Sebastian Montoya

Sebastian Montoya

If 2025 had a closing scene for clean-energy M&A in Europe, this would be it: deals still landing with the Christmas lights already on, and a clear message underneath the headlines.

The last Teaser Energy Europe edition of the year brings you 20+ announced deals spotted by our curation, plus a provocation: as AI keeps pushing power demand up, renewables stand out as scalable and flexible solution heading to 2026.

This week’s top stories include:

- A big platform bet: Qualitas Energy is reportedly in advanced talks to buy 50% of Cubico at a €7bn valuation, a move that’s less about one asset and more about owning a machine that can keep building deals.

- Capital recycling: TotalEnergies agreed to sell 50% of a 424 MW Greek wind-and-solar portfolio to Asterion for €508m, keeping operatorship and an offtake role while freeing cash for the next chapter.

- Gas is still in the mix: EQT secured control of renewable gas player Waga Energy after a tender offer valuing it at €534m, and Iberdrola agreed to sell biomethane development projects in Spain as it sharpens its electrification focus.

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

Momentum is back and clean energy is riding the rebound

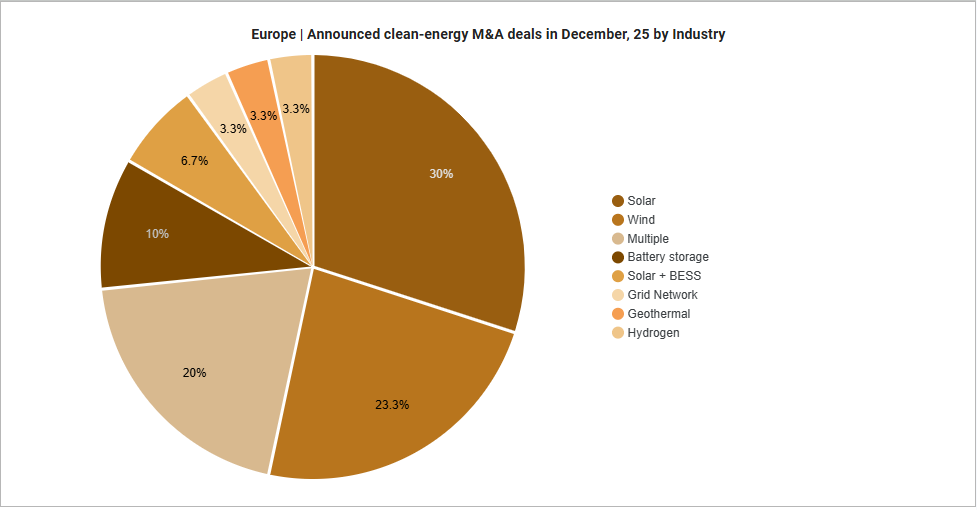

The 22 clean-energy M&A announcements we spotted across Europe this week capture a feeling that could sum up much of 2025’s dealmaking in one word: momentum.

