Daniel Black

Daniel Black

Hello,

The rumour mill is back up and running for 2026, with plenty of stories of deals that are either in the works or that have hit the skids.

Top stories that caught my eye:

- Shell and Exxon’s UK gas asset sale to Viaro Energy collapses

- HSBC wins Hang Seng shareholder backing for $14bn buyout

- The CMA didn’t block a single deal in 2025

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Shell and Exxon’s UK gas asset sale to Viaro Energy collapses

- Warburg Mulls $1 Billion Sale of London Insurance Broker McGill

- HSBC to explore selling Singapore insurance business

- HSBC wins Hang Seng shareholder backing for $14 Billion buyout

- Glencore and Rio Tinto resume talks on $260bn mining megadeal

- Revolut reportedly exploring FUPS acquisition to enter Turkish market

- AstraZeneca to acquire Modella AI to speed oncology drug research

- Baillie Gifford says UK Trust didn’t cut SpaceX stake for merger

- Diageo said to weigh options for China assets including sale

- SRG strengthens UK retail presence with acquisition of Hull and Leeds based broker

- Exclusive: ‘Big Brother’ owner Banijay in talks with All3Media parent over tie-up

- Blackstone moves to exit UK rental home platform Leaf Living

- UK’s Smith & Nephew to buy Integrity Orthopaedics for up to $450 million

- UK watchdog orders Aramark to divest Entier after merger probe

- UK watchdog to launch in-depth probe of AB Foods’ purchase of bread brand Hovis

- UK’s Oxford Biomedica confirms unsolicited bid from funds managed by EQT

- Mid-market PE firm launches new broker platform with acquisition of Essex broker

- Liontrust bleeds £1bn in latest quarter

Industry news

- Bank of England working to protect against non-bank failure risk, Ramsden says

- UK competition watchdog cleared every merger in 2025 after government pressure

- Sterling edges higher, key UK data flurry up ahead

- UK borrowing costs drop to lowest level in more than a year

- Bank of England’s Taylor says rates set to fall further as inflation drops

- UK business confidence drops to 3-year low, survey shows

- UK inflation expectations weakened in December, Citi/YouGov survey shows

- Barclays shares fall as Trump calls for cap on credit card interest rates

- Buy-backs in the UK have become popular. Here’s how they could be better

- Rokos Capital Management profits surge on strong performance

- Holistic Fire Safety takes on funding from Founders Private Capital

- UK economy beat expectations to grow 0.3% in November

- BoE accused of making ‘mistake’ in loosening capital rules

Salaries and bonuses

- Hedge fund Rokos Capital Management pays its people $500k per head. They might not like that

