Daniel Black

Daniel Black

Schroders has this week agreed to be acquired by US firm Nuveen for £9.9bn. The asset manager was founded during the Napoleonic Wars and the deal would see the Schroder family exit the company after 222 years.

According to the FT, the deal is worth 612p per share and will likely close in Q4.

And in other news this week:

- NatWest is nearing a £2.5bn takeover of wealth manager Evelyn Partners

- UK economy grew just 0.1% in Q4

- CVC is to buy Animal Nutrition & Health for €2.2bn

Thanks for reading, and connect with me on LinkedIn if you want to discuss how Ideals VDR can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Rio Tinto and Glencore abandon $260bn merger plan

- NatWest nears £2.5bn takeover of wealth manager Evelyn Partners

- CVC to buy Animal Nutrition & Health from dsm-firmenich in €2.2bn deal

- CVC to sell minority stake in Rayner to GBL

- Sun Capital Partners closes CV on UK law firm Fletchers

- CapVest in talks to buy TSG from HLD

- Nuveen to acquire UK’s Schroders for $13.5bn

- Schroders agrees £9.9bn takeover by US investment manager Nueeven

- BNP Paribas and Wells Fargo secure key roles on £10bn Schroders deal

- Barclays’ investment bank up 7% as trading gains offset dealmaking

- Lloyds, Phoenix Submit Initial Bids for Aegon’s UK Unit

- Acorn Owners Said to Weigh Options for £1bn UK Cab Insurer

- xAI’s Babuschkin says he has not purchased London penthouse

Industry news

- UK trade deficit for goods hits record high in 2025

- UK economy ends 2025 ‘in the slow lane’ after growing just 0.1% in Q4

- UK takes key step to digital gilt issuance this year

- Retail investors pull money from UK equity funds for tenth year in row

- UK Fintech Funding Fell 21% Last Year, Hitting Lowest Since 2020

- London Stock Exchange Group’s transformation faces its biggest challenge yet

Salaries and bonuses

- Barclays’ bonuses now £900k for MDs, despite poor year for bankers

- Everything we know about the 2026 bonus round, by bank

Job moves

- Apollo names Diego De Giorgi as incoming head of EMEA

- Morgan Stanley taps former DMO chief Stheeman

- Outset Global adds four senior traders as outsourcing trend grows

Market trends

PE’s weakest year

Recent Grant Thornton data reveals that 2025 was UK private equity’s toughest year since 2020, with deal values dropping to £20.8bn across 1,722 transactions, reflecting a 9% decline in volume and nearly £2bn in value. This downturn came after a year that started with high hopes but quickly ran into challenges, particularly due to the impact of US tariff policies in early 2025.

H2 2025 activity saw a 5% increase, making it the busiest six-month period since early 2022, aside from the spike driven by Capital Gains Tax changes in late 2024. However, it still hasn’t fully recovered the losses from the first quarter.

