Sebastian Montoya

Sebastian Montoya

Europe’s clean-energy private equity cycle is entering a new phase. PitchBook’s latest data reinforces the shift in value observed in previous quarters.

Dealmakers are moving beyond pure capacity build-out towards the infrastructure, platforms and system-level capabilities that enable electrification at scale. We bring you the details in this week’s analysis.

Also, don’t miss the deals of the week. The highlights include:

- Orrön Energy agreed to sell a 91 MW ready-to-build solar project to Gülermak Renewables for up to €5.6m, implying a steep discount at €61.5m/GW and underscoring ongoing compression in early-stage solar valuations.

- Plenitude completed the €500m acquisition of Acea Energia from ACEA, adding around 1.2 million customers and reinforcing its downstream strategy, where scale in retail supply is increasingly central to value creation.

- KGAL and PtX Development took a majority stake in Lhyfe’s 800 MW green hydrogen project in Lubmin, with expansion potential to 1.7 GW, backing a capital-intensive platform aligned with Europe’s industrial decarbonisation push.

Want more insight? Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Energy M&A in Iberia: Cocktails and connections

The Iberian energy market continues to lead the way in the European transition, driven by significant investment in renewables and a robust pipeline of infrastructure projects.

Join the M&A Community and Ideals for an exclusive networking evening at Casa Suecia. We’ll gather to discuss the evolving landscape of the Spanish energy sector at this stylish venue in the centre of Madrid.

Deals breakdown

From Capacity to Connectivity: Europe’s next clean-energy PE cycle

Human abstraction remains one of our greatest advantages. As technology accelerates and machines grow better at identifying patterns, people still stand apart in one essential way: the ability to connect disparate signals, interpret them in context and see the system behind the data.

PitchBook’s latest clean-energy PE data suggests that the European opportunity is moving towards that mindset. Investors are looking beyond capacity build-out alone and paying closer attention to the wider architecture that makes electrification viable: the infrastructure, platforms and operating models that allow the system to function as a whole.

That shift matters. In 2025, clean-energy PE deal value reached a new peak for the sector at USD 47 bn, up 9.7% from USD 42.8 bn in 2024, while deal count rose from 72 to 87, a 20.8% increase, albeit still below the 100 deals recorded in 2023.

More notably, PE growth deal value exceeded buyout/LBO value for the first time on record, with growth capital rising 129.7% year on year to USD 22.9 bn and buyouts’ share of annual deal value falling to 45.8%.

While PE growth has outnumbered buyouts by deal count in every year since 2018, 2025 marks the first time it has overtaken them by value. On its own, that is a meaningful global market signal. Through a European lens, it looks even more revealing: capital is leaning away from static exposure and towards platforms with room to expand, integrate and compound.

For Europe, this is more than a financial curiosity. It goes to the heart of where the transition now stands.

The continent has already proved it can deploy renewables at scale. The harder question now is not whether more clean capacity can be built, but whether the wider system can absorb it, balance it, move it and monetise it.

In other words, the challenge is becoming less about isolated megawatts and more about system logic. Pitchbook’s data points that the money is beginning to follow the infrastructure layer behind electrification in a faster and more concise way, not just the headline assets in front of it.

