Sebastian Montoya

Sebastian Montoya

This week’s Teaser Energy Europe comes with BESS still accelerating (both in individual projects and platform plays), while wind is in consolidation mode, with players rotating capital and deepening their presence in key markets.

We’re also bringing in takeaways from PwC and Bain & Company, and a set of seven practical realities for getting deals done in 2026.

And, of course, the usual latest European moves, and the strategies behind them:

- RWE agreed to sell its Swedish wind portfolio, covering onshore and offshore assets, alongside a 1.8 GW development pipeline, transferring a sizeable wind platform in the Nordics to Aneo.

- ContourGlobal entered the Greek market through the acquisition of 37 MWp of operating solar PV and a 500 MW/2,000 MWh battery storage pipeline, combining live assets with large-scale storage optionality.

- Prime Capital acquired Project Monet, a 135 MW battery storage project with four-hour duration, adding a fully permitted grid-scale BESS asset in Germany.

Want more insight? Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

Celebrating TetraxAI’s €1.5m funding milestone

Congratulations to our friends at TetraxAI on announcing a €1.2m funding round, led by The Footprint Firm, with participation from Norrsken Evolv and Carbon13.

With this round, TetraxAI has raised a total of €1.5m to accelerate the use of AI to streamline and automate due diligence and risk management for clean energy infrastructure projects.

Cheers!

Negotiating energy deals in Europe in 2026: seven realities you can’t ignore

PwC’s Global M&A Trends in Energy, Utilities and Resources, released early last week, points to an active market broadly aligned with the insights we have been sharing in Teaser Energy Europe.

- First: PwC highlights that deal volumes remained broadly stable throughout 2025, while values swung sharply depending on whether megadeals came into play.

- That was the reality of 2025, but also a continuation of the discipline that has been taking shape since 2022, following the sharp pullback in 2021.

- Over 2025, headline deal value in the region peaked at around the USD 200bn mark at previous highs (notably in 2016 and 2021) before settling closer to the USD 100bn range in 2024 and in PwC’s estimate for 2025.