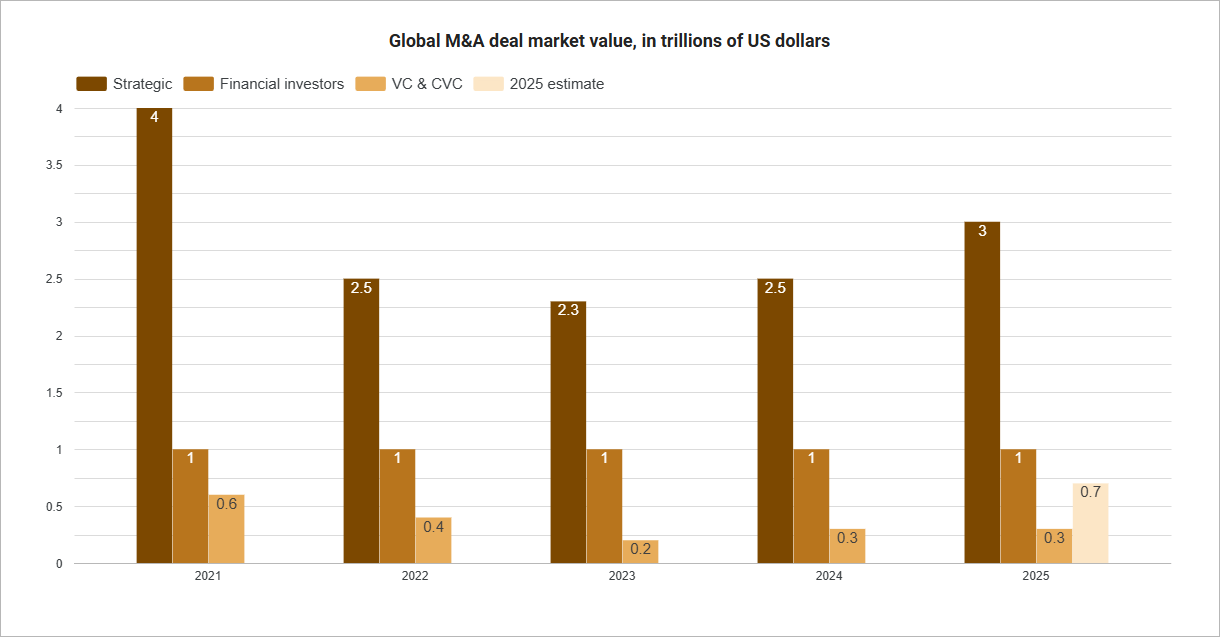

Across markets, even if global deal volumes bring no real surprises, the appetite to close transactions is still here and it shows up in rising deal values. In the broader backdrop, firms like Bain & Company have described 2025 as a potent rebound: global deal values (across industries) grew 36% in 2025, and the forces behind that lift may be the same ones that keep renewables in the spotlight in 2026.

The rebound in 2025 is notably broad-based across industries and geographies. But it’s hard to ignore how concentrated (and how influential) AI has been in the numbers.

By some estimates, 75% of strategic acquirers have assessed the impact of AI on a target’s business. And if powering that wave requires more electricity, then the “big three” we highlighted in our last edition (solar, wind and battery storage) start to look like a catalyst for opportunity.

Some key insights:

- Fast-moving technology needs infrastructure that can keep up. Flexibility, resilience, and speed to deploy have turned solar, wind and battery storage into deal magnets in 2025. The frame from our December curation shows that, so far, interest in the industries seems to remain strong.

- And as power demand has ramped up, the impact has started to show up in the spreadsheets: Costs per MWh have been trending down just as data-centre contracts start getting heavier.

- Looking ahead, 2026 may bring even more openings: As regulatory developments enable more technology deployment across the EU, and dealmakers keep their expectations anchored around continued activity.

