Daniel Black

Daniel Black

There’s been an interesting twist in DMGT’s takeover of the Telegraph Media Group. The FT reported this week that a consortium led by Dovid Efune and Axel Springer has made a rival bid on more favourable financial terms.

Whether it’s enough to get RedBird back to the negotiating table remains to be seen.

In other news this week:

- LSEG plans £3bn of share buybacks as AI fears mount

- HSBC dealmaking fees edge up 3% despite M&A retreat

- Schroders chief vows to keep wealth manager Cazenove after £9.9bn takeover

Thanks for reading, and connect with me on LinkedIn if you want to discuss how Ideals VDR can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Royal London Asset Management chief: Schroders sale to Nuveen ‘a loss for the UK’

- Schroders could raise £2.4bn if it sold Cazenove after Nuveen tie-up

- LSEG plans £3bn of share buybacks as AI fears mount

- Efune consortium willing to improve offer for Telegraph Media Group

- NatWest plans risk transfer tied to CRE loans amid M&A push

- Shell in talks with Adnoc, others over Australia LNG stake sale

- HSBC dealmaking fees edge up 3% despite M&A, ECM retreat

- Oaktree said to weigh sale, IPO of £2bn UK wealth manager Utmost

- Honeywell cuts Johnson Matthey deal price to £1.325bn and sets new 2026 closing window

- GSK secures potential ‘multi-blockbuster’ drug in $950mn deal

- Engie jumps after £10.5bn deal to buy UK power networks

- Top banks miss out on Li’s $14bn sale of UK power to Engie

- Revolut weighs share sale later this year on pre-IPO demand

- Anglo American halves value of De Beers diamond business

- Schroders chief vows to keep wealth manager Cazenove after £9.9bn takeover

- Drax Rises to 20-Year High After Earnings Beat Expectations

- LSEG and European exchanges mull bids for key UK stock trading data contract

- Ampyr Solar Europe snaps up 530-MWp solar project in UK HSBC kicks off Singapore insurance business sale, eyes over $1bn value