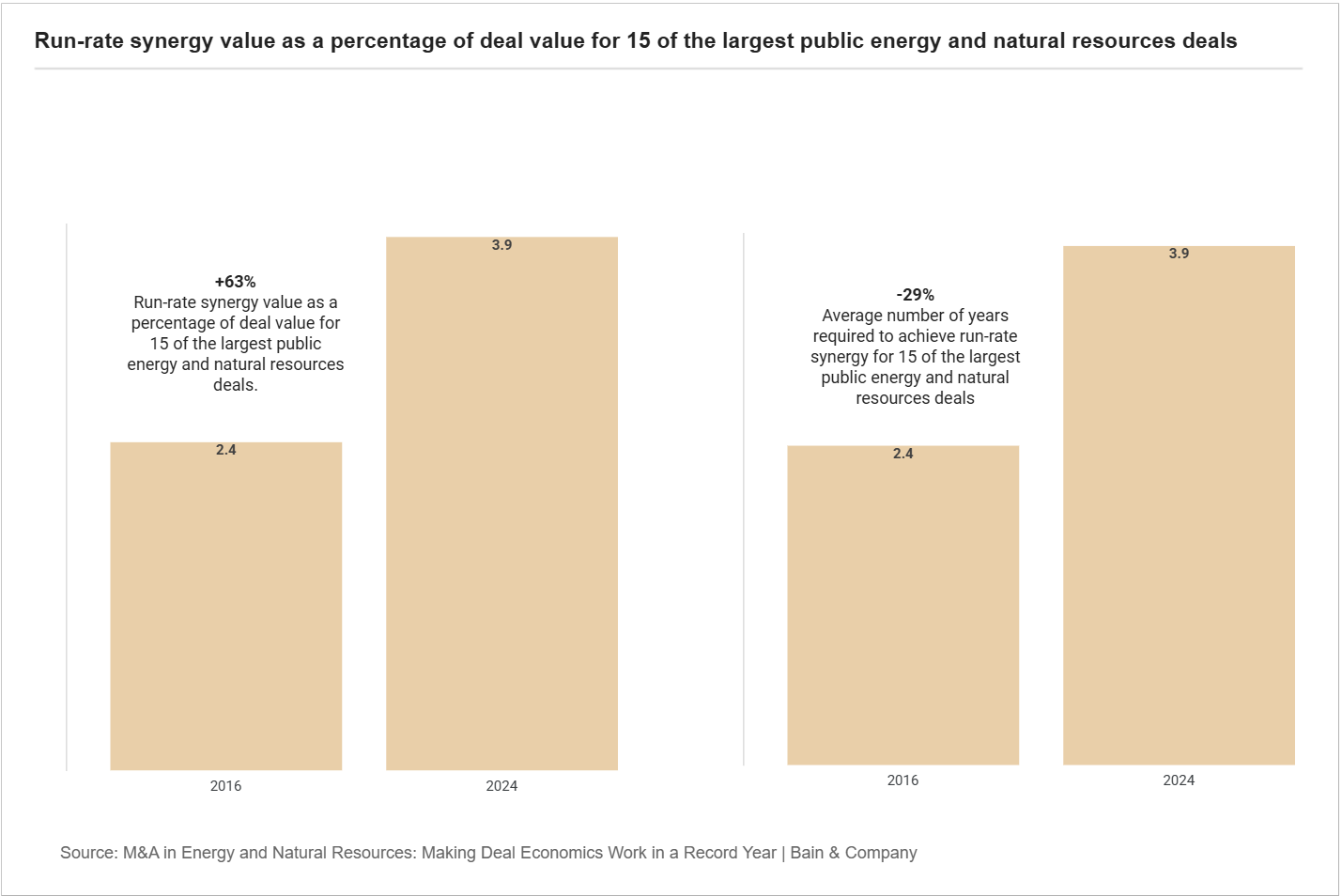

Bain’s Energy, Utilities and Resources data, also published in January, delivers an even clearer message. Run-rate synergy value, as a share of deal value, increased from 2.4% in 2016 to 3.9% in 2024, while the average time to reach run-rate synergies fell from 2.1 years to 1.5 years.

- In plain English: buyers still care about strategy, but they want payback sooner, and they’re building that expectation into the deal.

Taken together, these trends reinforce the core negotiation challenge for 2026. The market will reward certainty and speed, but penalise ambiguity and slow integration.

Finding the balance takes strategy, information, and good data. In today’s Teaser Energy Europe, I’ll help with the first two: below are seven realities worth having in mind, plus what they usually mean when you’re actually negotiating.

Ready? Let’s get into it.

1) In 2026, “capacity you can count on” beats “optionality with upside”

PwC’s big idea is simple: demand is shifting, not just cycling.

The growth of AI and data centres is lifting demand for power (and related infrastructure), and that changes what buyers pay up for.

Assets that can deliver near‑term capacity and predictable cash flow tend to win out over projects that are still years away from permits, grid connection, or supply chain certainty.

What this means at the negotiating table

- You’ll spend less time debating the “story” and more time debating timeline risk.

- “When can this be online?” becomes as important as “what multiple are we paying?”

2) EMEA volumes look resilient, but values are driven by whether megadeals show up

PwC’s EMEA data shows that deal volume peaked in 2021 (1,741), then stepped down to 1,252 in 2025e. That’s the trend many teams have been feeling since the 2021 high.

But values tell a different story. The value line is much more volatile, because a handful of megadeals can change the year.

A second detail worth noting: power and utilities dominate the volume mix across industries (604 deals in 2025e). That helps explain why certainty around regulation, grids, permitting, and operating readiness feels so central in European processes.

What this means at the negotiating table

There are often two “mini‑markets” in play:

- Megadeal dynamics: structure, approvals, stakeholder management, and financing certainty are front and centre.

- Mid‑market dynamics: buyers are pickier, diligence is tougher, downside protection matters more.

If you treat one like the other, you’ll misjudge timing, terms, and leverage.

3) Consortiums aren’t just a funding choice, they change how negotiations work

PwC expects more co‑investment and consortium models, because many EU assets are simply too large, too complex, or too capital‑intensive for one party to carry alone.

That is not just a capital structure detail. It changes the shape of the negotiation.

What this means at the negotiating table

- Sellers will ask: “Who is really in charge? Who is signing? Who can make a decision quickly?”

- Buyers have to prove they can move as one team, or they risk being slowed down by their own governance.

4) Private credit is now a deal lever, treat it like one

PwC highlights private credit as a major enabler in a world where capex needs are heavy and valuation gaps can persist. In practice, private credit can be the difference between “we like it” and “we can close it”.

What this means at the negotiating table

- Financing is no longer a back‑office topic. It becomes part of your credibility.

- More flexible funding can speed things up but it can also introduce tighter lender protections.

5) Synergy has become hard currency, and it’s priced into 2026 expectations

Bain’s data is blunt: for large public energy and natural resources deals, run‑rate synergy value increased from 2.4% (2016) to 3.9% (2024), and the average time to get there fell from 2.1 years to 1.5 years.