AI changes the game and energy sits at the core

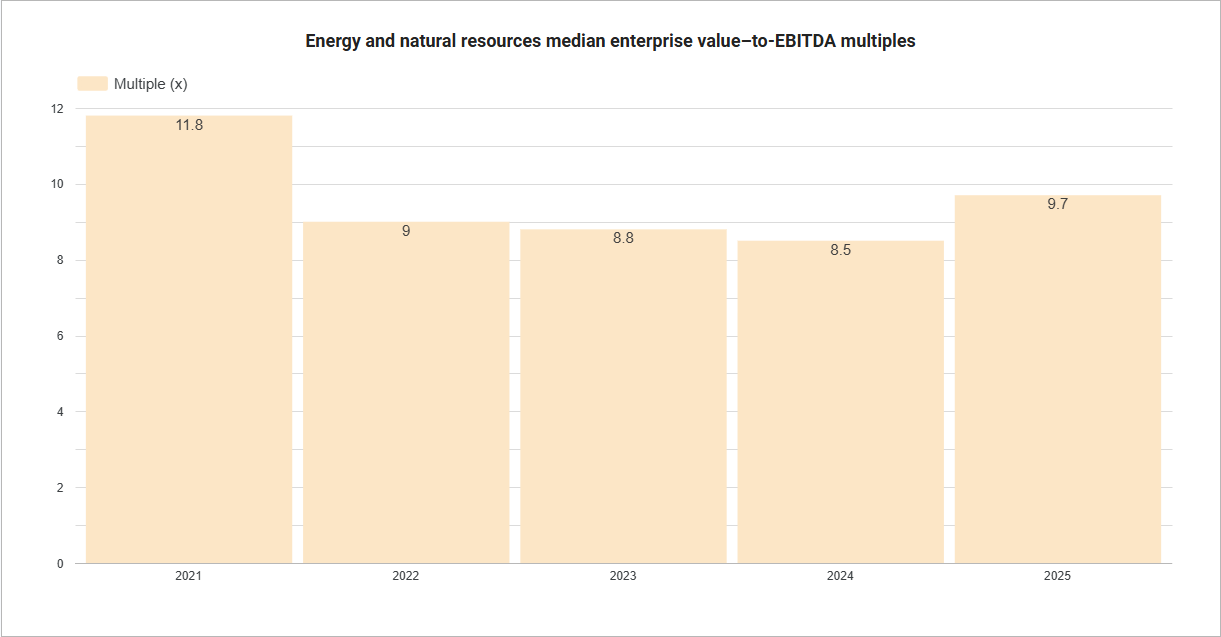

The scramble for energy assets is global. It’s estimated that sector valuation multiples in 2025 climbed to 9.7x, up from 8.5x in 2024. The drivers are varied, but one theme stands out: AI is reshaping dealmaking across sectors.

Companies across the board will need to invest in AI capabilities, physical automation, and modernising their tech stack. In a market that rewards early adopters, that has become a real competitive edge for businesses looking to cut costs and streamline operations in 2025.

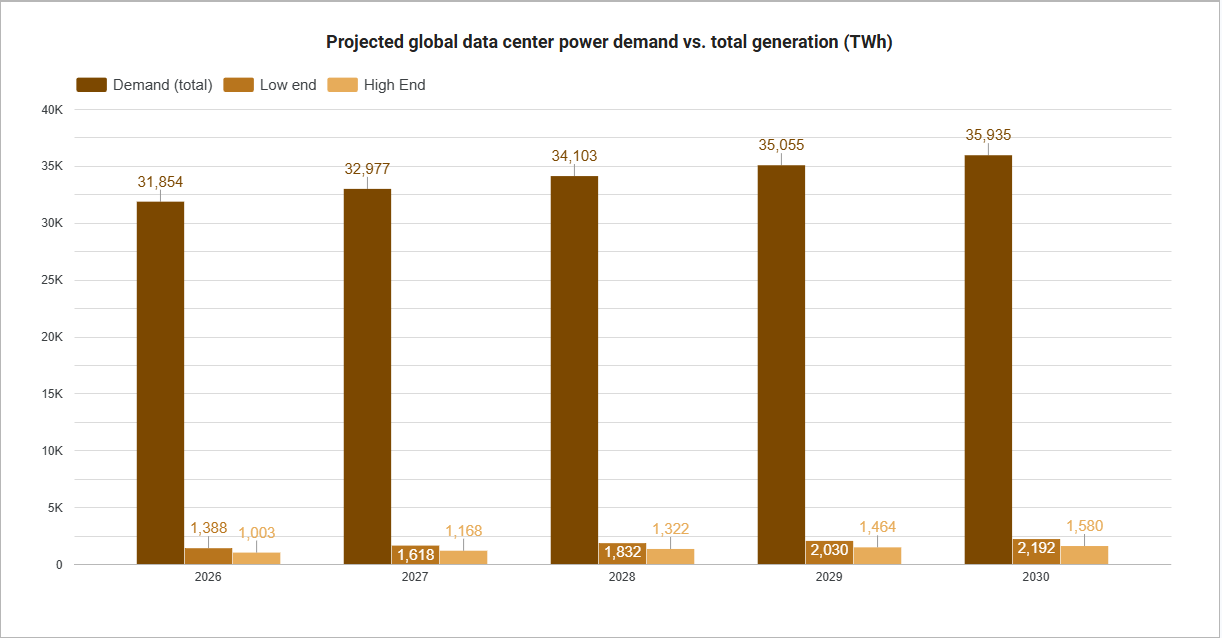

And in an economy supercharged by AI, S&P Global Energy’s high-growth view suggests global data-centre power demand could grow 17% to 2026 and 14% per year through 2030, reaching potential demand of over 2,200 TWh (roughly equivalent to India’s current total electricity consumption).

The demand is there, and it favours renewables.

As a reference point in the US, Lazard’s June 2025 LCOE report still finds renewables to be the most cost-competitive new-build option on an unsubsidised $/MWh basis. This is especially relevant in a high power-demand environment, where renewables stand out as both the lowest-cost and quickest-to-deploy resource.

Using Lazard’s LCOE (the all-in cost per MWh to build and run a typical plant over its lifetime) as a reference, unsubsidised ranges are approximately:

- Utility-scale solar PV: $38–$78

- Onshore wind: $37–$86

- Geothermal: $66–$109

- Utility-scale solar PV + storage (hybrid): $50–$131

- Onshore wind + storage (hybrid): $44–$123

- Offshore wind: $70–$157

- Gas combined cycle (CCGT): $48–$109

- Coal: $71–$173

- US nuclear: $141–$220

- Gas peaking: $149–$251

- Community & C&I solar PV: $81–$217

Lazard also lands on a few practical takeaways.

