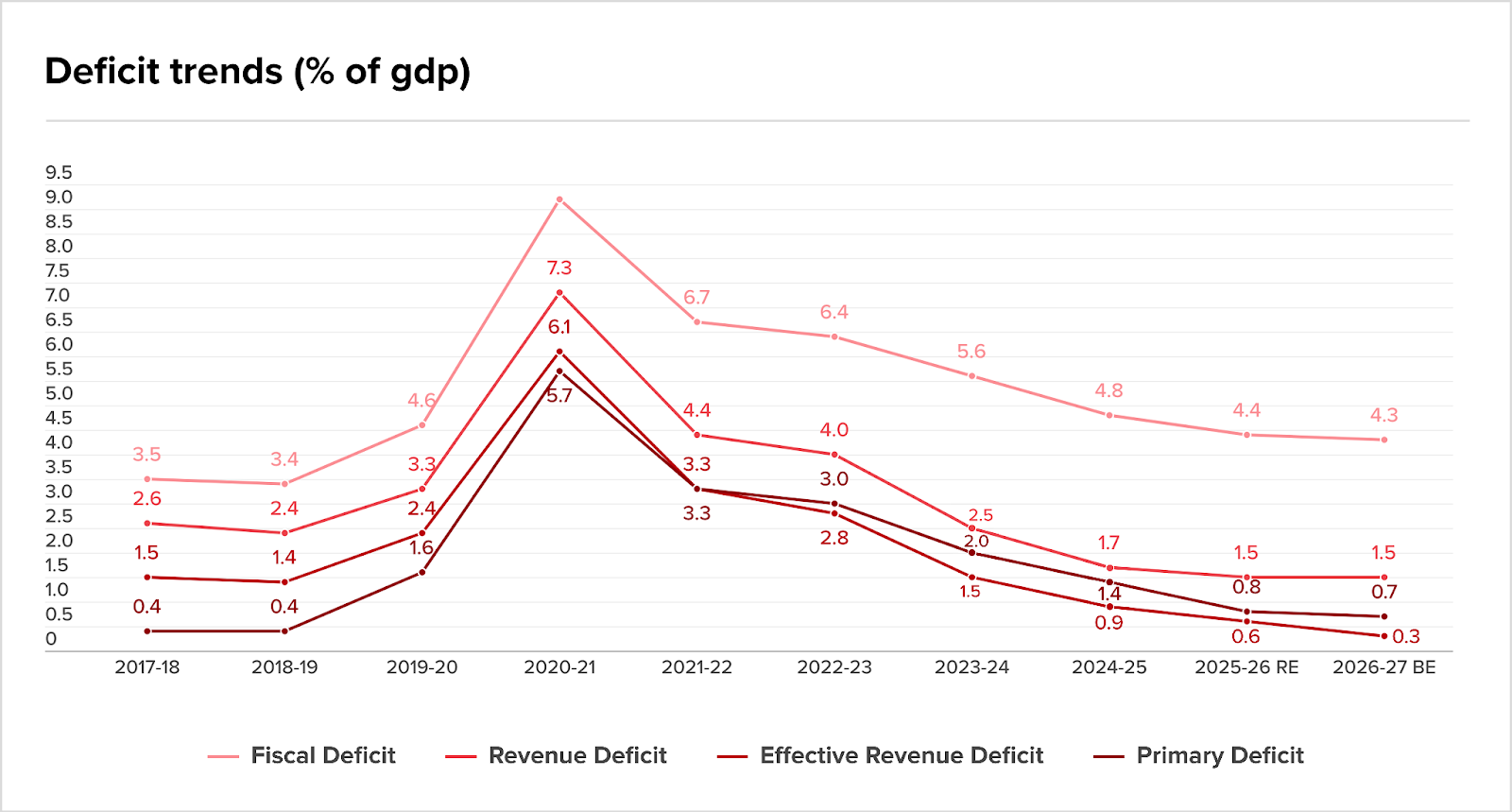

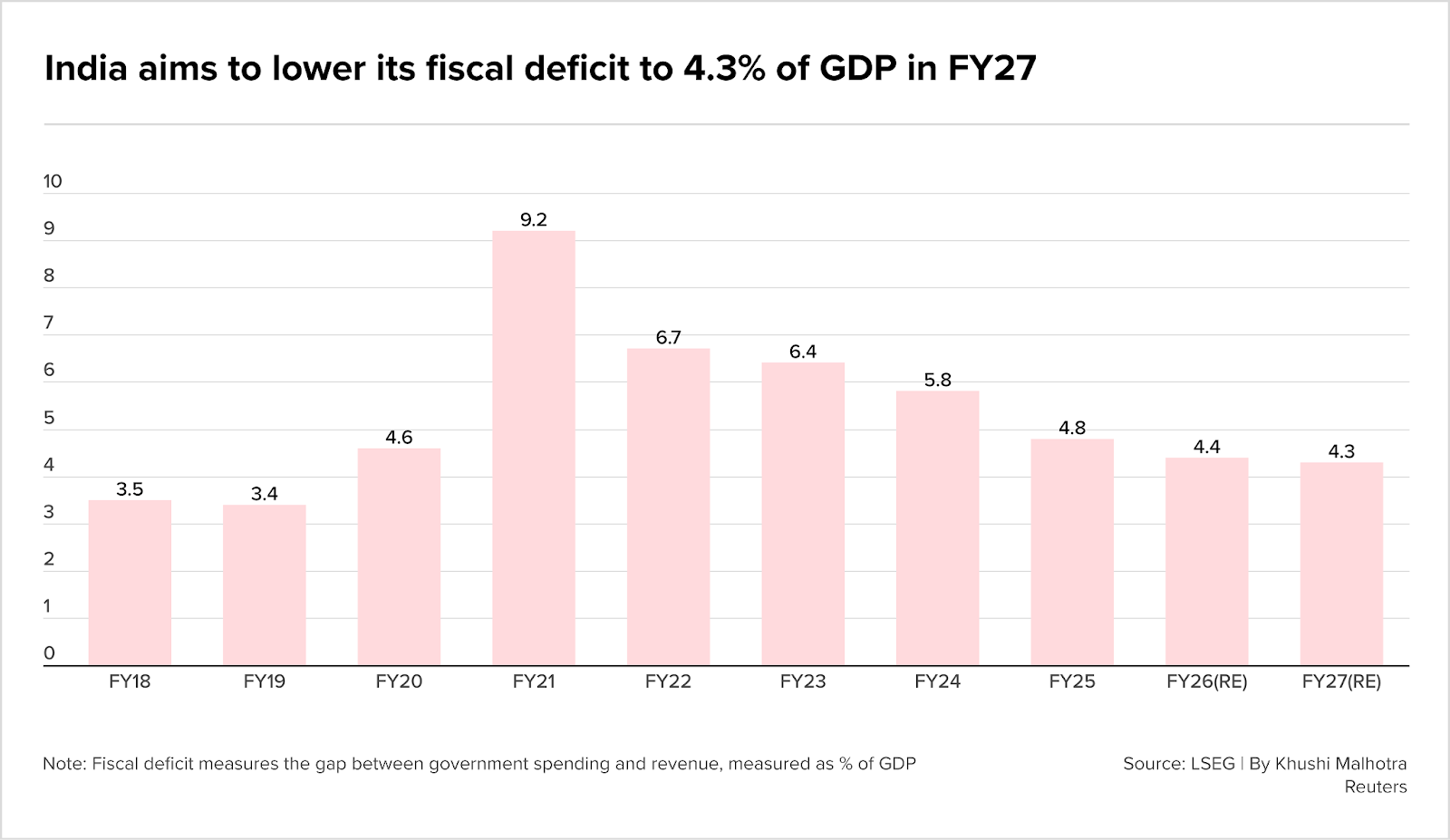

Add caption: Fiscal deficit glide path to 4.3%

The government aims to reduce the fiscal deficit to 4.3% of GDP by FY27. In plain terms: for every GDP is ₹100, it plans to borrow ₹4.30 that year. That gradual narrowing economists call ‘fiscal consolidation’ is designed to stabilise the debt ratio.

This sustainability will hinge on three variables: nominal GDP growth, interest costs, and inflation. If nominal growth exceeds the effective interest rate on government debt, the debt burden will gradually ease.

