Daniel Black

Daniel Black

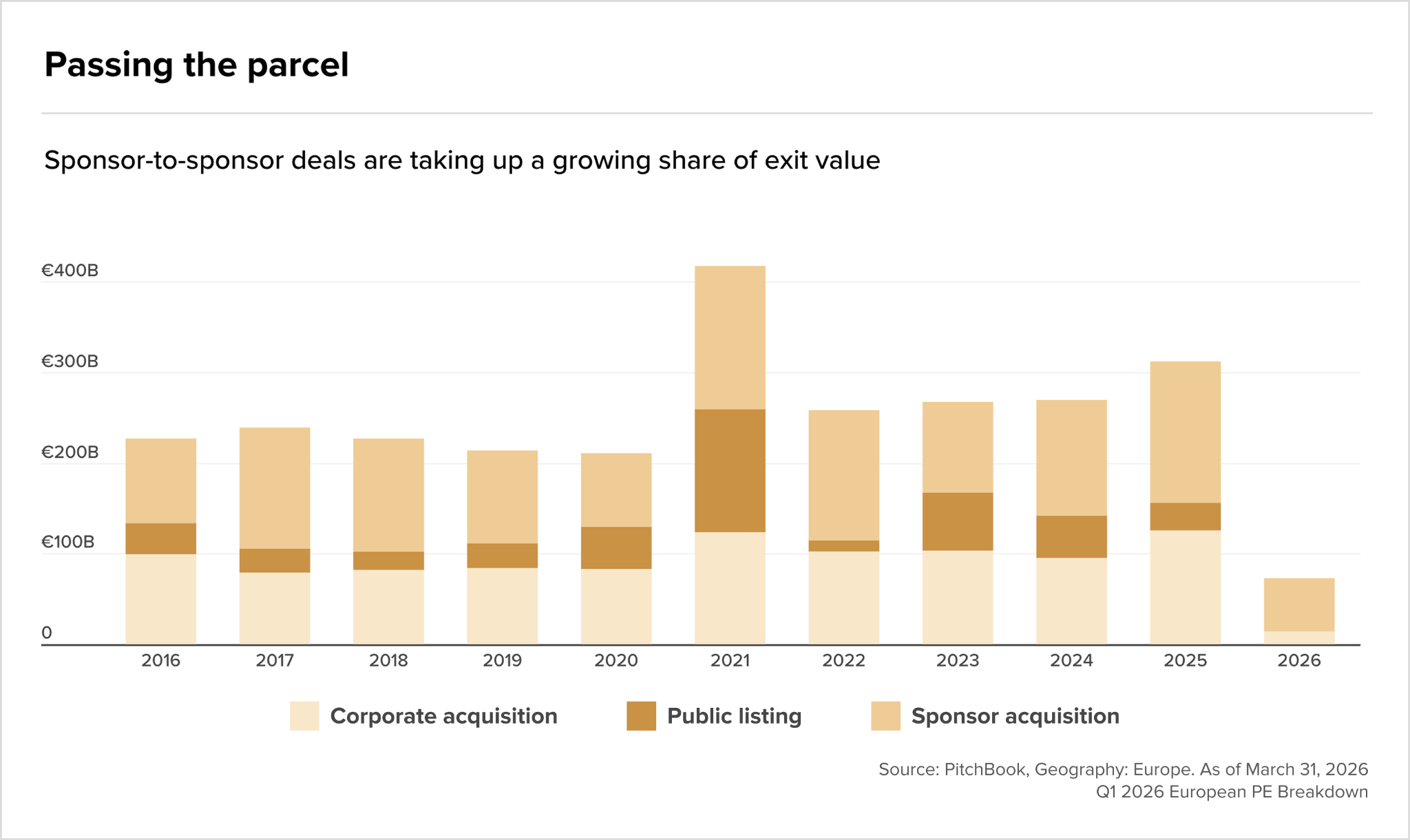

New data published this week confirms that PE firms are running short of exit options. According to PitchBook, sponsor-to-sponsor deals made up 76.1% of exit value in Q1 2026.

