Sebastian Montoya

Sebastian Montoya

This first Teaser Energy Europe of 2026 feels like the market is switching the lights back on. The first banks and consultancies have started publishing their reports, and they all point to the same conclusion: the European energy M&A 2026 corridor is reopening, but with discipline. Steadier rates are helping pricing, equity is again funding capex, and private capital is under pressure to recycle and return cash.

Because of the holiday pause, this edition covers the announced deals we spotted between 26 December and 9 January. The top stories include:

- Capital recycling at scale: Ørsted closed the sale of 50% of Hornsea 3 (2.9 GW) to Apollo‑managed funds for DKK 39bn, reinforcing the partnership model underpinning offshore wind funding.

- Platforms, not single assets: Galp and Moeve entered talks to combine downstream portfolios, while Octopus spun off Kraken at a €7.35bn valuation (two routes to scale across retail, mobility and energy software).

- Batteries keep compounding: Gresham House agreed to acquire 297 MW of UK BESS projects and MFT Energy took a majority stake in Northium Energy, signalling storage’s central role in the flexibility build‑out.

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

European energy M&A 2026: the corridor reopens, but with discipline

As consultancies return from the year-end break, early 2026 signals suggest the financial system is beginning to function again (with greater predictability) as a channel for funding capex and operational transformation. An welcoming perspective that comes after a period jammed up by high rates, valuation gaps, and political uncertainty.