Run‑rate is just the steady, repeatable value once integration is fully up and running. What’s changed is the expectation that it should arrive faster.

What this means at the negotiating table

- Buyers will resist paying today for value they believe they must create through integration.

- Sellers who can show “synergy readiness” (clean processes, clear data, fewer integration landmines) are in a stronger position to defend value.

6) Diligence is becoming AI‑assisted, but in Europe it still needs to be explainable

Bain notes that more acquirers are using generative AI to support, such as TetraxAI, diligence and synergy building: scanning supplier contracts, identifying savings, analysing customer and portfolio data, and speeding up early analysis.

That can improve confidence, but it can also raise expectations.

What this means at the negotiating table

- “We ran the numbers” won’t be enough. You’ll still need to explain the logic , especially when committees, lenders, regulators, or employee stakeholders get involved.

- Data access and handling matter more (GDPR, clean teams, and practical governance).

7) Integration starts before closing, not after

Bain’s point on pre‑close integration planning is worth underlining. If the market expects value faster, you can’t wait until the ink is dry to start figuring out how the combined business will actually run.

What this means at the negotiating table

- Integration planning becomes a deal lever: the more credible your plan, the less room there is for “maybe” in the terms.

- In Europe, timelines can also be shaped by labour frameworks and stakeholder engagement, so early planning is not optional.

What this means for your 2026 negotiating stance

If you’re negotiating in Europe’s EU&R market this year, you’re operating in a world where:

- Deal volumes are holding up, but the market is still keeping the same pace as after the 2021 peak.

- Average deal values can swing hard depending on whether megadeals show up. Take this into account when looking at valuations.

- Synergy expectations are higher, and the clock is ticking faster. In this context, strategies such as rapid asset rotation need to be assessed with greater care. Increasingly, value is being created beyond the exit itself.

Battery storage

- Europe | R.Power completes €250 m equity financing to scale grid-secured battery storage portfolio across multiple European markets, underpinning long-term renewables platform growth

- Germany | Prime Capital acquires 135 MW four-hour Project Monet battery storage asset in Saxony-Anhalt from Zelos Energy Developments, expanding German grid-scale BESS portfolio

- Latvia | Infinite Grid Capital-backed Baltic Energy Reserve acquires 45 MW battery storage development portfolio in Riga from Solar Energy Fund, expanding grid-scale BESS footprint

Bio-fuels

- Italy | Cycle0 acquires 1 MW Corte Pila biogas plant as part of €100 m investment programme, advancing conversion to biomethane production and grid injection

- Spain | Italian fund FIEE SGR acquires majority stake in biomethane developer Naturmet via €30 m capital increase, backing expansion of Spanish renewable gas portfolio

Retail/Grid Network

Solar

- France | ABO Energy sells three solar projects totalling 85 MWp to Tenergie and CVE, advancing capital recycling through turnkey and project rights disposals

- France | TSE partners with Ocealia to develop 500 MWp agrivoltaic solar pipeline in Nouvelle-Aquitaine, enabling long-term PV deployment alongside agricultural land use

- Germany | Aream Group acquires solar developer GME Ventures, adding 500 MWp ground-mounted PV pipeline with battery storage options to strengthen development capabilities

- Germany | Solestial acquires photovoltaic manufacturing lines from Meyer Burger to relocate solar cell production to the United States, advancing fully domestic space-focused supply chain

- Poland | Calik Renewables acquires 255 MW portfolio of operational solar farms from PAD RES Group, marking first renewable investment and strategic entry into Polish market

- United Kingdom | Funds managed by Triple Point acquire 28 MW ready-to-build solar PV project in Essex from IG Renewables and Anglo Renewables, strengthening UK energy transition portfolio

Solar + BESS

- Germany | Enlight Renewable Energy agrees to acquire majority stake in Project Jupiter, a 2,000 MWh battery storage and up to 150 MWp solar project, deepening energy storage footprint with Prime Capital

- Germany | European Commission clears solar and battery storage joint venture between EVH Gruene Energie and HSBC Alternative Investments, enabling development of hybrid project in Brandenburg

- Greece | ContourGlobal enters Greek market with acquisition of 37 MWp operational solar PV portfolio and 500 MW/2,000 MWh battery storage pipeline, scaling renewables and grid-scale storage platform

Wind

- Europe | Gulf Marine Services agrees acquisition of mid-class offshore wind support vessel, financing purchase with $37.4 m interim loan to meet rising market demand

- Sweden | RWE agrees to sell Swedish onshore and offshore wind portfolio and 1.8 GW development pipeline to Aneo, refocusing capital on core large-scale renewables growth markets