- Verdane makes £186m bid for Augmentum Fintech

- Accenture to buy Verum Partners

- Chrysalis looks to drop managers as UK fund sells assets

Industry news

- How Santander plans to avoid US ‘graveyard’ for European banks

- UK warns tariff retaliation is an option if US reneges on trade deal

- Elliott tells UK it won’t seek LSEG break-up or New York listing shift

- Private Equity ratchets up its bet on London Office Refurbs

- UK swings to record £30bn budget surplus in January as retail sales surge

Salaries and bonuses

Job moves

- HSBC has both empowered its people with AI and hired 1,800 technologists

- HSBC’s pre-bonus equities job cuts are fine news for the survivors

- Rothschild taps ex-HSBC managing director as head of market structure

Market trends

PE health check

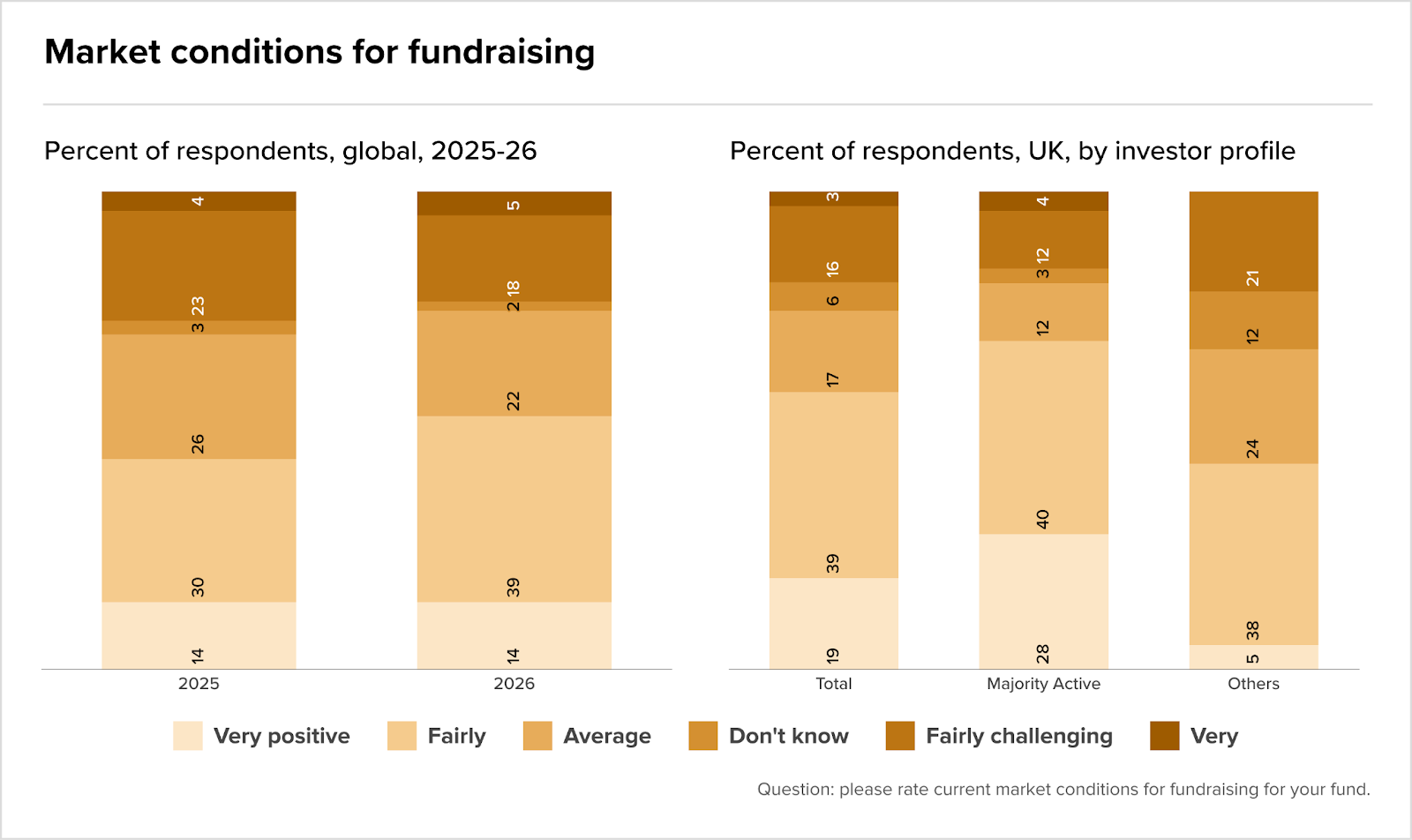

Globally, positive perceptions of fundraising conditions have risen nine points year-on-year, with 58% of UK private equity professionals now viewing the environment favourably, as reported by Forvis Mazars.

At the deal level, however, the same market is creating friction: 59% of UK PE firms say that financing conditions have impacted their buy-and-build strategies, and 51% mention the same pressure on exit timing.