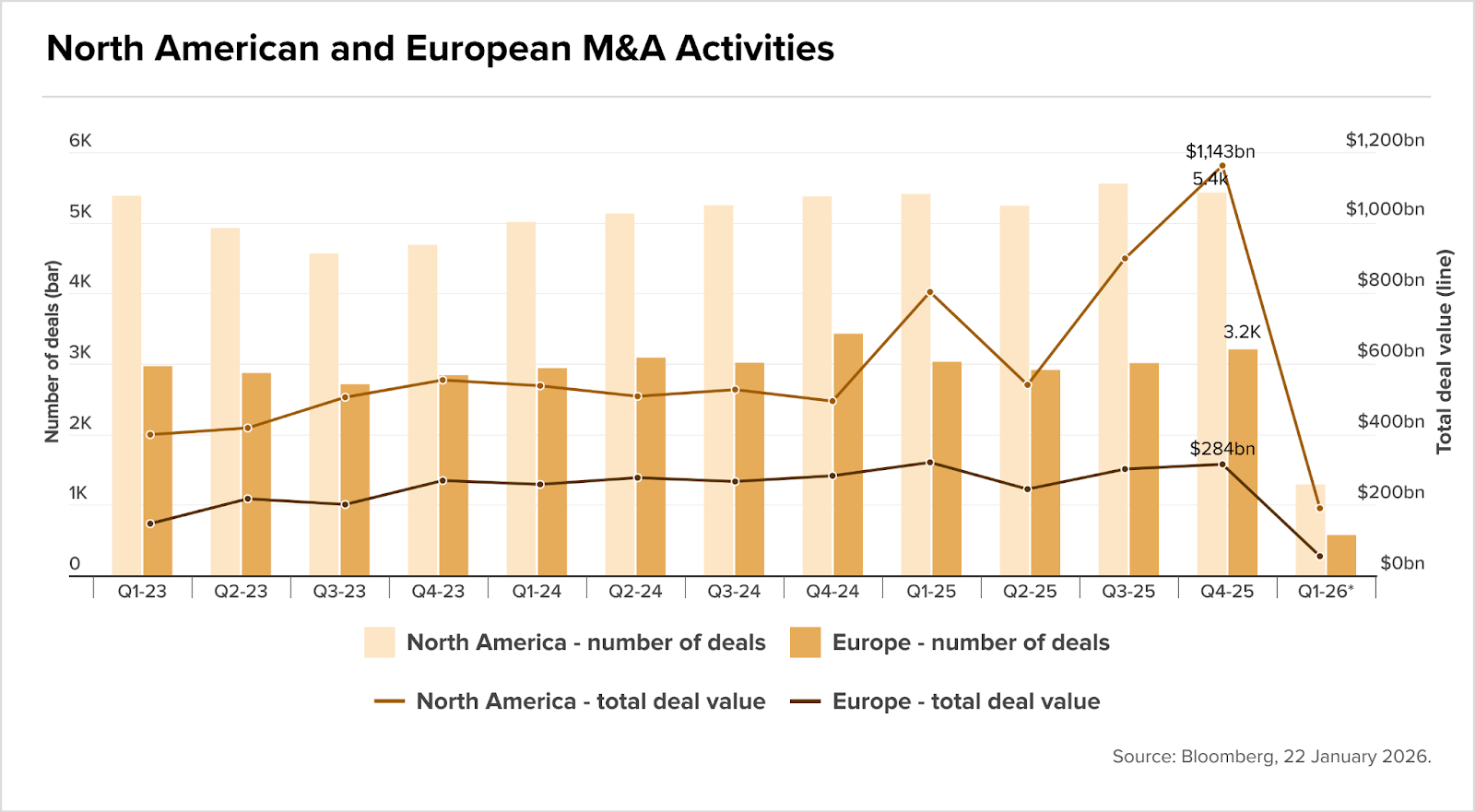

Global deal values rebound on late-year momentum

Global M&A recovered to $4.4tr in 2025, with momentum concentrated in the year’s final months, according to Macfarlanes. Twenty-two of the 70 deals above $10 billion closed in Q4 alone, while European activity jumped 25% between Q2 and Q4.

North America posted over $1.1tr in Q4 deal value, reflecting a return to scale transactions after two years of caution. The pipeline for 2026 looks serviceable, contingent on continued easing of antitrust posture in the US and stable debt markets.