- For building new capacity and meeting rising demand, solar and onshore wind continue (in general) to sit at the cost floor of the system (even without subsidies), while also being fast to deploy.

- Storage, in turn, strengthens the mix as a complementary resource. Beyond the practicality of RTB assets, BESS value snapshots point to higher returns driven by the combination of lower costs and higher prices (a dynamic that can help expand the technology, particularly in regions where data-centre growth is prevalent);

We’re looking at a scenario where demand not only exists, but clearly favours renewables. Combined with declining cost per megawatt, this might create a series of attractive opportunities for those looking to close deals.

Setting the stage for the next wave of deals

According to A&O Shearman, the EU’s ongoing regulatory reform programme is expected to create momentum for AI-related M&A deals in 2026.

- Europe has been softening parts of its sustainability and AI rules to make it easier for companies to compete and innovate. At the same time, the European Commission has opened a public consultation to review how the EU Merger Regulation is applied in practice.

- More clarity should come in March, when Executive Vice-President Teresa Ribera will bring experts together to discuss where today’s competition rules may be falling short. The aim is to make sure the EU’s merger framework stays practical, relevant, and aligned with how markets are actually evolving.

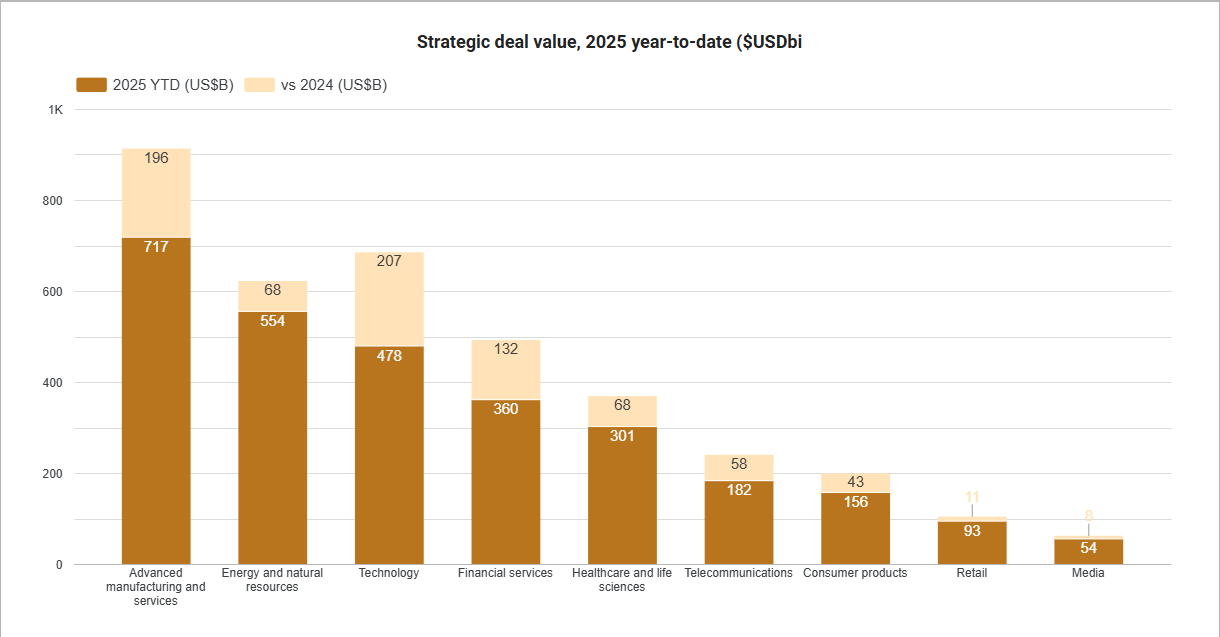

This is backed up by Bain & Company’s figures, which also show that in 2025, global strategic deal value in Energy & Natural Resources reached standout levels, even surpassing technology.

So the question becomes: how do you capture these energy opportunities and turn them into success stories?

Consider it a provocation for the holidays. Energy Europe is back in January, with the news and insights that can help you get closer to those answers.