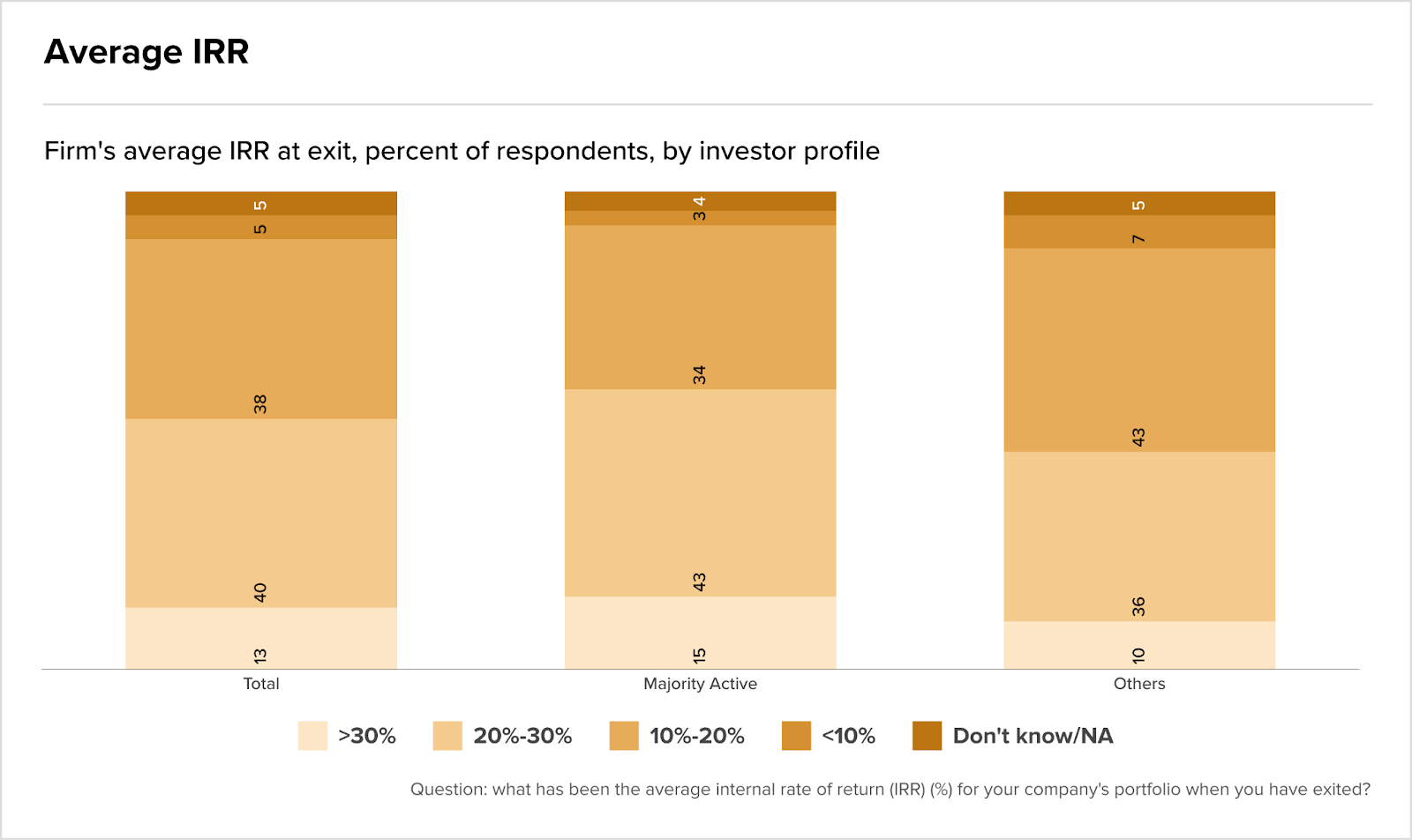

Performance holds up nonetheless. Some 53% of UK firms are generating internal rates of return above 20%, tracking modestly ahead of global peers, with portfolio outperformance relative to expectations outweighing underperformance both at the three-year mark and at exit.

The IRR data tells a similar story. Majority active investors are more likely to clear the 20% return threshold at exit, with 58% achieving this compared to 46% among other investor types. Hands-on ownership, it seems, continues to earn its premium.