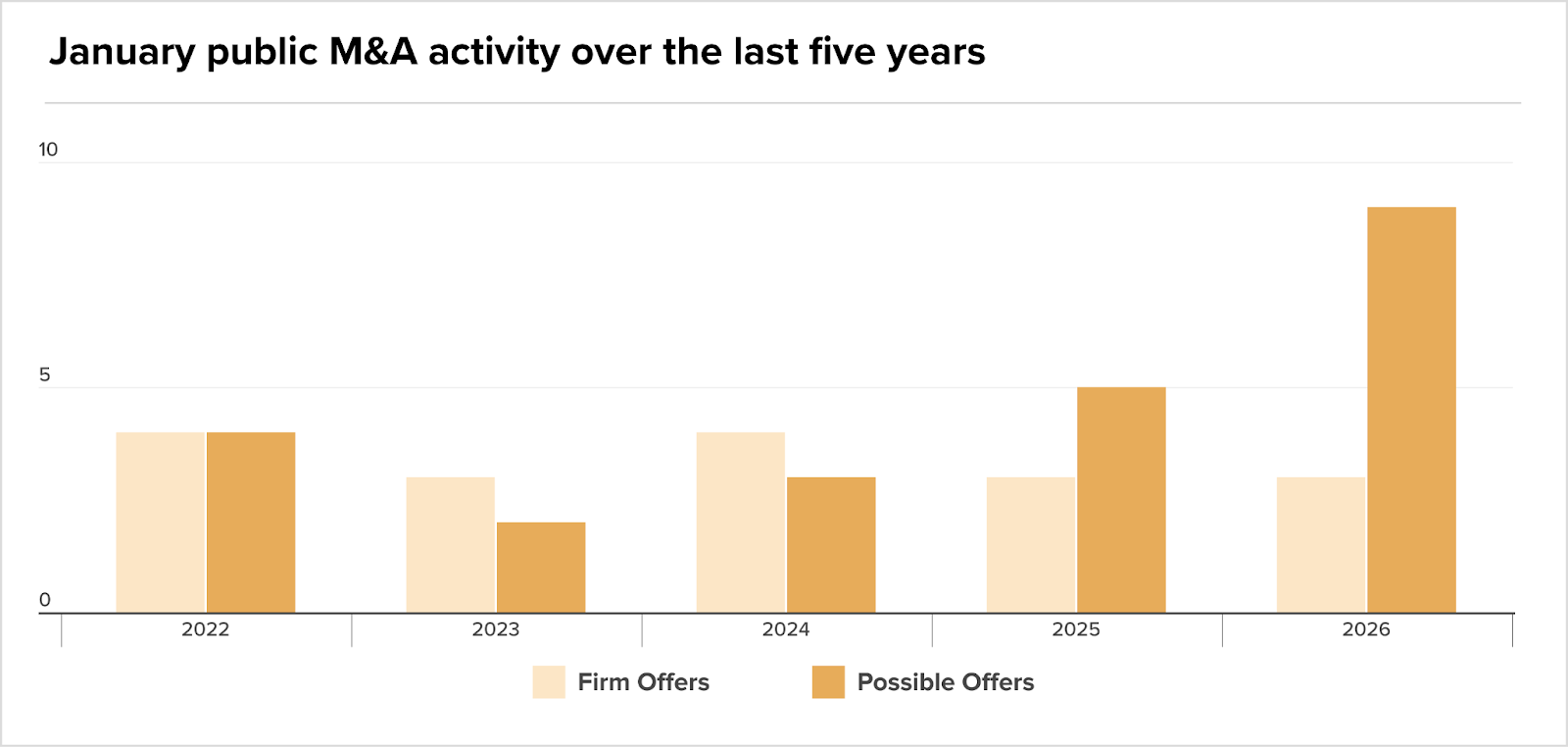

Breakdown of January deal activity

In the UK public markets, momentum is showing through. In January, there were three firm offers worth £488 million and nine possible offers. These included Zurich’s offer for Beazley and Rio Tinto’s offer for Glencore.

At the same time, the regulatory landscape is changing. By suggesting modifications to phase 2 decision-making procedures and more precise jurisdictional thresholds for share of supply tests, the government’s consultation on CMA reform seeks to bring speed and predictability to the merger regime. Timelines for phase 1 remedies would be extended from 10 to 20 working days, providing more room for remedy negotiations without requiring a more thorough review.