It also revealed that the number of exits dropped by 31.3% year-on-year. You can read more in the Market Trends section.

And in other news this week:

- Aegon is to sell its UK unit to Standard Life for $2.7bn

- Paramount Skydance’s deal for Warner Bros. will likely see a UK antitrust review

- JPMorgan gave its top London investment bankers a 19% bonus hike

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of confirmed M&A deals in the UK.

The rumour mill

- Axel Springer’s Telegraph deal waved through by UK government

- Perella Weinberg to buy London advisory boutique Gleacher Shacklock

- Pret A Manger owner books $6bn gain in 2025 from JDE Peet’s sale

- Aegon to sell UK unit to Standard Life for $2.7bn

- UK mulls Shutterstock’s editorial business sale for Getty deal

- BP to buy 60% stake in three Eco Atlantic PELs offshore Namibia

- Paramount Skydance’s deal for Warner Bros. expected to see UK antitrust review

- ESCO Technologies to buy Megger Group in $2.35bn cash and stock deal

- Perella Weinberg discloses stock consideration for Gleacher Shacklock deal

- Engie is said to eye divestments in US, France to fund UK acquisition

- UK’s Intertek mulls breakup to lift product testing firm’s value

- CVC said to seek Partners for €10.9bn Recordati deal

- UK signs drone interceptor deal with Cambridge Aerospace

- UK Tax Office opposes oil firm Waldorf’s debt plan in court

- Adnoc in Advanced Talks to Buy Shell’s South Africa Gas Stations

Industry news

Salaries and bonuses

Job moves

- HSBC’s top investment banker in Europe and the Americas set to depart

- Student Landlord Unite Hires Goldman to Ramp Up Asset Sales

Market trends

The roundabout PE market

Sponsor-to-sponsor deals accounted for 76.1% of European PE exit value in Q1 2026, up from 49.6% for the full year prior, as the IPO window stayed shut and corporate buyers retreated further amid the Iran conflict.

According to PitchBook, exit value fell 9.5% quarter-on-quarter, exit count dropped 31.3%, and what little activity occurred clustered at the top of the market, with 16 mega exits above €1bn capturing 67.9% of total value.

The UK offers a bright marginal spot. The first transactions on Pisces, the new regulated private trading platform, mark a structural development worth tracking. But with corporate buyers still cautious and the London IPO market showing little sign of reopening for PE-backed assets, sponsor-to-sponsor deals will remain the dominant exit route for UK managers throughout the year.

