Sebastian Montoya

Sebastian Montoya

The first week of February has a very clear theme — storage and hybrids.

Solar and wind shared the lead on volume, while BESS kept showing up as a key ingredient across Europe’s deals.

We zoom in on European solar M&A in 2026 to look at the factors that are actually moving terms and valuation: softer PPA pricing, capture-price pressure, and why storage-backed structures are quietly becoming the new shorthand for bankability.

This week’s key highlights include:

- Ørsted agreed to sell its entire European onshore wind, solar and BESS business to Copenhagen Infrastructure Partners for €1.44bn, sharpening the strategic divide between “platform builders” and “portfolio shufflers”.

- Brookfield launched the sale of renewables developer X‑Elio at an estimated €4bn valuation, putting a sizeable multi-country platform (with storage exposure) back into play.

- Zenobē entered Germany’s battery storage market by acquiring 1.3 GW / 2.5 GWh of operational and under-construction BESS assets.

Want more insight? Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

European Solar M&A 2026: When MW stop being the whole story

If 2025 taught dealmakers anything, it’s that a market can look greener by deal value than by deal count.

Globally, a S&P report points to a growth in transactions, helped by large deals and sponsors willing to underwrite scale. In European power markets, solar kept growing. But the marginal value of solar output kept getting squeezed.

European solar M&A in 2026 is less about buying MW and more about revenue quality: capture value, contracting route, and flexibility.

2025 in numbers: M&A value rebounds as solar value compresses

Global deal value improved meaningfully on value. The punchline is not that everyone suddenly fell back in love with risk, it’s that big transactions did a lot of the heavy lifting, while broader activity stayed selective.