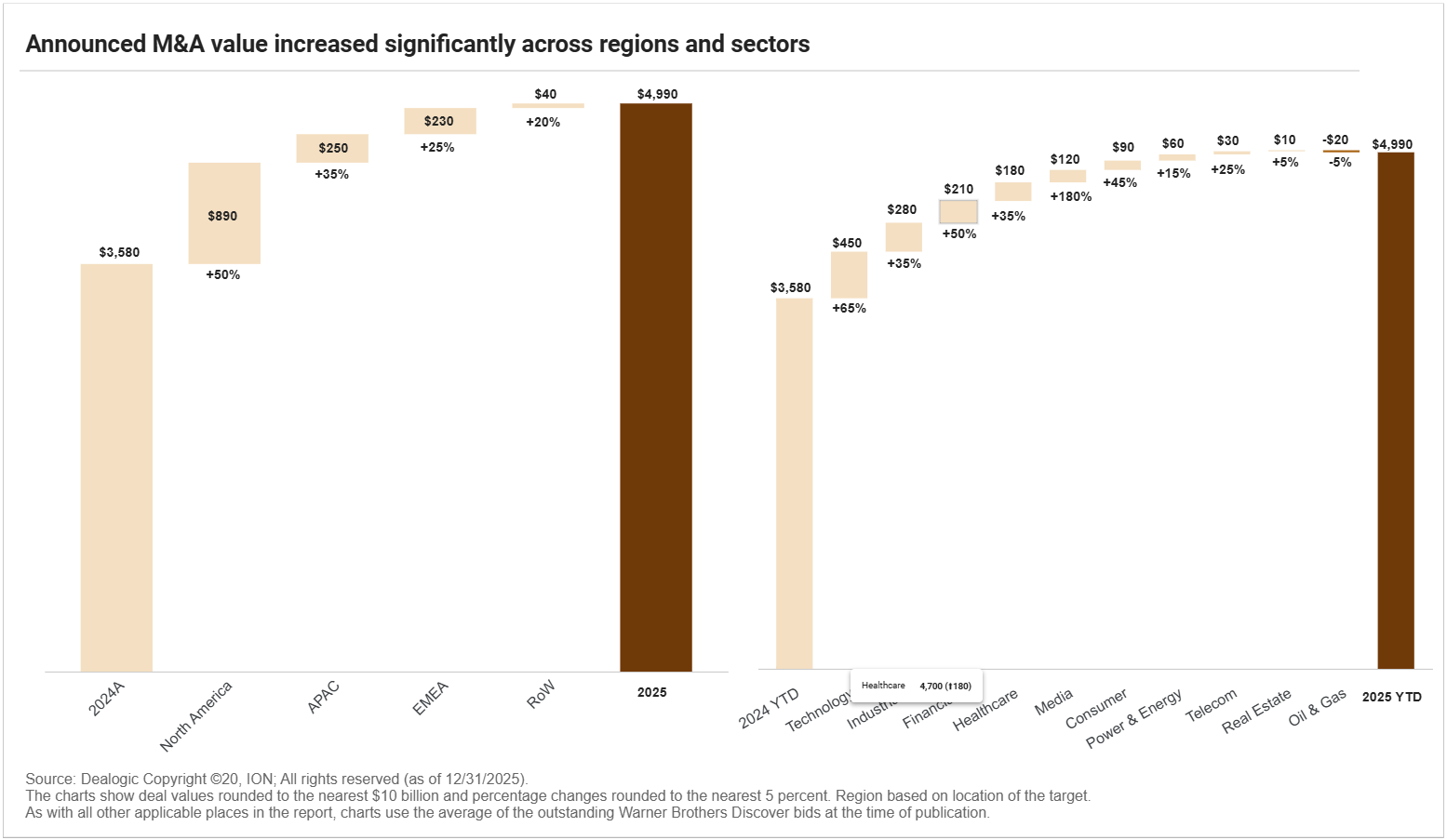

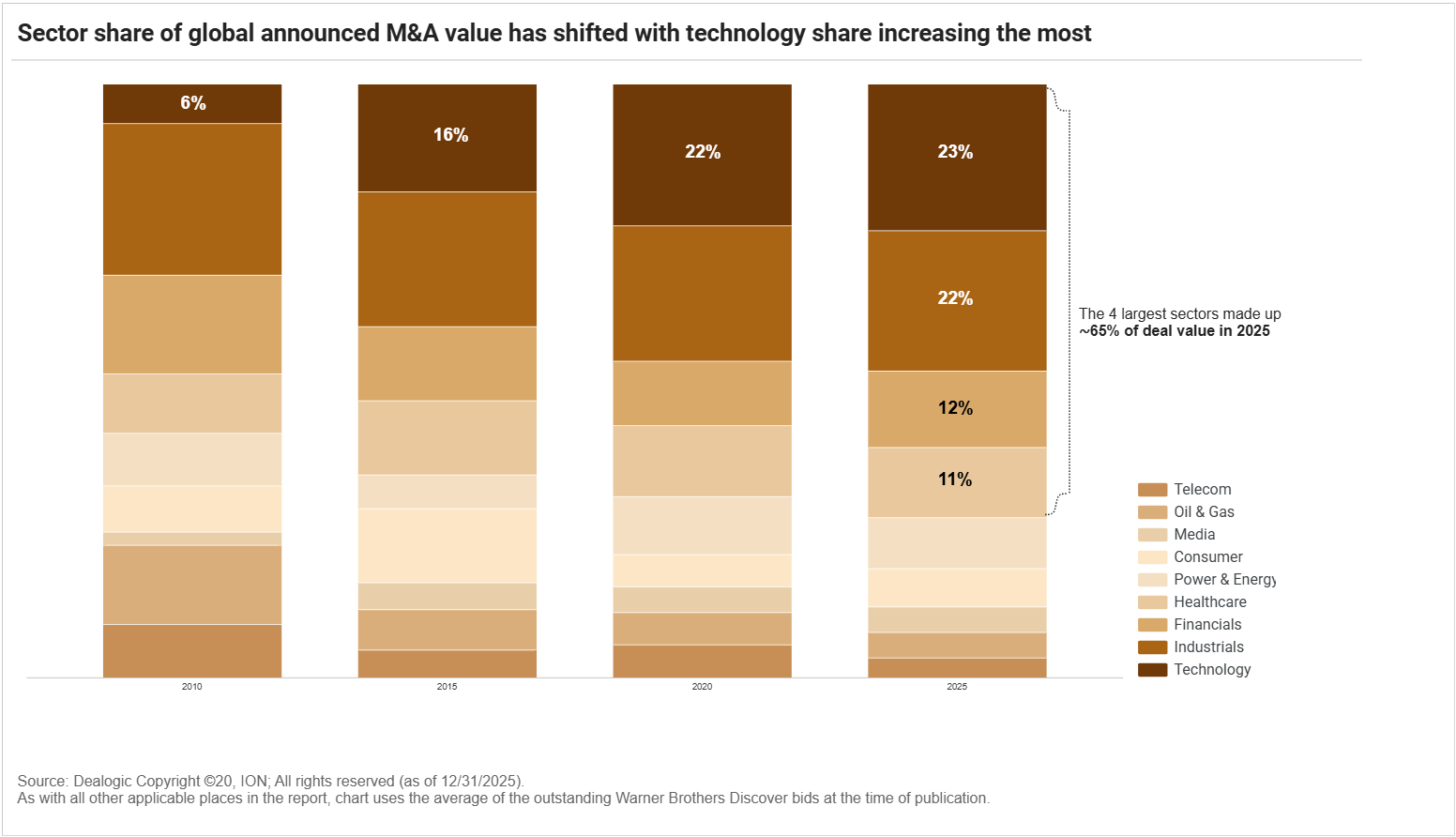

This turn comes with a number that is hard to ignore: according to Lazard, global announced M&A value grew 40% in 2025, a move the bank describes as momentum with the potential to carry into the start of 2026.