An AI-proof buying strategy

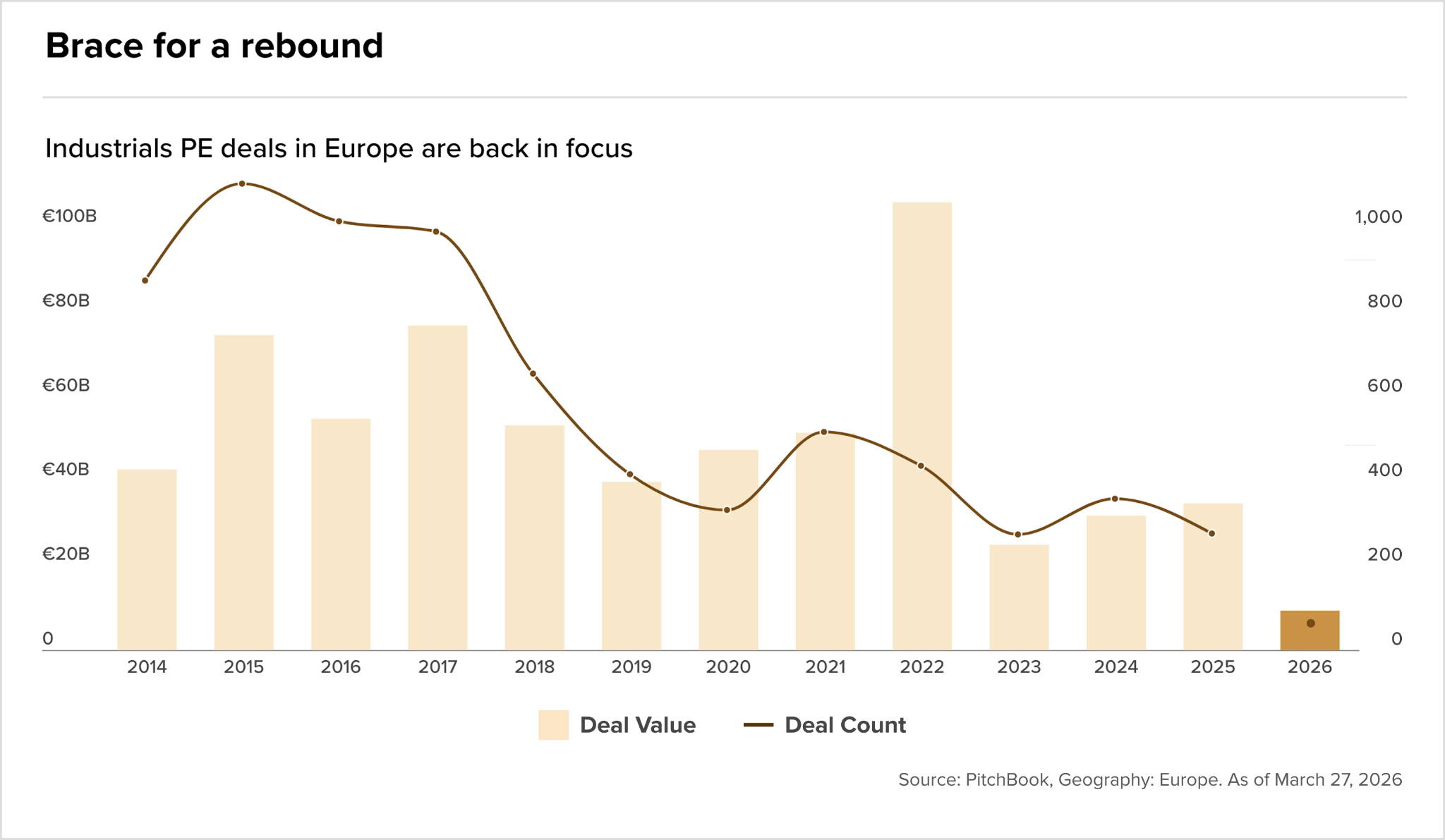

The exit scarcity is also reshaping where the capital goes next. With software valuations under pressure from AI disruptions, European PE is rotating back towards tangible assets, deploying €9.1bn into industrials in Q1 alone, backed by PitchBook data. Blackstone and Arcline are among bidders for British aerospace supplier Senior, while Brookfield, Blackstone and CVC have all submitted offers for Volkswagen’s shipping engines unit at up to €7bn.

The sector remains below its 10-year average by value, but deal activity rose 9% in 2025. The investment case centers on what some are calling HALO sectors, heavy assets, low obsolescence, a deliberate counterweight to software positions most vulnerable to agentic AI.