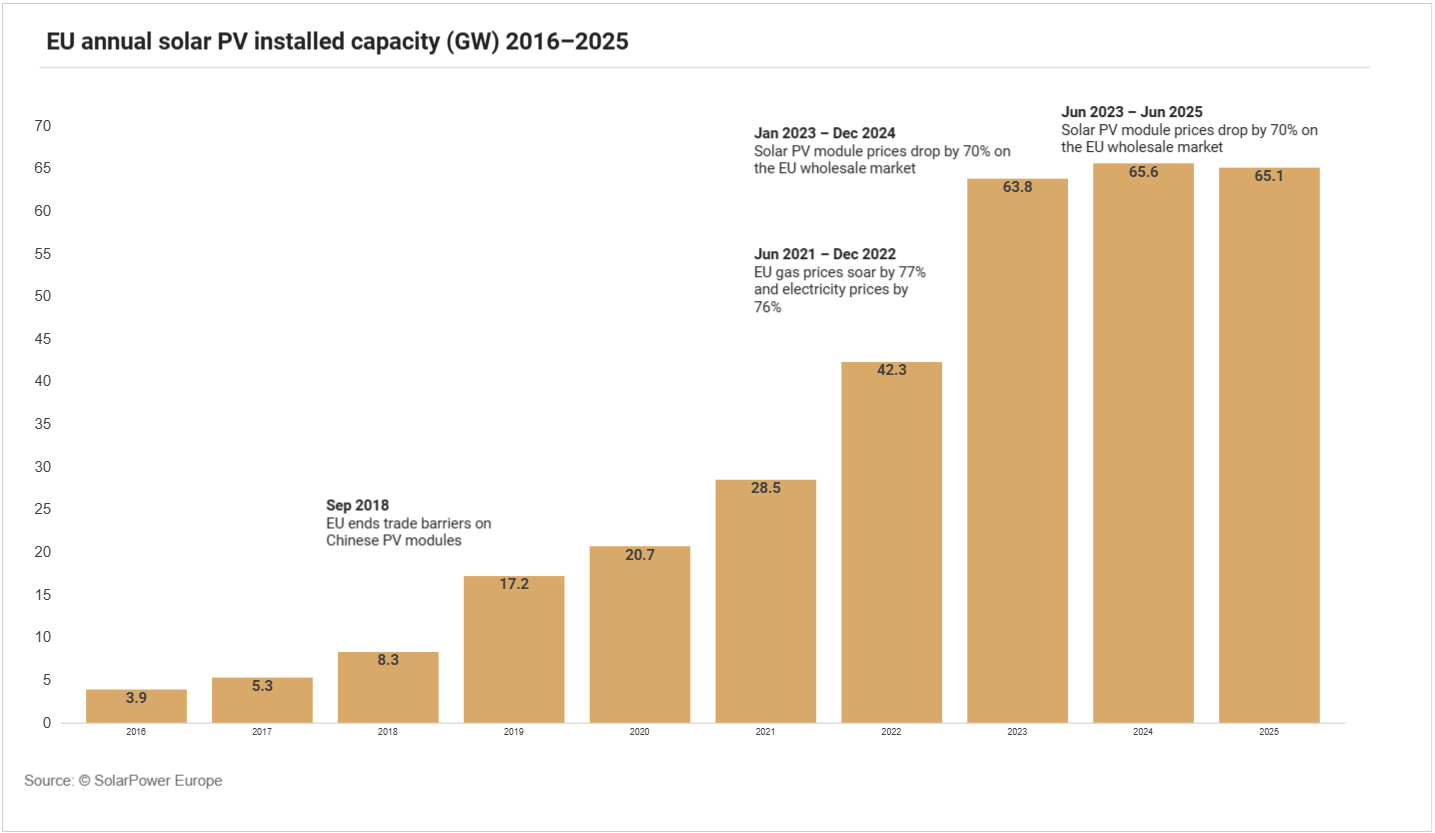

Meanwhile, based on SolarPower Europe’s EU Solar Market Outlook 2025–2030, Europe’s solar story in 2025 was the kind that looks perfect in capacity charts and complicated in revenue models:

- Solar’s electricity share in the EU is expected to reach 13.4% in 2025, up from 11.6% in 2024, a fast structural shift in the generation mix.

- But the market signal underneath got complicated: lower capture rates and more volatility in high‑renewables markets.

In plain terms: Europe is producing more solar electricity, and paying less for each incremental unit at the hours solar produces the most.

That “value compression” shows up in multiple layers that matter directly for M&A underwriting:

1. Capture rates (the price your solar actually earns) deteriorated in key markets

SolarPower Europe points out that solar capture rates are falling across Europe’s most mature markets. In 2025, average capture rates dropped to around 58% in Germany and 52% in Spain, reflecting increased cannibalisation during peak solar hours.

At these levels, a larger share of revenues is exposed to wholesale price volatility, which means merchant exposure plays a materially bigger role in valuation and deal structuring.

2. Route‑to‑market is tilting harder toward auctions while PPAs face pressure.

Across Europe, auctioned volumes have remained dominant in utility‑scale procurement, while the corporate PPA market shows signs of slowing in parts of the region.

3. Storage becomes part of the underwriting logic

Not because batteries are trendy, but because data from LevelTen’s Q4 2025 report point to batteries as the most straightforward way to defend capture value, reduce volatility exposure, and regain control over delivery profiles. We’ve covered the BESS angle in more detail in a previous edition.

