Daniel Black

Daniel Black

EQT isn’t taking no for an answer. After having its £9.3bn takeover proposal rejected by UK testing specialist Intertek, the Swedish PE firm came back this week with an improved offer worth £9.7bn.

If it goes through, it would be one of the largest take-private deals in the UK this year.

And in other news this week:

- AB Foods is to spin off Primark in a bid to unlock the group’s value

- Morgan Stanley hiked UK investment bank bonuses to £1.2m

- Private AI companies raised $226bn in Q1 2026 alone, more capital than in the entirety of 2025

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- EQT makes improved £9.7bn offer for Intertek

- William Hill owner in takeover talks with gaming operator Bally’s Intralot

- UK testing specialist Intertek rejects EQT’s £9.3bn takeover proposal

- Vattenfall to sell Muir Mhor stake to JV partner Fred. Olsen Seawind

- KeyCorp to acquire UK-based Clearwater Corporate Finance

- CVC is said to be frontrunner in Standard Life Pension Deal

- CVC Capital, GTCR bid to take medical device maker Teleflex private

- Aberdeen hit with net outflows of £2.9bn in first quarter

- VW is said to shortlist EQT Group, CVC, Bain for Everllence

- Jupiter continues positive flows with £1.5bn gathered during first quarter

- AB Foods to spin off Primark in bid to unlock group’s value

- HSBC is said to shortlist Allianz, Sumitomo for Singapore insurer

- US private equity firm TA Associates in talks to buy UK’s Advanced Medical Solutions

- Goldman Sachs-backed Doxa to acquire Eaton Gate Group

- William Hill UK owner Evoke weighs $304m takeover bid from Bally’s Intralot

- TA Associates in talks to take Advanced Medical Solutions private

- Schroders assets drop as market turbulence sparks more than £1bn of outflows

Industry news

- UK public sector borrowing hit £12.6bn in March as Iran war strains finances

- UK business activity rose more than expected in April

- Investment banks are facing a shortage of juniors after years of cuts

- LSEG boosts 2026 guidance as first-quarter revenue beats estimates

- New hedge funds target individual investors as 75% line up separate accounts

- Grant Thornton aims to leapfrog UK rivals in AI push

- Rothschild’s new UK wealth CEO makes first senior appointment

- UK could save £2.5bn by helping banks to buy gilts, says Barclays

Salaries and bonuses

- Goldman Sachs hikes pay for EU hubs by 19% after revenue bounce

- Morgan Stanley hikes UK investment bank bonuses to £1.2m

- JPMorgan hikes bonuses for top London investment bankers by 19%

Job moves

- Hedge fund Jain Global is hiring quants in London

- Rising hedge fund paying $1m in London hired an ex-Balyasny quant

- Barclays taps Jefferies dealmaker Yildiz to co-head European financial sponsors

Market trends

The British-German corridor

Two of Europe’s largest economies are growing, just not in any way that inspires confidence.

German GDP grew just 0.2% in 2025; the UK managed 1.3%, though the IMF now puts both on the same footing for the year ahead at 0.8%.

Neither the ECB nor the Bank of England moved rates in March, citing energy-driven inflation that remains stubbornly above target on both sides. With the BoE sitting at 3.75% against the ECB’s 2%, the rate differential continues to shape cross-border financing structures and relative asset valuations for acquirers working the corridor.