Europe’s opportunity is shifting from assets to architecture

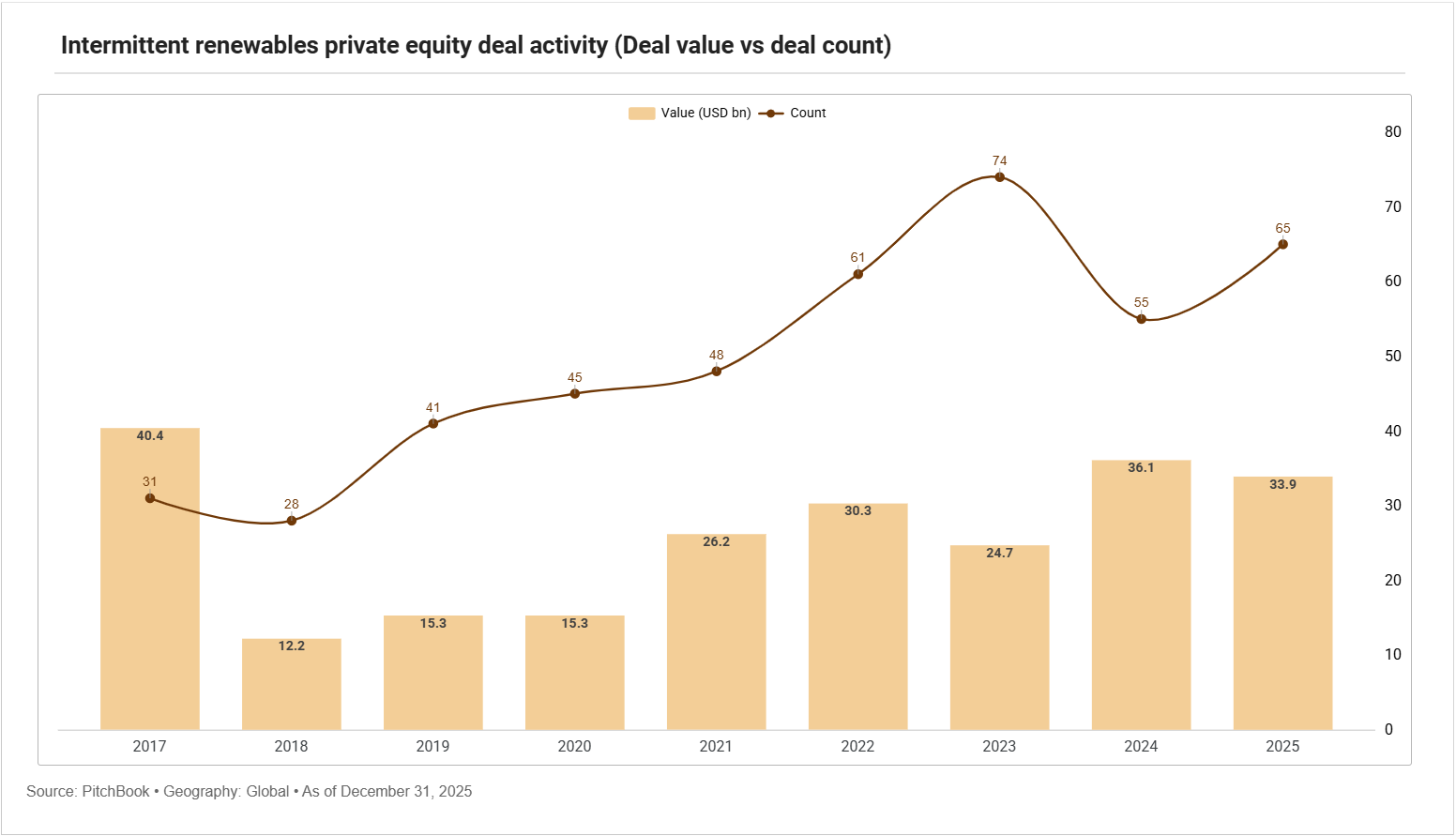

PitchBook identifies intermittent renewables and grid technologies as the two largest segments of the clean-energy PE market by both deal count and value.

That pairing says a great deal. Intermittent renewables still dominate, as would be expected in a mature market built around solar, wind and mixed-renewables platforms. But the analyst note also highlights grid technologies as the standout segment for consistency, with deal count and deal value rising steadily since 2018 and reaching a peak in 2025.

The drivers are equally telling: renewable integration, electrification and the rapid build-out of datacentre capacity.

For Europe, that combination reads almost like an investment roadmap.

The region’s energy transition is increasingly constrained not by ambition, nor even by generation economics alone, but by connection queues, balancing requirements, network bottlenecks, industrial power demand and the broader complexity of cross-border energy systems. Europe does not merely need more clean electrons. It needs a more coherent machine for producing, transporting, storing and using them.

That is why the shift in growth capital feels so important. PE growth has long been prominent in clean energy by deal count, what changed in 2025 was its ability to match and then surpass buyouts on value as well.

The implication is that investors are not just acquiring mature cash flows, they are backing businesses with operational runway.