The $5 trillion silver lining

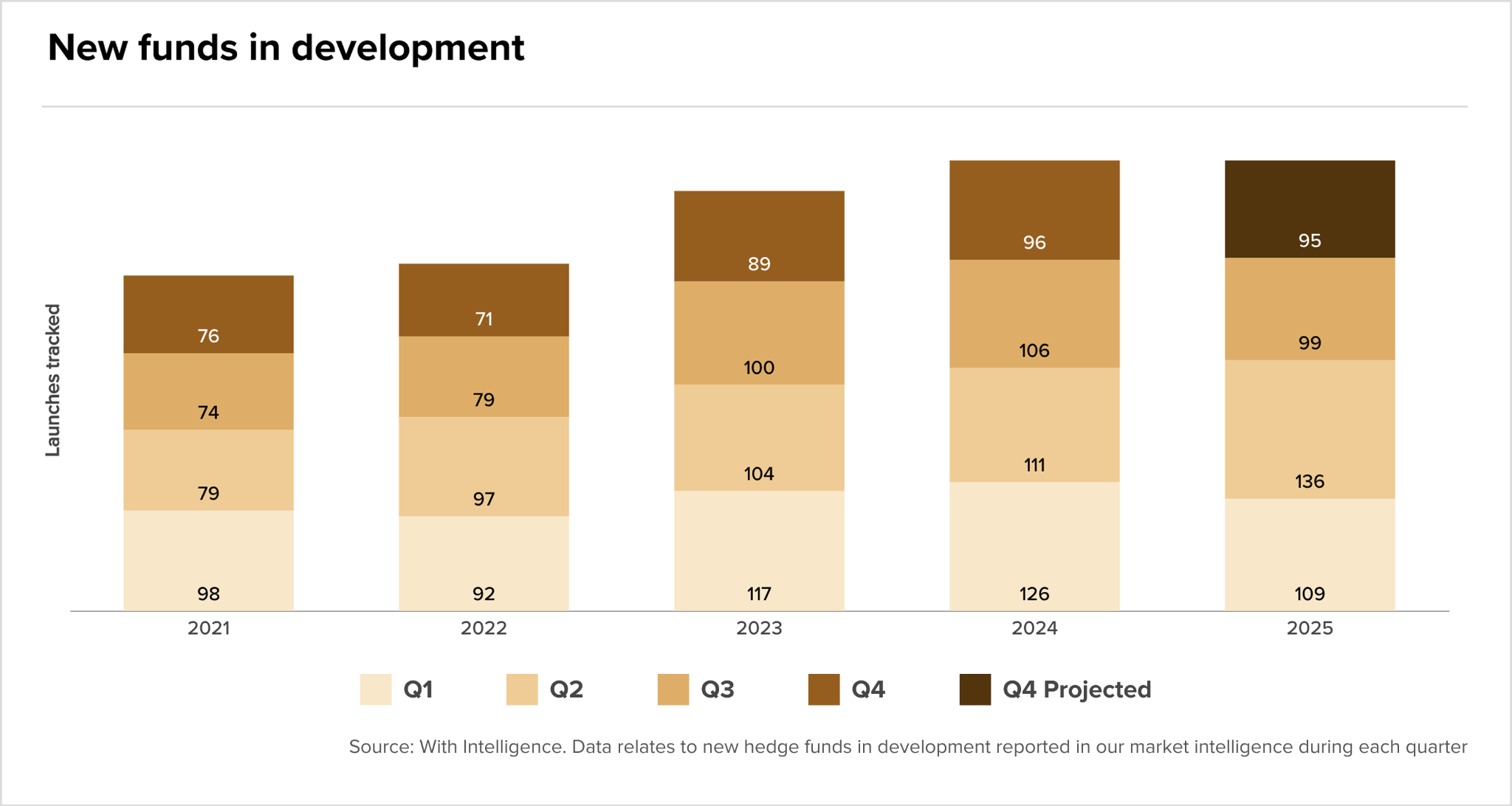

The same uncertainty suppressing PE exits is filling hedge fund order books. With 344 new funds tracked in development across the first nine months of 2025, the most since Covid, allocators are building out non-directional sleeves as a counterweight to volatile long-only positions, and multi-manager platforms remain oversubscribed.

According to With Intelligence, the industry is now on track to hit $5tr in AuM by end-2027, a full year ahead of where forecasters stood 12 months ago.