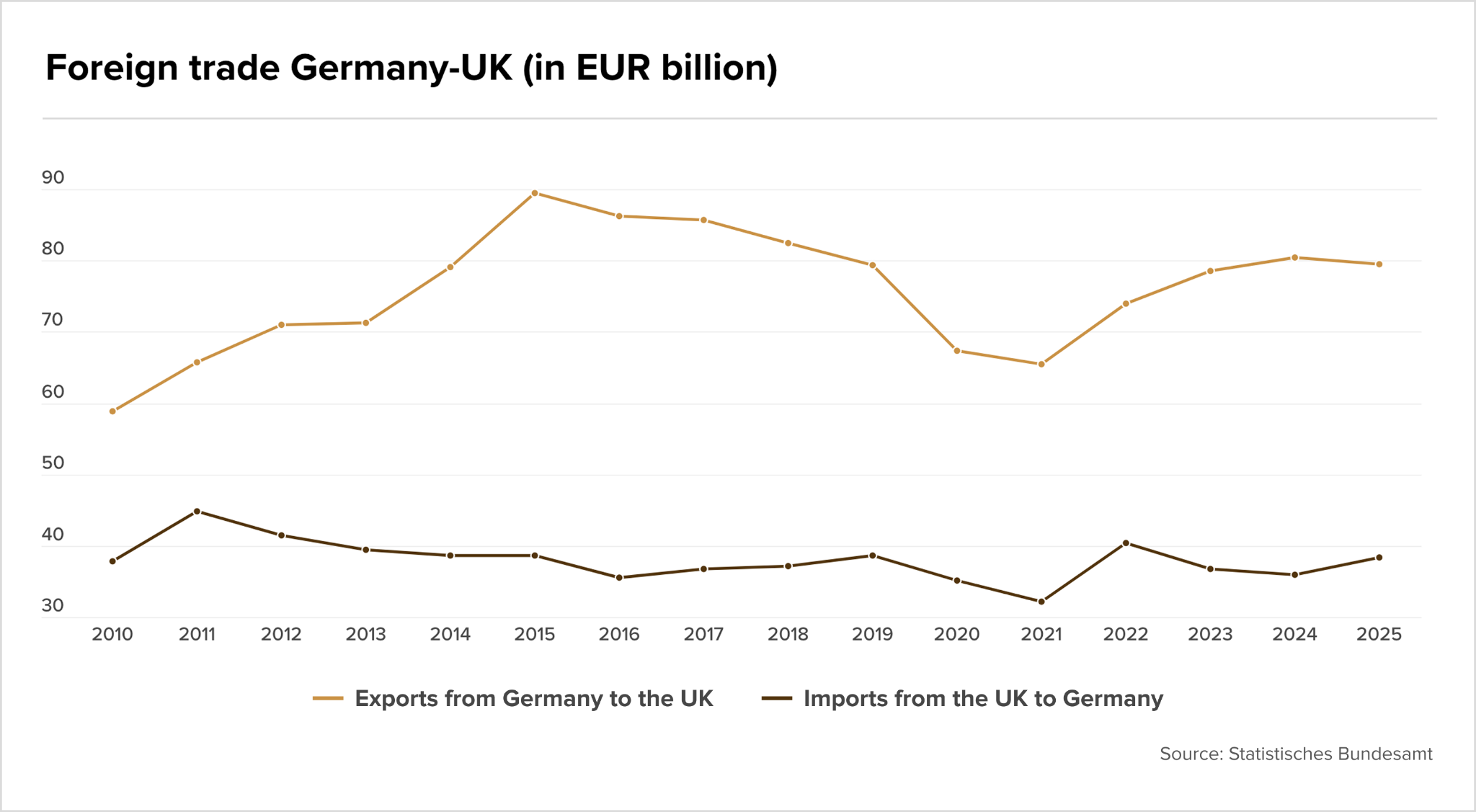

The trade relationship has quietly held up well. KPMG reports that bilateral volume reached €118bn in 2025, the fourth consecutive year of modest growth, with Germany running a €41bn surplus.

For deal professionals, the more telling signal is on the capital side: UK inward FDI has fallen to a historic low of 0.1% of GDP, while Germany’s own inflows have been declining steadily since 2020. Neither market is drawing the foreign capital it once did.

On the fiscal side, the UK’s debt-to-GDP ratio of 102.3% versus Germany’s 62.9% leaves Berlin with meaningfully more room to deploy stimulus, a gap that will increasingly influence where sponsors and strategics choose to anchor platform assets.