- London bankers’ bigger bonuses are fraught with complexity

- Centerview’s MDs did wonderfully in London. They got a pay cut for it

- Morgan Stanley hikes London banker bonuses by up to 15%

Job moves

- Nomura hires HSBC dealmaker Moureaux to lead financial sponsors in France

- Hargreaves Lansdown taps Vanguard for new CEO

- Mayer Brown loses levfin partner to HSF Kramer

- BNP Paribas hires ex-Citigroup trader Ford to bolster UK equities team

- Millennium hires Eisler Capital money manager

- Cofra appoints Jens Brenninkmeyer as CEO of Bregal Investments

Market trends

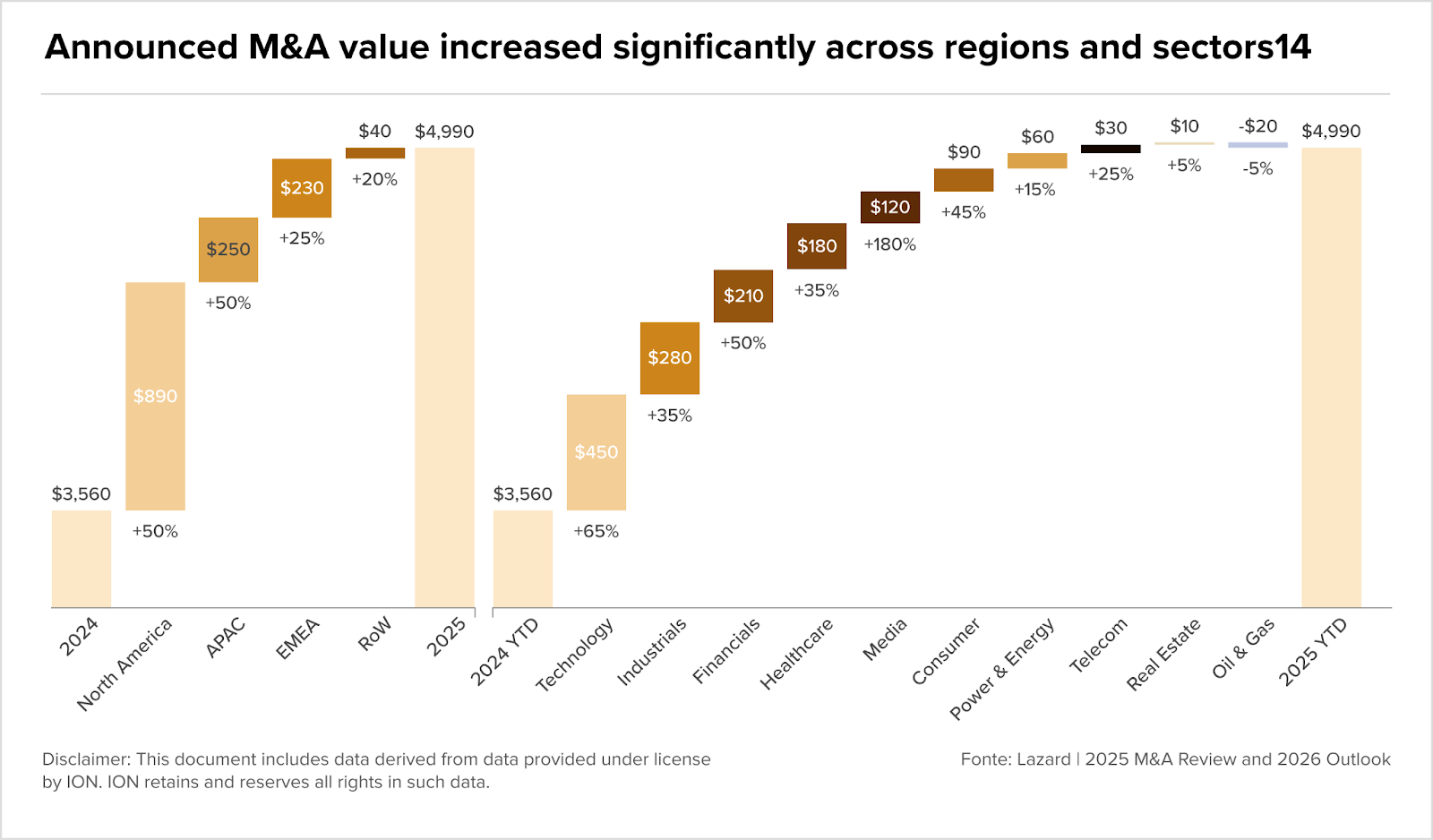

Lazard paints a rosy picture

Global M&A activity jumped in 2025, with announced deal value rising 40% YoY, according to Lazard’s 2025 M&A review. North America led this optimistic narrative as a perceived easing of regulatory constraints enabled larger transactions to proceed. APAC followed closely with an approximately 80% surge in Japan, fuelled by shareholder-friendly capital market reforms, accounting for over one-third of the region’s growth.

EMEA delivered solid gains but lacked the regulatory catalysts and industry dynamism that propelled activity in other regions, leaving it trailing the pace set by North America and Asia-Pacific.