A short-lived rally for equity sellers

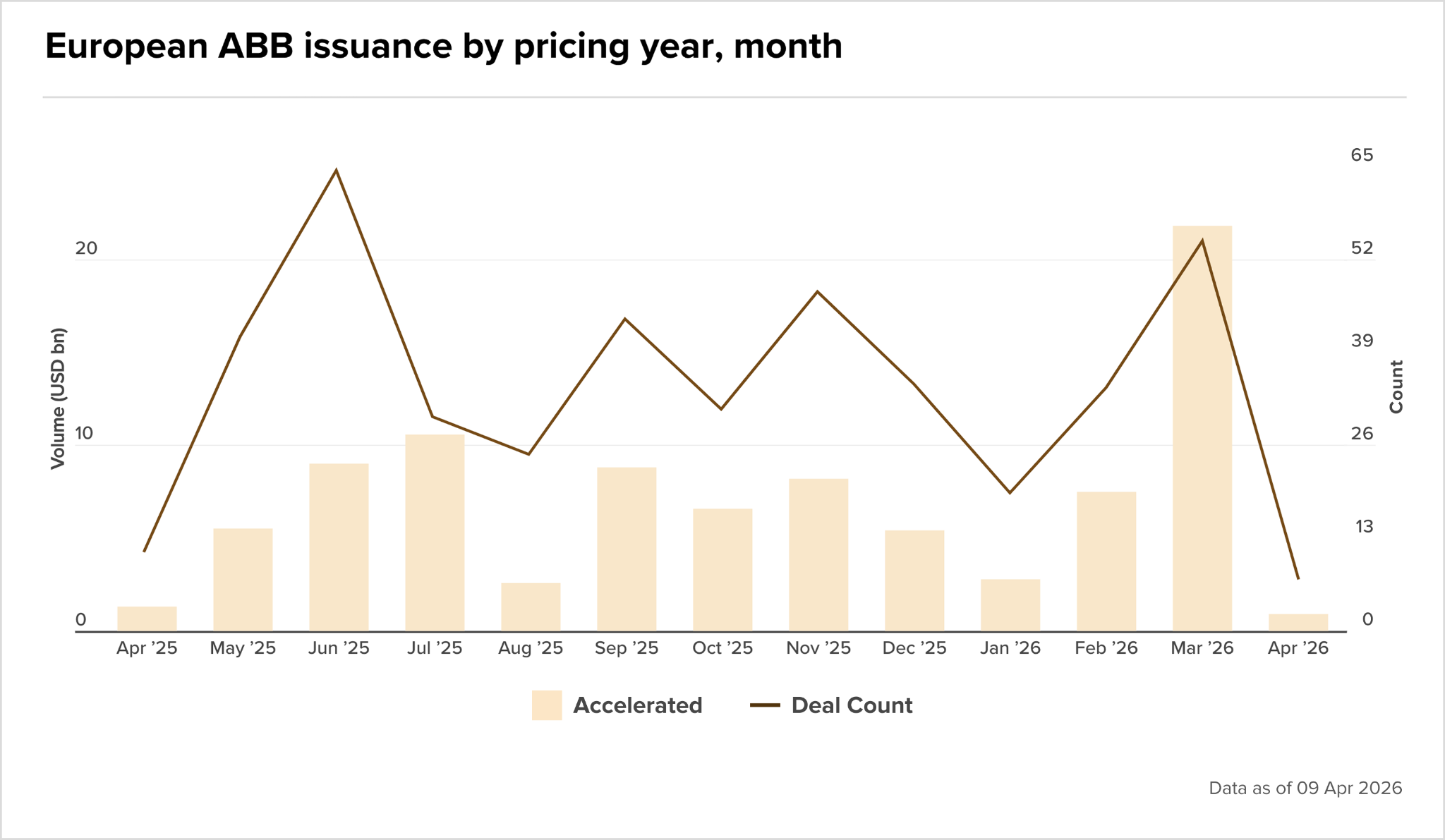

European ECM has settled into a rhythm of opportunistic bursts rather than sustained issuance, with the Gulf conflict dictating the pace. When a ceasefire announcement briefly lifted markets on April 8, sellers moved within hours: Cinven raised $445m from a block trade in Allegro, HLD disposed of a 4.42% stake in Exosens for €145m, and AMG Critical Materials printed a EUR 110.5m primary raise, all the same evening.

The March surge visible in the Dealogic data, the strongest month since June 2025 by both volume and deal count, reflected a similar dynamic, with sellers capitalising on a brief window.

IPOs