Media and marketing comeback quarter

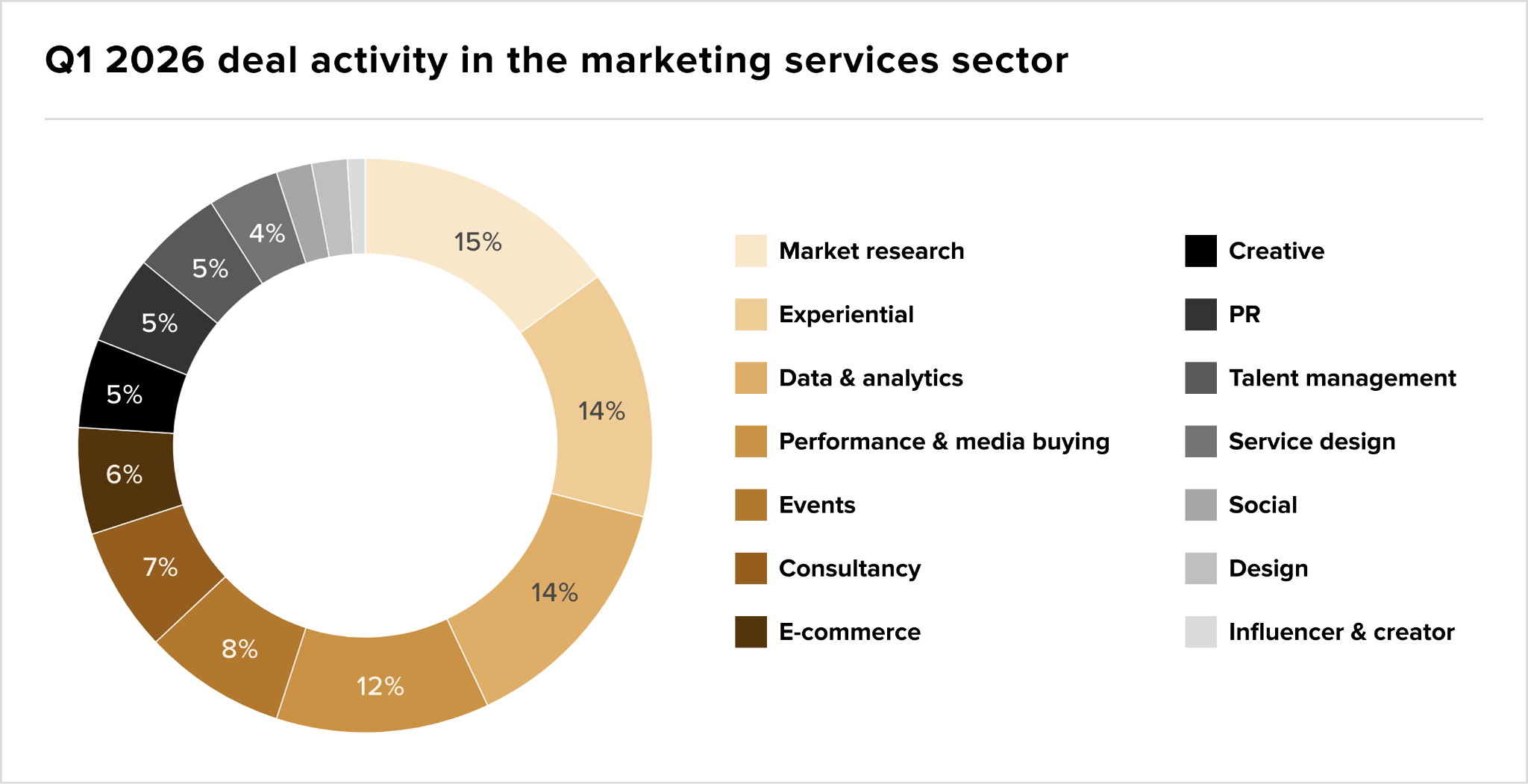

After a bruising 2025, deal volumes in the UK’s media and marketing services sector have snapped back hard. According to Moore Kingston Smith, Q1 2026 recorded 118 completed transactions, more than double Q4’s 57 and the strongest quarterly figure since early 2023.

PE drove the bulk of it, backing 54% of deals, with technology-first marketing businesses accounting for more than a quarter of activity as buyers kept their focus firmly on data and digital capability over traditional agency exposure.

Market research led all subsectors, claiming 15% of transactions after barely registering in Q4. Geopolitical uncertainty has a way of making consumer intelligence feel less discretionary. US acquirers acted on that, targeting UK firms with AI-enhanced research capabilities that travel well into North American portfolios. The pace may not hold as rate cut hopes fade and Middle East disruption feeds into costs, but deal appetite across the sector remains broad.