In Europe, that should favour companies sitting in the connective tissue of the transition: grid equipment suppliers, power electronics specialists, flexibility aggregators, distributed-energy operators, EV charging networks, storage integrators and software layers that help make a fragmented system legible and manageable. This is notable when we pay closer attention to the composition shift visible in Pitchbook’s global data.

PitchBook notes that the segment has consistently been the largest by deal value since 2017, accounting for between 47.7% and 84.7% of annual deal value, and that its scale reflects both its commercial maturity and its larger deal count.

Over the past five years, intermittent renewables averaged 60.6 deals annually, versus 26.2 for grid technologies, the next largest segment.

But the more interesting line is strategic rather than statistical: platform investments in solar and wind can be expanded through adjacent technologies such as energy storage, EV charging and energy-management systems, or through regional expansion. That is exactly the kind of layered thesis Europe now seems built for.

The next value pools may sit where the system is under the most pressure

If the first phase of Europe’s clean-energy story was about proving deployment, the next phase may be about proving orchestration.

That places renewable generation into a wider context. Solar and wind remain the backbone of the transition, but backbone assets alone do not resolve congestion, intermittency or rising power demand from transport, heating and digital infrastructure. Investors increasingly appear to understand that the real scarcity is not always generation capacity itself, but the infrastructure and operating model required to make that capacity useful at scale.

The quarterly pattern in PitchBook’s 2025 data reinforces the point that this is not a simple, risk-on rebound.

Activity was uneven. Deal value fell to a two-year low in Q2 2025 at USD 5.8 bn, then recovered progressively through Q3 and Q4, reaching USD 18.1 bn by year-end. Over the full trailing 12 months, exit count rose from 13 to 17, while public listings increased from 2 to 7. That suggests a market that is reopening selectively rather than indiscriminately.

Capital is returning, but it is choosing where to concentrate.

For Europe, that selectivity may favour the businesses that solve friction rather than merely participate in momentum.

It is also worth reading the global comparison carefully. PitchBook flags US policy headwinds in 2025, including tariff exposure on clean-energy hardware and changes to tax incentives that affected development economics. Europe has no shortage of its own policy complications, from permitting delays to regulatory fragmentation. Still, relative attractiveness matters in private markets.

If the US environment becomes more volatile on hardware costs and incentive visibility, Europe may look comparatively stronger for investors seeking durable infrastructure-linked growth, particularly where assets and platforms are tied to essential system needs. That is an inference rather than an explicit claim in the report, but it follows logically from the combination of US headwinds and the segments showing the strongest momentum.

At the same time, the note is a reminder that not every strategically important segment is ready for scaled PE deployment.