In the final 2025 edition of Teaser Energy Europe, we explored how the turn of the year might unlock new perspectives for Europe’s energy sector, as AI increasingly moves from narrative to a practical variable influencing demand and infrastructure.

Now, as January moves on, reports from consultancies and advisory houses reinforce a common point: appetite for deals and returns, but with discipline. And energy (renewables included) gains space in that equation.

The macro backdrop: steadier rates, clearer pricing, less noise in valuation

Part of that discipline comes from the macro backdrop. RSM describes that, by mid‑2025, the European M&A environment had become more “stable and orderly”, with investors returning to a strategic, long‑term approach. In the period between 2024 and June 2025, the firm says it supported 731 completed transactions in the region.

In the same window, the consultancy notes that lower interest-rate volatility has restored predictability to asset pricing. With cumulative cuts of 200 basis points by the European Central Bank, it became easier to estimate the long‑term cost of money. These factors, combined, reduce the noise when it is time to negotiate valuation.

This is where the energy sector starts to show up not as a cycle bet, but as an infrastructure equation.

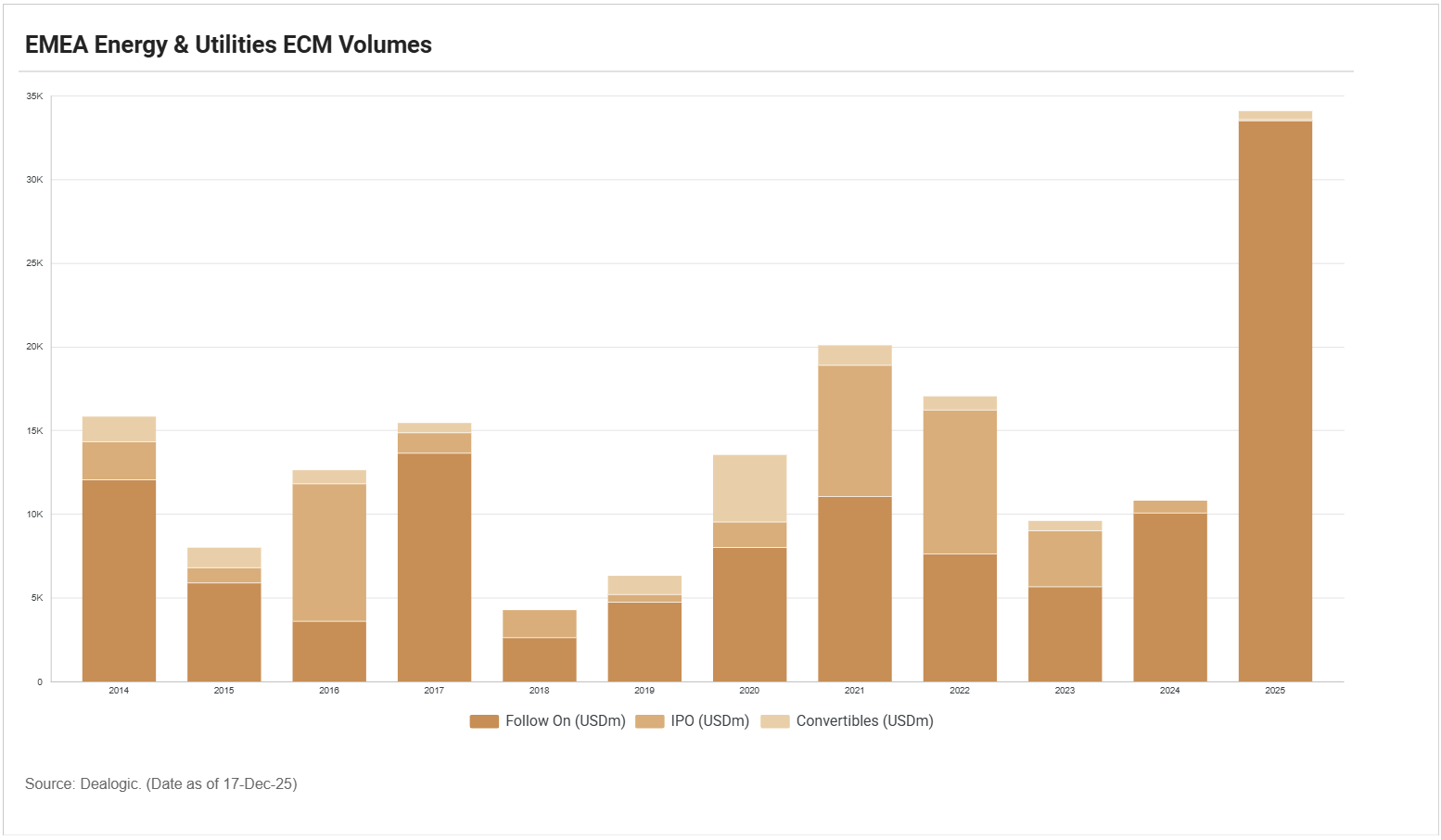

In December, Dealogic showed that equity capital markets (ECM) for energy and utilities in the EMEA region ended 2025 at the best level of the decade: US$34bn across 54 deals, versus US$10.8bn across 43 deals in 2024. The engine of the year was follow‑ons and large transactions, pulled by clear capex needs (including investment in grids).