The warm-up was 2025

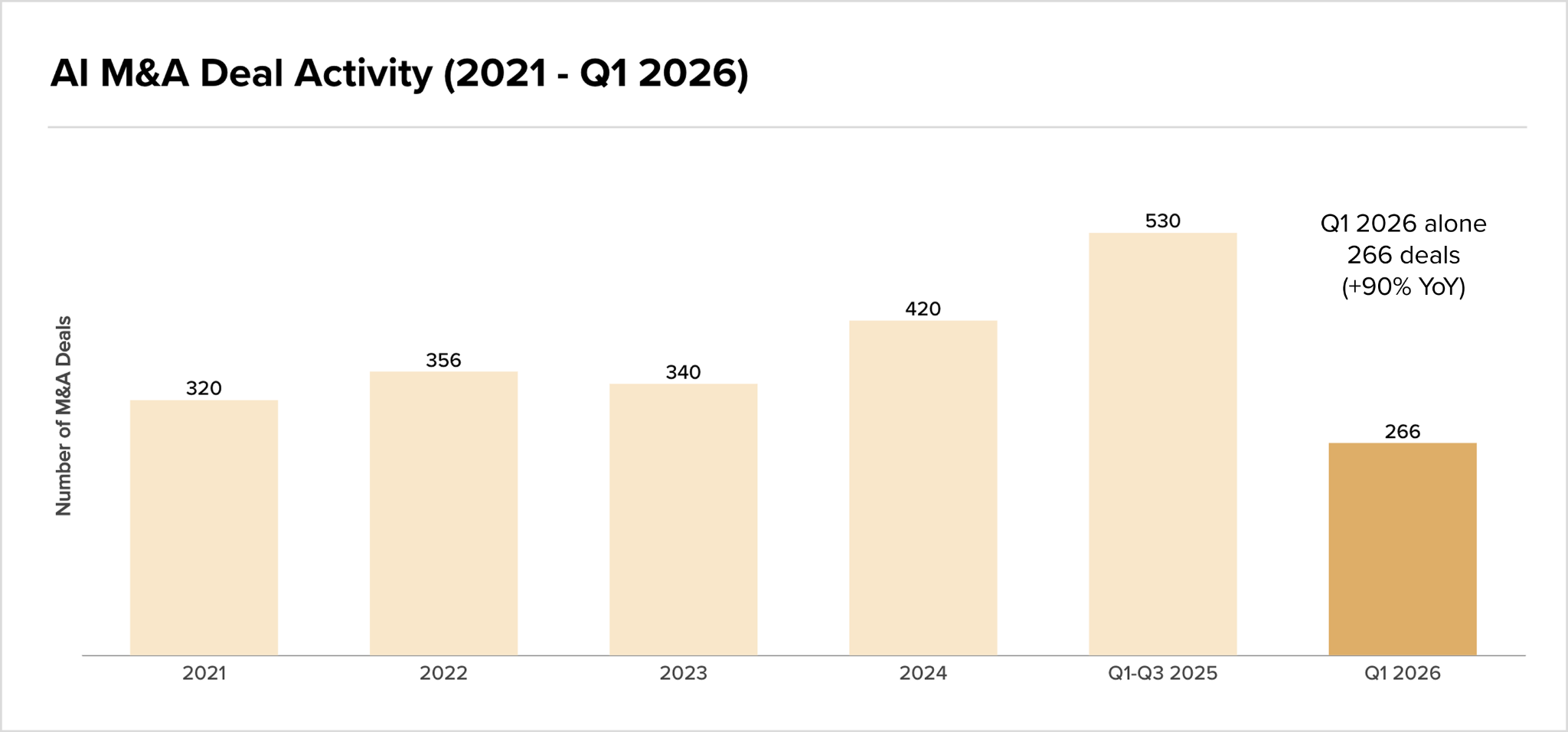

The numbers are moving past the point where they need much commentary. Private AI companies raised $226bn in Q1 2026, which is more capital than in the entirety of 2025. Global tech M&A jumped 77% in 2025 to roughly $1.08 trillion, with AI-related targets accounting for nearly half of all strategic deal value above $500m, up from 25% the year prior. Q1 2026 produced 266 AI deals, a 90% year-on-year increase.

US private AI investment reached $109bn in 2024, nearly 12 times China’s and 24 times the UK’s. Morrison Foerster’s survey found 57% of technology dealmakers expect volumes to rise further over the next 12 months, with AI capability ranked as the top acquisition priority.

Fundraising

- Bridgepoint said to raise €6bn at new fund’s first close

- Baird Capital raises $450m for private equity fund

IPOs