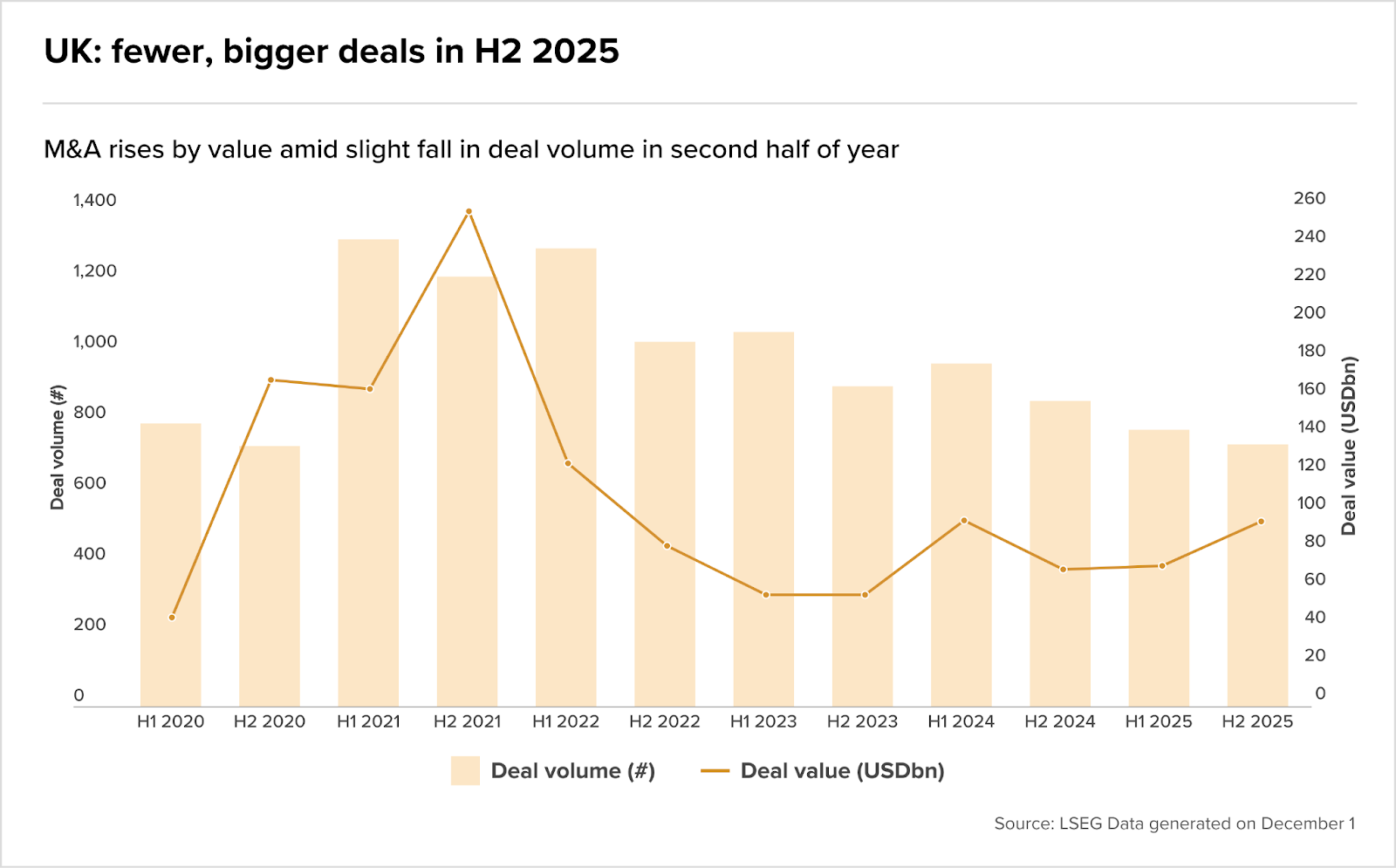

FS deals doubled in UK

The UK market’s total disclosed deal value in financial services nearly doubled from £19.7bn in 2024 to £38bn in 2025, driven by a resurgence in transactions over £1bn. Twelve deals exceeded the £1bn threshold, signalling renewed appetite for larger strategic transactions particularly in banking and insurance sectors.

Separate data from AO Shearman shows that despite Q3 2025 seeing a 16% volume decline versus Q2, aggregate deal value rose 38% as average transaction size jumped 63%, supported by improved financing conditions from more stable interest rates and inflation. This tendency is expected to carry into 2026, with increased deal processes launching and greater optimism among banks and private equity firms.

However, currency weakness and market uncertainty may have priced some UK buyers out of overseas acquisitions, with UK firms acquiring foreign targets falling from 97 to 88, whilst inbound acquisitions by non-UK firms surged from 74 to 94 deals.