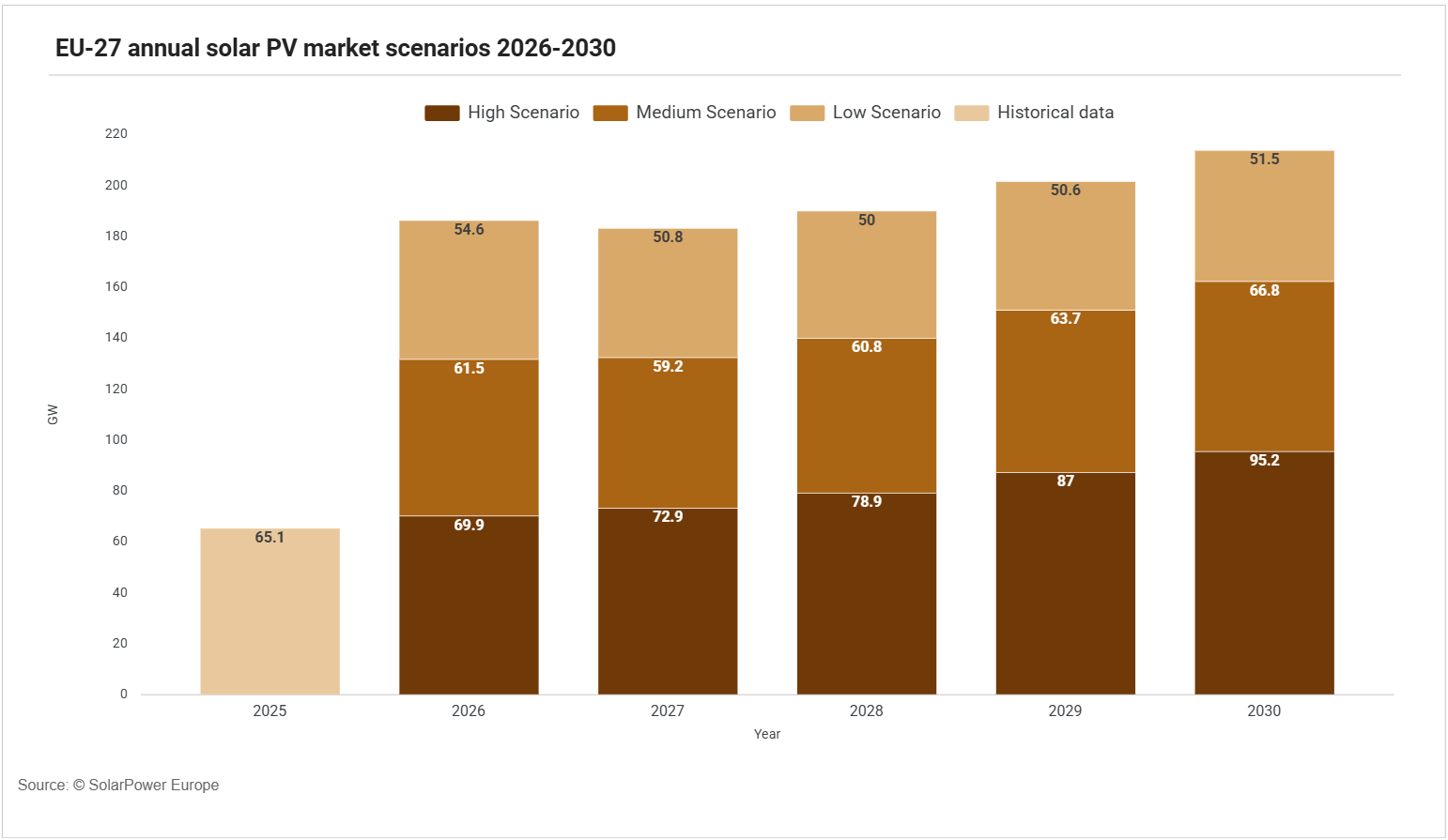

In 2026, market reality is going to reshape solar growth

Looking ahead to 2026, SolarPower’s report broadly aligns with other recent publications, and taken together, they point to a set of key insights for the sector.

A) Financing conditions: lower friction helps deals selectively

Market outlooks point to a more constructive macro backdrop for transactions if financing costs keep easing. In practice, that typically favors:

- platforms with scale,

- assets with resilient contracted cashflows,

- portfolios that can be optimised (repowering, co‑location, storage add‑ons).

B) Power‑market reality: Pure‑play solar PPAs keep repricing

Europe’s corporate PPA pricing trend has been down, with European P25 solar PPA prices down 8% year‑over‑year according to LevelTen’s Q4 2025 index update.

The same update also flags the underlying drivers: low/negative power prices and solar cannibalisation eroding contract values, pushing developers toward hybridisation and making storage pricing increasingly relevant in corporate procurement.

- This is where the M&A implication becomes very concrete: when contracts reprice and merchant risk rises, buyers become pickier about what kind of solar they’re buying.

C) Grid and permitting: the policy narrative is converging on “first‑ready”

Grid constraints are no longer an abstract “challenge section” slide, they are becoming a central design principle for policy and for deal screening.