A banker quoted by ION drew a clear link between issuance and deal pipeline. On the primary side, fundraisings were reinforced by a more active M&A backdrop, with companies tapping equity markets to finance investment programmes, regulated networks, renewables and transition assets.

Meanwhile, in private capital, CJPI frames 2026 as the year when private equity enters with a tougher “mandate”: the era of holding assets indefinitely is over, and LPs have started to demand more than mark‑to‑market gains. Their priority is DPI, the indicator that measures how much capital has actually been returned to investors, in cash, relative to what was invested.

In the European picture, this pressure tends to show up in two ways that matter for energy and renewables:

- First, via portfolio reshuffling: CJPI projects a strong year for carve‑outs in Europe, with conglomerates selling non‑core divisions to finance their own energy transitions.

- Second, via focus on transition infrastructure: cited by CJPI as one of the most attractive vectors in the region (grid, renewables, storage).

Global M&A in 2025: value rises, but stays concentrated with power & energy in the mix

This backdrop also speaks to the sector snapshot of global M&A in 2025, looking at it might be useful to calibrate expectations. Lazard’s data points to M&A value that grows, but remains concentrated in a few sectors:

- Technology

- Industrials

- Financials

- And, of course, power & energy

These four largest sectors accounted for around 65% of value in 2025, with power & energy showing up as a material slice of the mix.

For 2026, a quick cross‑analysis of these sources is less a promise of “easy money coming back” and more the formation of a more functional corridor for doing deals in Europe.

And, as we’ve seen, plenty of people reinforce this optimism. RSM points to a more predictable cost of capital. Lazard suggests available capital and infrastructure firepower. ION, in turn, reinforces an equity market willing to finance capex in utilities/energy, with the caveat that issuance needs to be properly pulled through, so investors do not get saturated.

All of this suggests that clean energy M&A in Europe in 2026 is moving towards concentrating capex and liquidity in the same assets. In energy, mainly grids, regulated infrastructure, and transition platforms. Renewables are on the agenda, and our moment is good.But, at the same time, regulation and price volatility remain as brakes (and should continue to dictate deal structure and timing). The next few quarters should be able to tell whether those brakes can actually reduce the speed of this locomotive. 2026 promises to be anything but boring.

Battery storage

- Denmark | MFT Energy acquires majority stake in BESS developer Northium Energy, entering utility-scale battery storage to expand physical asset footprint under Envision ’28 strategy

- France | Axens, Syensqo and IFPEN form Argylium to develop and industrialise solid-state battery electrolytes in France, targeting commercial-scale production by 2030

- United Kingdom | Gresham House Energy Storage Fund agrees to acquire 297 MW of UK battery projects including Cockenzie and Monet’s Garden, advancing three-year BESS growth plan

Retail/Grid Network

- Spain | Galp and Moeve enter non-binding talks to combine downstream portfolios into RetailCo and IndustrialCo, targeting scale in Iberian energy, mobility and low-carbon platforms

- United Kingdom | Balfour Beatty sells equity stakes in OFTO assets for three UK offshore wind projects to Equitix as part of £87m infrastructure divestment, progressing operational asset disposal strategy while Equitix consolidates OFTO portfolio exposure

Solar + BESS

- Europe | Hydro Rein sells Energy Solutions unit to Global Green Asset Management, carving out behind-the-meter solar and battery business to focus on large-scale renewables

- Germany | Cube Infrastructure Managers raises €150 m for CubIKS solar PV and battery storage platform, lifting total equity to €325 m to build 1 GW hybrid portfolio with The Dillinger Group

Wind

- Denmark | SUSI Partners sells 89 MW onshore wind portfolio to NRGi Renewables, completing final exit of SUSI Renewable Energy Fund II after full fund lifecycle

- Europe | Holcim takes minority stake in BW Ideol, partnering to scale floating offshore wind foundation fabrication in France and Scotland under clean energy infrastructure growth strategy

- Germany | Qualitas Energy acquires 91 MW onshore wind portfolio from PNE AG across Rhineland-Palatinate, Hesse and Brandenburg, strengthening near-term delivery and long-term German pipeline