M&A in distressed circumstances

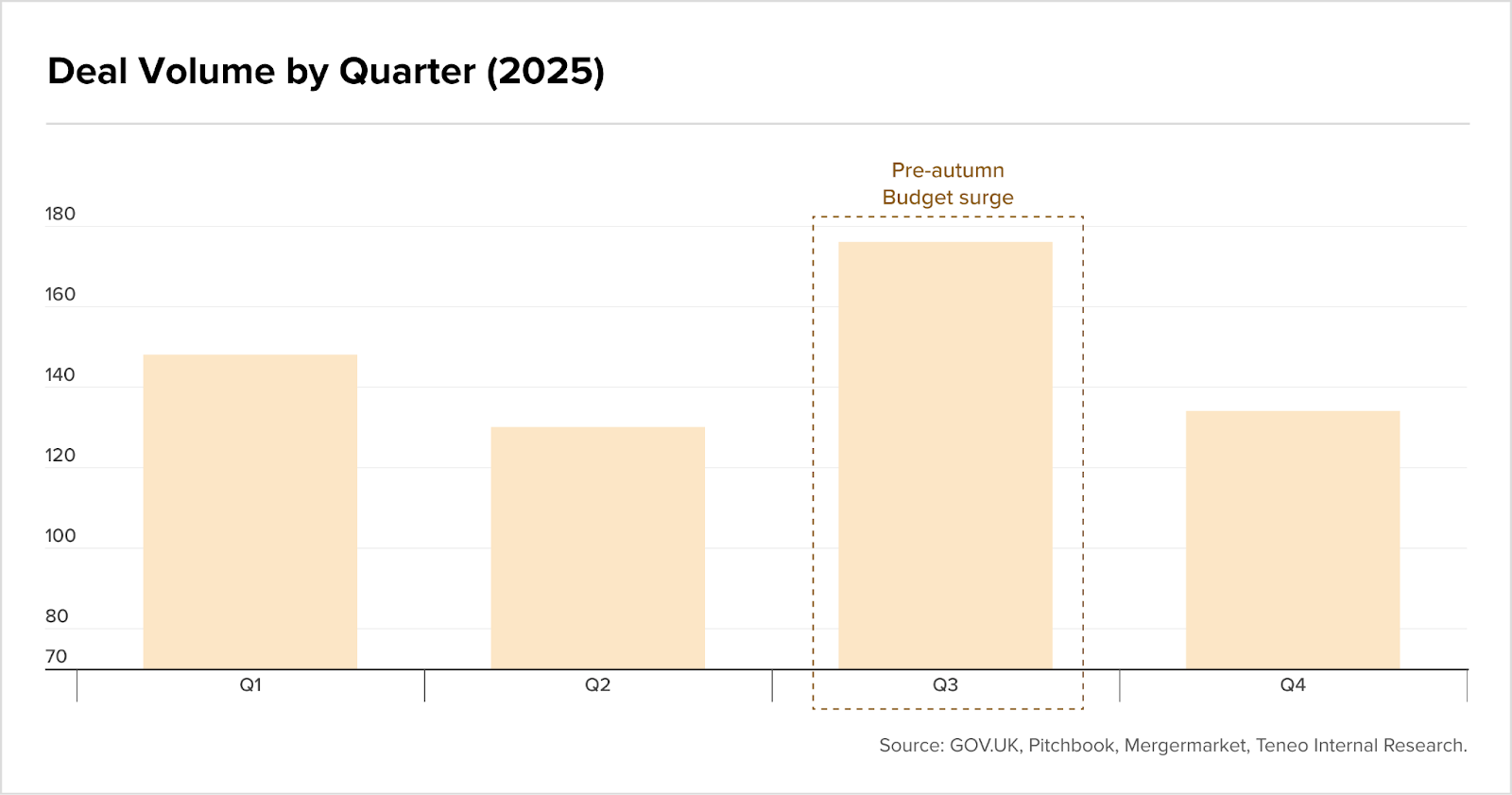

According to Tenoe, over 600 special situations deals were completed in the UK during 2025, underpinned by a combination of operational stress, failed conventional sale processes and urgent liquidity requirements. Corporate carve-outs added further volume as larger groups accelerated disposals of non-core assets, while Q3 activity surged notably ahead of the autumn Budget.

The aggregate impact is significant. Across the year, distressed transactions preserved an estimated 73,000 jobs and generated £1.7bn in cash proceeds for stakeholders. With financing conditions remaining tight and valuation gaps still wide in parts of the market, the conditions that sustained this level of activity show little sign of easing into 2026.