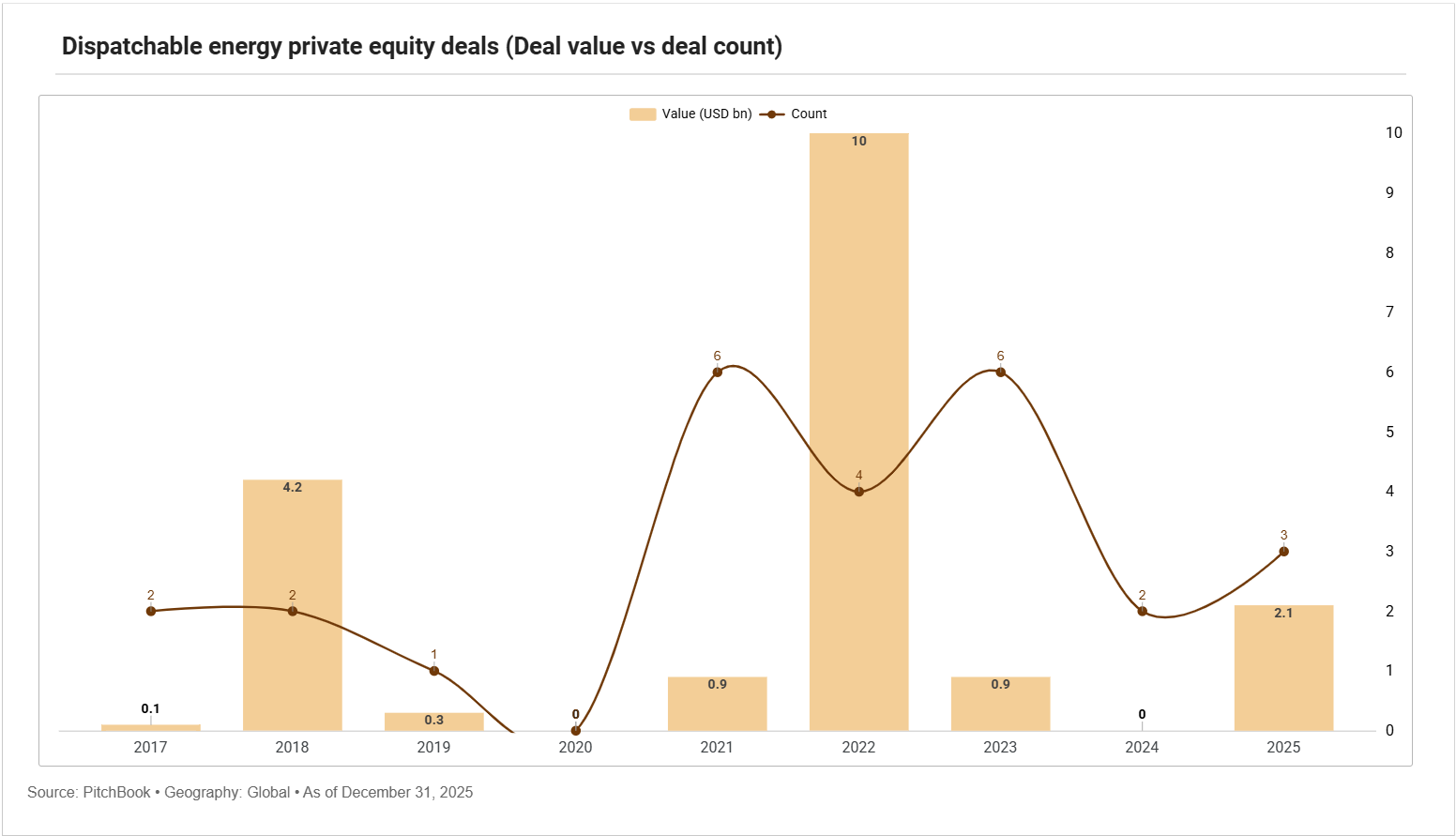

- Dispatchable low-carbon energy remains a much smaller category, largely because there are too few mature, post-revenue projects in areas such as geothermal and advanced nuclear.