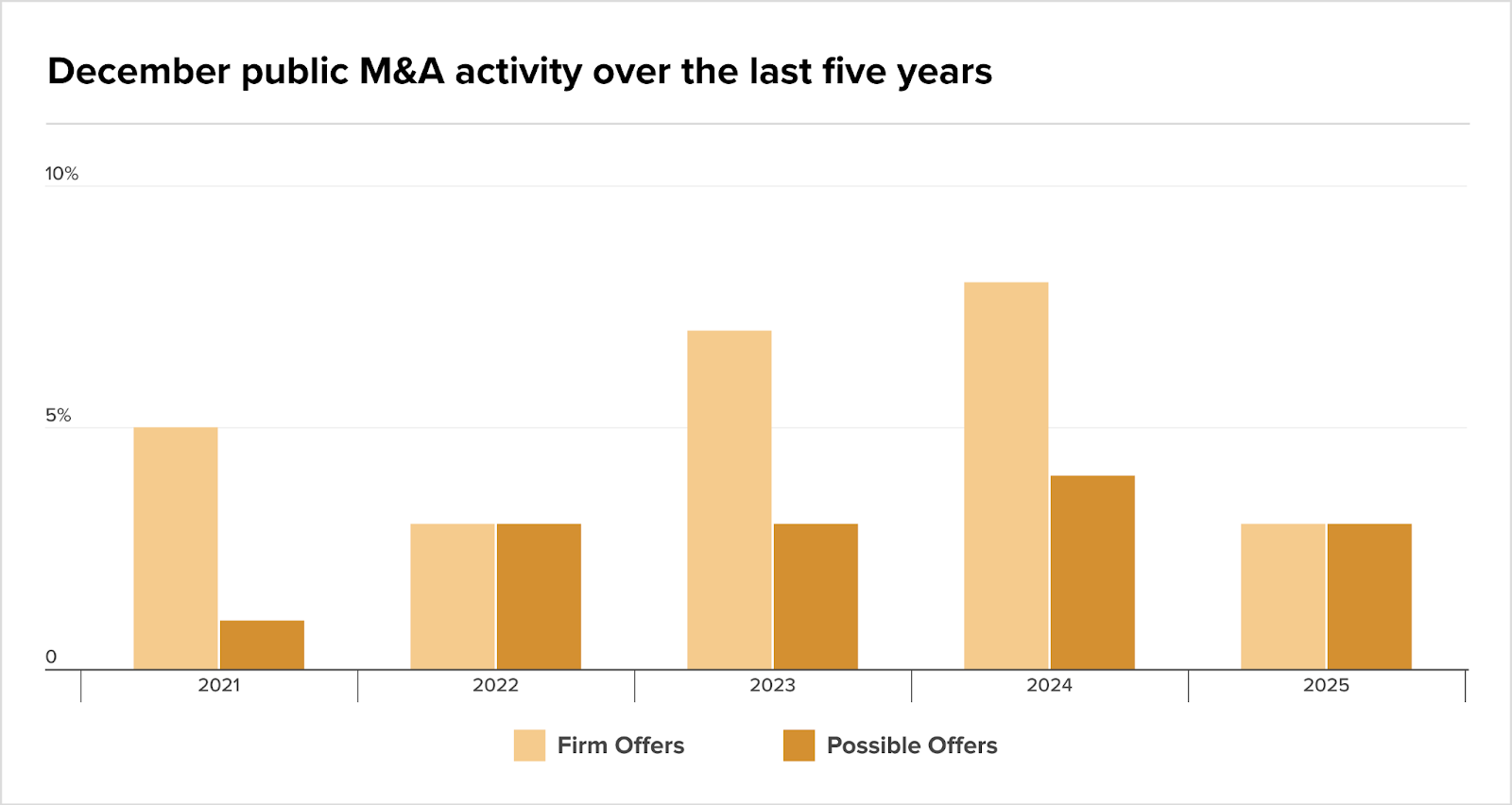

Deals drop in December

Scaling down to the UK public markets, December 2025 saw a notable dip in activity compared to the previous year. Herbert Smith Freehills Kramer recorded just three firm offers versus eight in December 2024.

But when looking at the full year, there’s a more resilient picture, with 63 firm offers announced in 2025, slightly ahead of 2024’s 57 deals. Activity peaked in Q2 with 30 firm offers, whilst H2 saw some moderation.