At EU level, the Commission’s European Grids Package explicitly focuses on faster permitting and queue discipline, including the “first‑ready first‑served” principle and measures to streamline grid connections and infrastructure build‑out.

If implemented effectively, an analysis from Delfos Energy suggests that it could reduce the advantage of speculative queue positions and increase the premium on projects that are genuinely ready to build and connect.

D) Solar market growth remains concentrated (which matters for deal flow)

Looking into 2026–2030, the largest additions remain concentrated in the big markets (Germany, Italy, Spain), with continued emphasis on utility‑scale build and grid‑access realities.

For M&A, concentration tends to do two things:

- It attracts more institutional capital into a smaller set of jurisdictions (raising competition for “good assets”),

- and it increases the dispersion between “headline MW” and “bankable MW”.

Battery storage

- Europe | Schroders Greencoat partners with CATL and Lochpine Capital to jointly develop up to 10 GWh of battery storage projects, establishing a European energy storage investment platform

- Germany | Zenobē enters German battery storage market by acquiring 1.3 GW/2.5 GWh of operational and under-construction BESS assets, backing large-scale grid-level expansion

- Latvia | Elenger Grupp acquires Mood Deco, securing development-stage battery energy storage project to expand regional energy storage portfolio

- Latvia | NGEN Group acquires 100 MW/200 MWh battery storage project via SIA Liepaja ESS, committing €50 m to enter Latvian energy storage market

Multiple

- Europe | European Commission clears renewables joint venture between Plenitude and Societe Generale’s Vulturno Investments, enabling multi-technology solar, wind and storage expansion across key European markets

- Europe | Ørsted agrees to sell its entire European onshore wind, solar and BESS business to Copenhagen Infrastructure Partners for €1.44 bn, refocusing strategy on offshore wind

- Spain | Brookfield launches sale of renewables developer X-Elio at ~€4 bn valuation, initiating major divestment of multi-country platform with storage exposure

Retail/Grid Network

Solar

- Italy | Comunita Energetiche agrees to sell 13.7 MWp solar development portfolio in Puglia to infrastructure fund, divesting non-core assets to refocus on C&I energy communities

- Italy | Zenith Energy acquires 10 MWp agrivoltaic solar project in Piedmont for ~€0.8 m, expanding Italian development portfolio toward 200 MWp target

- Spain | Galp agrees to sell 525 MW near-ready-to-build solar portfolio in Aragón to Ignis, accelerating capital rotation as it refocuses Spanish renewables strategy

- Spain | Iberdrola contributes 646 MW of operational solar farms to joint venture with Norges Bank Investment Management, expanding co-investment platform to 1.5 GW of renewable capacity

- United Kingdom | Schroders Greencoat agrees to acquire 283 MW solar portfolio from Metlen Energy & Metals, adding income-generating assets backed by long-term corporate offtake agreements

Solar + BESS

- Germany | Green FOX Energy and ON Energy divest 85 MWp solar portfolio with co-located battery storage to German family office, recycling capital to advance development pipeline

- Germany | MEC Energy partners with CleanCap to develop 500 MWp solar and 2.5 GW battery storage portfolio, advancing large-scale hybrid and standalone BESS pipeline

- Germany | RP Global and MaxSolar sign MoU to jointly develop over 100 MW per year of solar PV and battery storage projects, accelerating utility-scale renewables rollout

Wind

- Europe | MEAG agrees to acquire minority stake targeting 24% in offshore wind installation specialist Fred Olsen Windcarrier, backing long-term growth in turbine installation and marine services

- Finland | Metsähallitus agrees to sell project rights for up to 800 MW onshore wind portfolio to Nordic Generation, supporting large-scale renewables deployment toward carbon neutrality

- Germany | European Energy divests 5.56 MW Henglarn onshore wind project to DaVinci Energy, rotating capital from operational assets into German renewables development pipeline

- Greece | EDP completes sale of 150 MW operating wind portfolio to Enel- and Macquarie-backed Principia for ~€200 m, continuing asset rotation strategy

- Poland | PGE Renewable Energy acquires 35 MW Dzwola onshore wind farm, strengthening eastern Poland footprint and advancing onshore wind expansion strategy