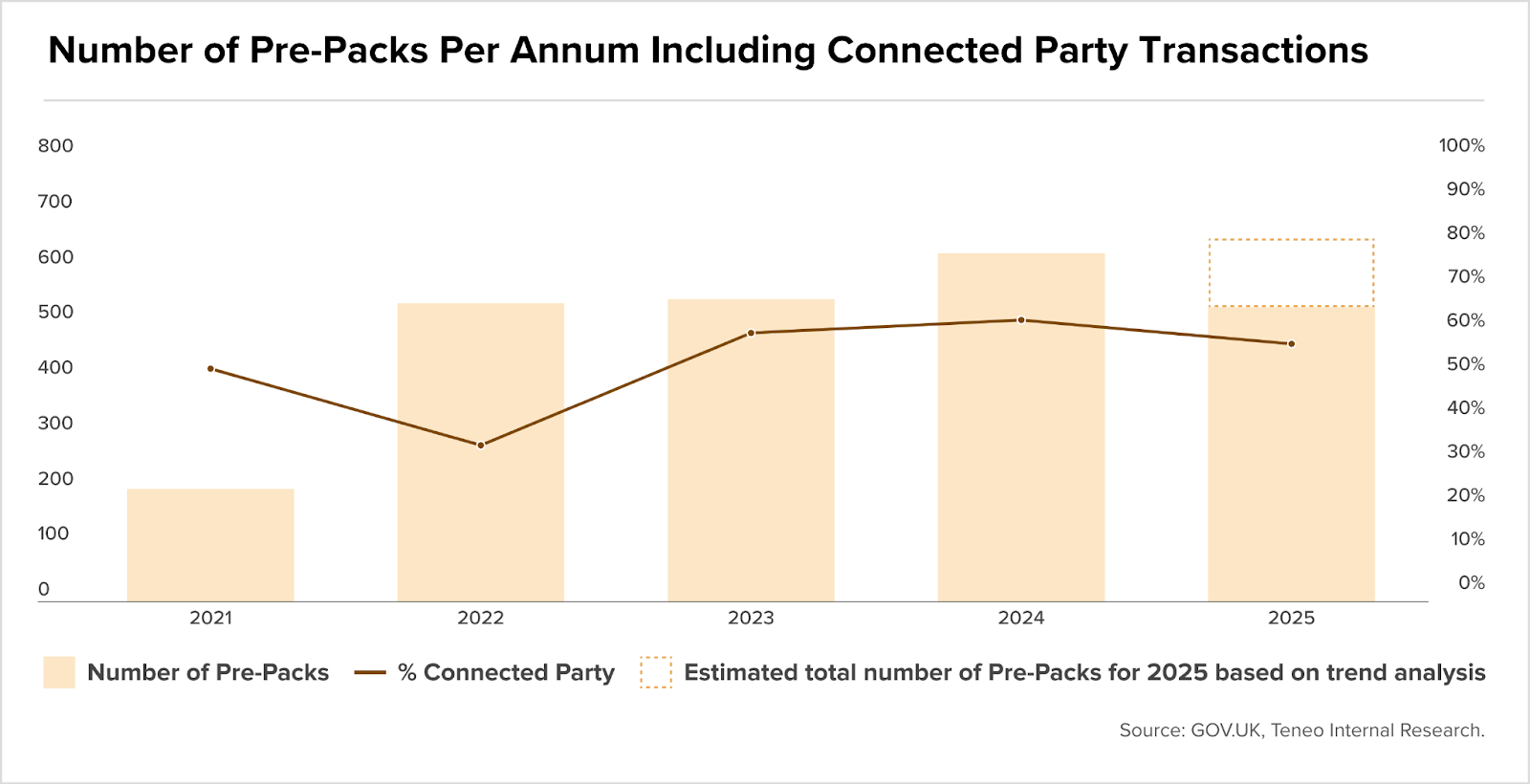

Insolvency-led structures accounted for the majority of that activity, generating over £600m in cash proceeds to stakeholders. Within that, the pre-packaged insolvency mechanism has become the dominant delivery route, with an estimated 531 pre-packs recorded in 2025 and the full dataset yet to be released by GOV.UK. Volume has grown markedly since 2021, when just 201 transactions were completed.

Connected-party outcomes featured prominently in around 58% of insolvent pre-pack deals, spanning non-consensual restructurings, debt write-downs and loan-to-own strategies. The mechanism’s ability to preserve going concern value while minimising operational disruption continues to underpin its position as the restructuring route of choice.