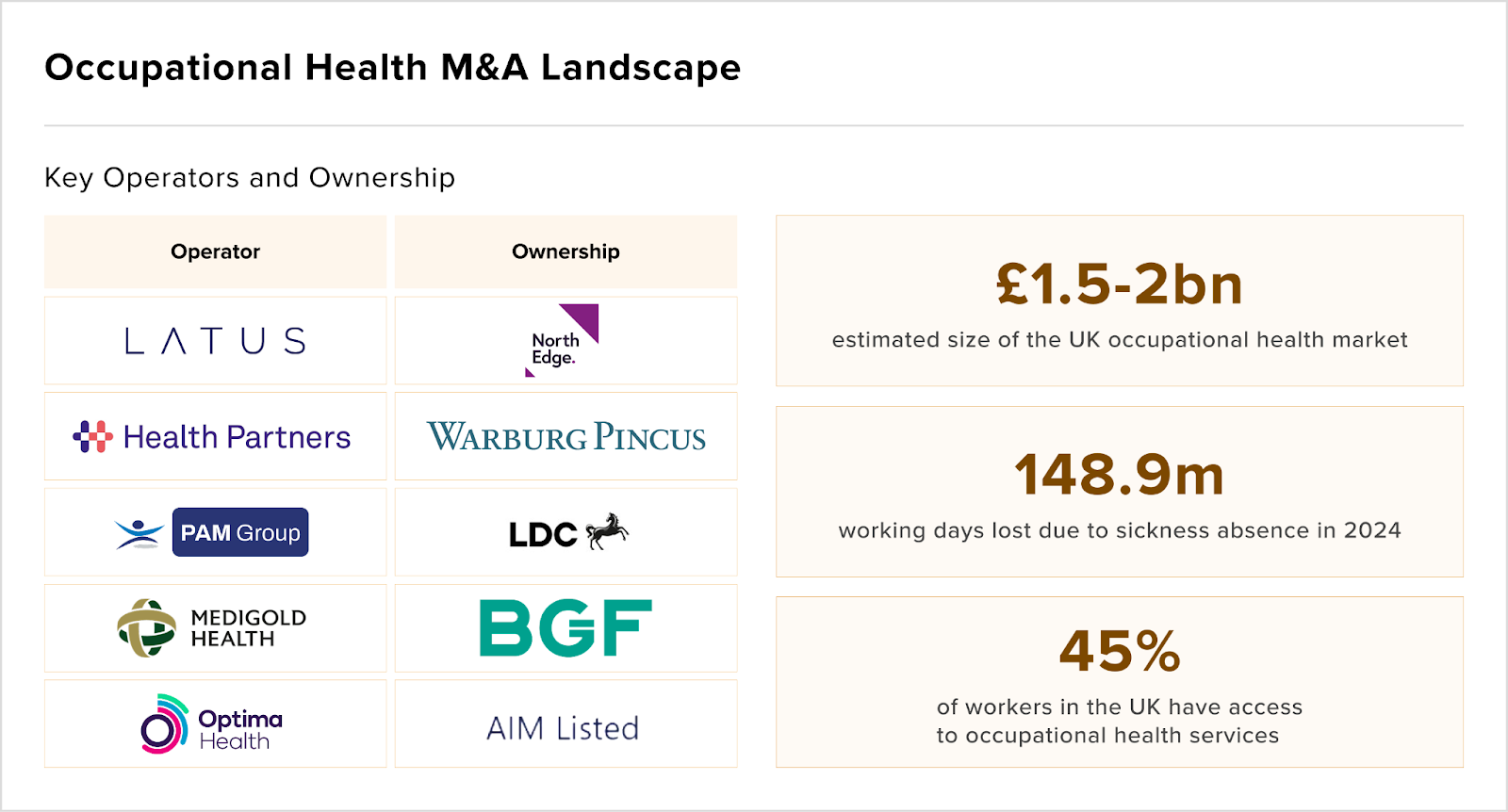

Growing market for occupational therapists

Healthcare dealmaking took an unexpected turn in 2025, with occupational health emerging as one of the UK’s most active M&A sectors. The investor appeal is obvious: a market worth £1.5–£2bn growing at 6% per year, underpinned by structural tailwinds including rising employee absences, demographic shifts towards an older workforce, and escalating mental health challenges.

The growth runway remains significant given current penetration sits at just 45%, leaving more than half of UK employees without access to occupational health support, particularly in the underserved SME segment where coverage gaps are most acute, reports Eclipse.

High-profile transactions in the field include: Warburg Pincus investing in Health Partners, NorthEdge backing Latus Health, and Spire Healthcare acquiring Vita Health, The Doctors Clinic Group and Acorn Occupational Health.