Battery storage

- Germany | EB-SIM acquires 49% minority stake in Nofar Energy’s 104.5 MW Stendal battery project for ~€25m, marking Nofar’s first German BESS monetisation while retaining control

- Germany | ICG Infra partners with W Power Storage to back German grid-scale BESS platform, supporting multi-gigawatt battery pipeline and accelerating energy transition investments

- Germany | Ju:niz Energy acquires rights to 250 MW/612 MWh battery storage project in Brandenburg from Pacifico Energy Partners, expanding German grid flexibility backed by EQT financing

Bio-fuels

- France | EQT secures 85.88% controlling stake in renewable natural gas producer Waga Energy following tender offer valuing the company at ~€534m, paving way for potential squeeze-out

- Poland | Neo Bio Energy acquires 2 MWe agricultural biogas plant in Żórawina from Biowatt, continuing rapid expansion of its Polish biogas and biomethane portfolio

- Spain | Iberdrola agrees sale of 52 MW gas-fired slurry treatment plants and biomethane development projects to Edison Next, continuing asset rotation and sharpened electrification focus

Multiple

- Denmark | Eurowind Energy acquires stake in Ausumgaard biogas and wind energy park, marking first Danish biogas investment and expanding integrated renewable portfolio

- Greece | TotalEnergies sells 50% stake in 424 MW wind and solar portfolio to Asterion Industrial Partners for €508m, recycling capital while retaining operatorship and offtake role

- Pan Europe | Nofar Energy agrees to acquire 45.9% controlling stake in Ellomay Capital from S. Nechama Investments, Kanir Joint Investments and Anat Raphael at ~NIS 1bn valuation, pending approvals

- Pan Europe | Qualitas Energy reportedly in advanced talks to acquire ~50% stake in multi-technology renewables platform Cubico Sustainable Investments, valuing business at ~€7bn

- Poland | Eurowind Energy acquires 370 MW wind and solar development pipeline and 12 MW of operating wind assets from Sabowind, accelerating build-out of its Polish renewables platform

Solar

- Germany | Energy Invest Mittelhessen I Fund acquires 25 MWp Metternich solar project in North Rhine–Westphalia from Pacifico Energy JV, with Pacifico retaining construction and operations role

- Germany | Sunovis acquires 95 MWp ready-to-build solar PV project in Brandenburg from Visiolar, adding large-scale standalone asset to its German renewable portfolio

- Netherlands | BayWa r.e. and GroenLeven complete sale of 46 MW Skûlenboarch floating solar project in Friesland to local cooperative and public partners, enabling largest FPV park in the country

- Spain | Greening Group ups all-share takeover bid for solar firm EiDF, improving exchange ratio and seeking shareholder approval ahead of planned January vote

- Spain | ib vogt sells 95.18 MWp Baobab Solar photovoltaic project in Segovia to EOS NER Solar España, supporting EOS’s Iberian expansion under a long-term PPA

- Spain | Soltec Power launches restructuring as DVC Partners injects €30m equity and takes 80% controlling stake, stabilising balance sheet and refocusing on solar tracker core

- Ukraine | Kyivstar acquires 12.95 MW operational solar farm via purchase of SUNVIN 11, marking first move into renewables to boost energy resilience and cut power cost volatility

Wind

- France | Ocean Winds completes sale of 20.25% minority stake in 500 MW Iles d’Yeu and Noirmoutier offshore wind farm to Allianz Global Investors for ~€200m

- France | Qair acquires Eno Energy’s French subsidiary and ~260 MW cross-border wind development pipeline, strengthening its European wind portfolio and diversifying its renewable energy mix

- Germany | Encavis acquires 34 MW Bebensee onshore wind farm from PNE, extending long-standing cooperation and lifting its German wind portfolio to ~770 MW

- Germany | Enel acquires 51 MW onshore wind portfolio, adding ~€10m annual EBITDA under premium tariff and marking its first major purchase of operating assets in the country

- Poland | RWE agrees to sell 350 MW F.E.W. Baltic II offshore wind development project to PGE, transferring permits and advancing PGE’s Baltic Sea pipeline ahead of Q1 2026 close

- Romania | Greenvolt Group agrees sale of 253.1 MW onshore wind project in Ialomița County to ENGIE Romania, advancing asset-rotation strategy and strengthening ENGIE’s local renewables footprint

- Spain | Equitix acquires majority stakes in 87 MW El Castillar and Joluga onshore wind farms from Capital Energy, launching first deals under 1 GW hybrid wind-solar-battery framework