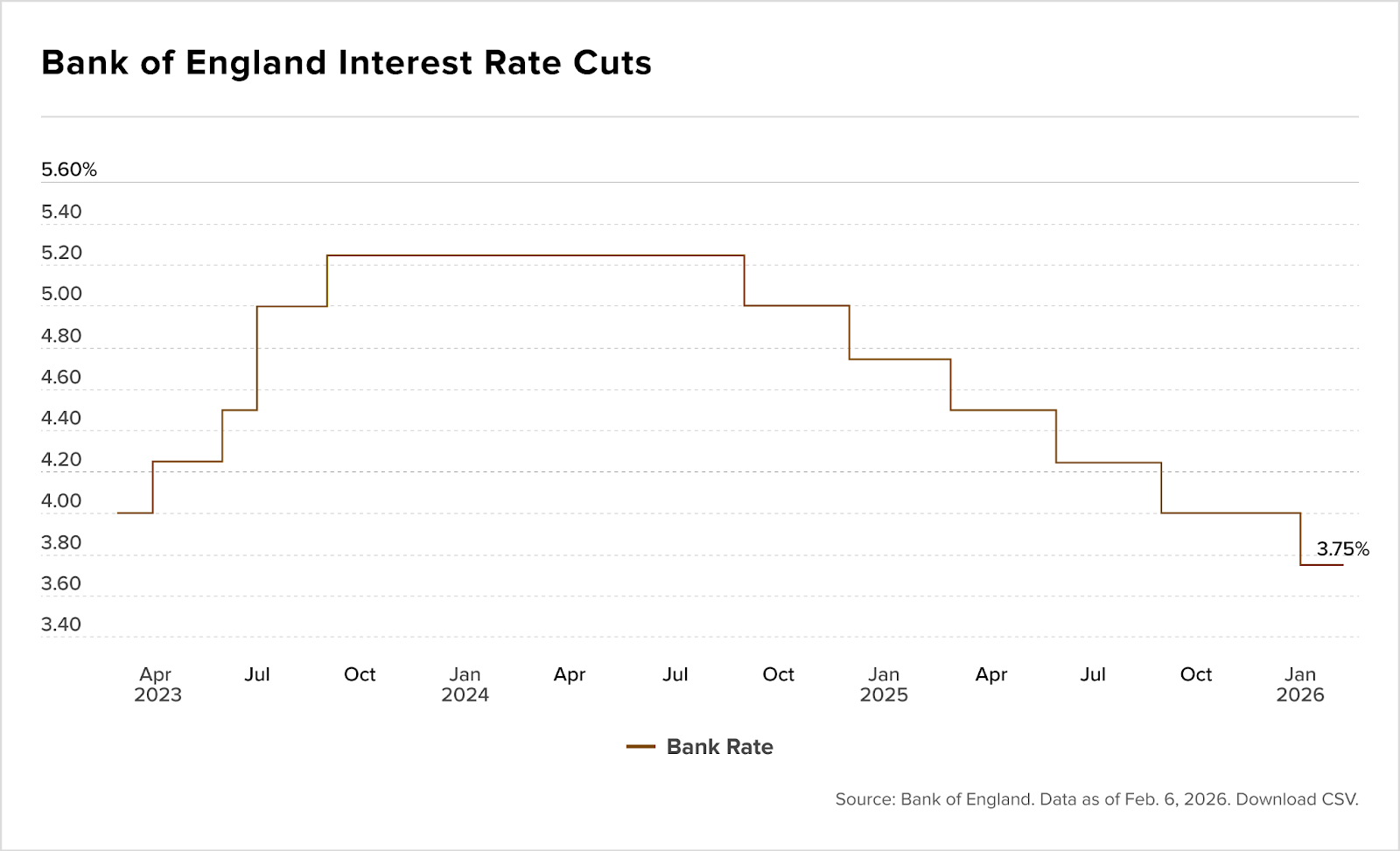

Rate cut on the horizon?

The financing backdrop is showing incremental improvement, according to Morningstar. Markets now assign a 65% probability to a March rate cut, bringing the bank rate down to 3.5%, with a second move expected in June.

That’s a shift from expectations at the start of the year, driven by inflation tracking towards the 2% target by April rather than later in Q2. Governor Bailey’s emphasis on “good news” in the data suggests the Monetary Policy Committee is growing more comfortable with the disinflationary trajectory, though the five-to-four split on holding rates in February underscores continued caution.

Fundraising

IPOs