India’s growth outlook remains stronger than most major economies, and inflation has stayed broadly within the RBI’s comfort zone. Still, interest payments already absorb a significant share of government revenue — a constraint markets watch closely.

The big picture of Big Debt in India is that it is not in crisis, but fiscal headroom is no longer unlimited. For dealmakers, the signal lies in yields, liquidity conditions, and whether sovereign borrowing crowds out private capital — or catalyses it through sustained public capex.

India’s inflation remains within the monetary policy committee targets, keeping borrowing costs manageable, as RBI governor Sanjay Malhotra said.

- “We are certainly in the same sweet spot, maybe even better because growth is looking up. Growth is looking even better and inflation is the same.”

The rumour mill

- Adani plans to invest $100 billion in AI data centers by 2035

- Alkem Labs unit to buy up 55% of Occlutech or $118m

- Blackstone leads $600 million raise in AI cloud startup Neysa at $1.4 billion valuation

- CTUIL-Grid India merger back on Centre’s agenda to revamp transmission sector

- Global private equity firms bowled over by Indian cricket league IPL

- India competition watchdog approves acquisition of Axis Securities’s portfolio management services Biz by Axis Asset Management

- India’s Inflexor Ventures eyes first close of Fund III soon, existing LPs likely to re-up

- Reliance Industries buys 3 apartments at One Altamount Road for ₹85 crore

- Yuan poised to extend surge againstINR, analysts-say

- Fountainvest, EMS call off deal for Eurogroup Laminations stake due to India compliance issue

M&A news

- RBI grants approval to Bain Capital for acquiring up to 41.7% stake in Manappuram Finance

- Automation In India Is As Much A Social Challenge As An Engineering, Says Dassault Systèmes’ Manish Kumar

- D-Street’s new-age firms strike a profit note

- India deal values fall 60% in Jan 2026 to $7.2 bn as big-ticket M&A stalls

- Buyouts gain ground as private equity firms take control in India

- Merger involving $61 billion of debt to help India Credit Market

- Outbound M&A by India Inc will sustain, says Citi’s Rahul Saraf

- SoftBank’s India exits tell one story. The numbers beneath tell another

- Banks to drive domestic M&A as RBI eases financing norms

Job moves

IPOs

- Amagi Media trims IPO size, targets $869 million post-money valuation to woo investors

- Fractal shares fall in Mumbai debut after $313 million India IPO

- Software selloff is disrupting some M&A and IPO deals, US bankers say

- Why new-age IPOs are seeing shrinking issue sizes, slashed valuations

- Will PhonePe’s IPO trigger a rerating for Paytm shares?

Fundraising

- Affirma taps local limited partners

- C2i semiconductors raises $15m Series A led by PeakXV Partners

- Pravega Ventures leads Otto Money pre-seed round. The company raised $1.3 million

- Digital identity firm IDfy raises $53m from Neo Asset, others

- Former TPG exec’s VC firm Arc180 gets LP for fund to back Indian-origin founders

- India doubles down on state-backed venture capital approving 1.1b fund

- Kotak Yield Growth Fund secures $430m in first close

- Morgan Stanley Asia PE plans continuation fund to pave way for next raise

- Motilal Oswal Alternates raises Rs 8,500 cr for fifth PE fund

- W Health-ventures raises $61m in initial cloaw of Fund II

Compliance/regulatory update

- A review of key developments in India’s merger control regime: 2024 – 2025

- Brokers flag liquidity risks in RBI’s new credit curbs on capital market intermediaries, likely to make representation to regulators

- Delhi Tribunal denies treaty exemption to a Singapore company on sale of grandfathered shares; reiterates substance test

- India central bank allows lenders to fund up to 75% in M&A deals

- India curbs loans extended to brokers in blow to trading volumes

- India’s forex reserves drop $6.7 billion to $717 billion, gold reserves dip, reveals RBI data

- S&P global CEO: India’s post-covid expansion among most consistent for any major economy

- Union Budget 2026-27: Infrastructure-led growth to strengthen real estate sector outlook

- What explains the spike in bond yields despite 125 bps in RBI repo rate cuts

- Zerodha CEO Nithin Kamath explains how RBI’s new lending norms for brokers impact stock market investors