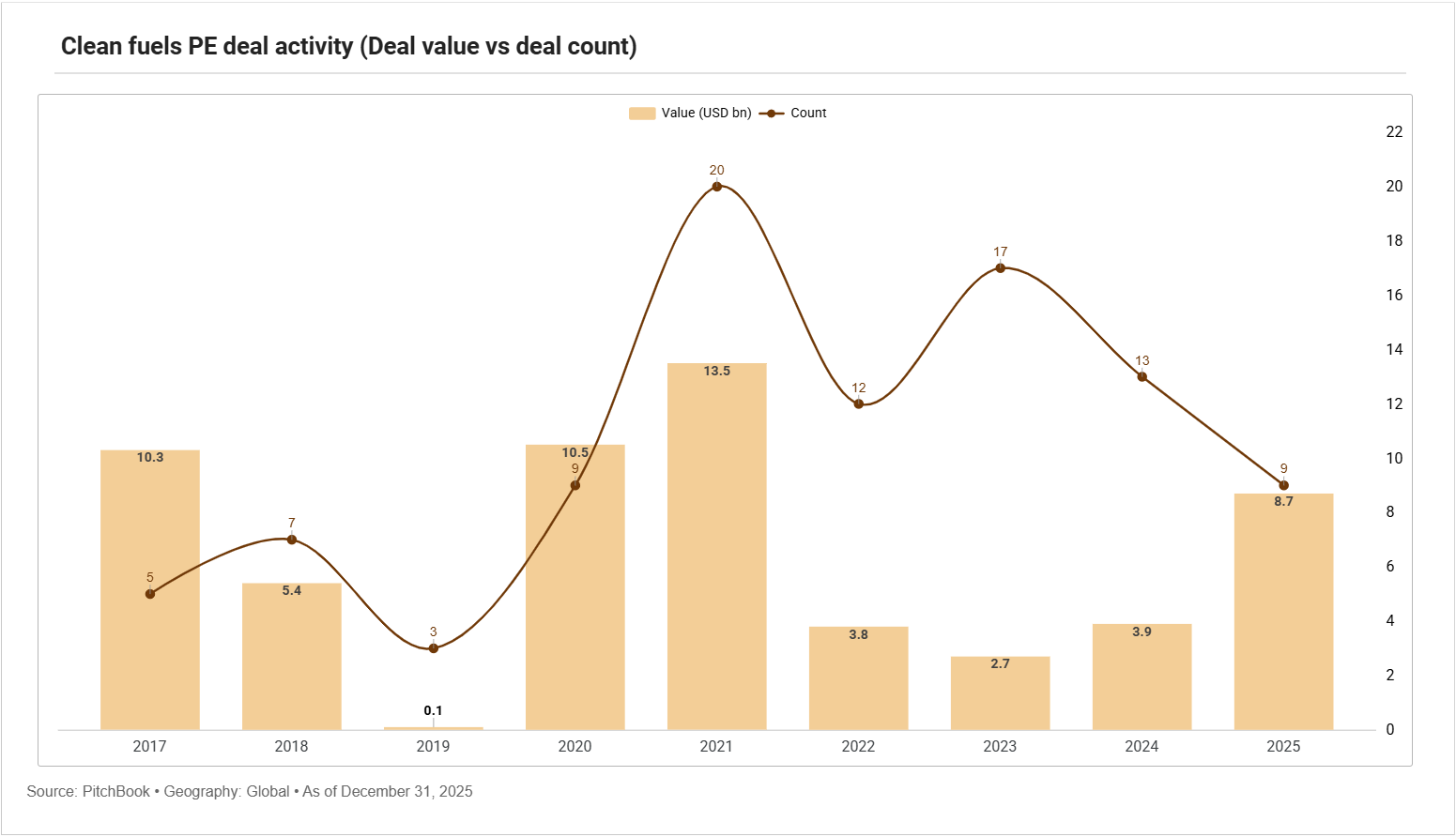

- Clean fuels also remain uneven, with waste-to-energy leading segment deal value while hydrogen faces headwinds.

Europe will almost certainly need a broader mix of dispatchable and low-carbon solutions over time. But private equity tends to move decisively once commercialisation, asset maturity and repeatable revenue are clearer. For now, the strongest conviction appears to sit in the technologies and platforms already solving operational constraints around a more electrified economy.

That, ultimately, is the deeper meaning behind the Pitchbook’s data. In Europe, the next clean-energy PE cycle may be defined less by the race to add capacity and more by the ability to read the transition as a system.

The market is beginning to value not only what can be built, but what allows everything else to function. If the opening insight is that human judgement lies in seeing the whole picture rather than just the data point, then Europe’s clean-energy market may now be asking investors to do exactly that.

Battery storage

- Denmark | Battery Investment Group consortium takes minority stake in BattMan Energy through triple-digit million DKK equity raise, funding 1 GWh battery storage portfolio rollout

- Germany | Akaysha Energy partners with Copenhagen Energy to develop mega-scale battery storage projects, advancing large-scale BESS deployment to support grid flexibility

- Germany | FP Investment Partners’ FP Lux fund acquires 50 MW/100 MWh battery storage project in Saxony, marking first investment to build European storage portfolio

Multiple

Retail/Grid Network

Solar

- Germany | Orrön Energy sells 91 MW solar project to Gülermak Renewables for up to €5.6 m, advancing greenfield monetisation while retaining development through ready-to-build

- Italy | Iberdrola agrees to acquire 42 MW solar PV plant in Lazio from CCE, expanding Italian renewables portfolio and integrating asset into Etruria complex

Wind

- Germany | ENOVA acquires project rights to 21 MW share of Thüle onshore wind farm from Jade Concept and landowners, advancing regional expansion alongside project financing

- Ireland | Infracapital acquires majority stake in Farra Marine to expand offshore wind vessel fleet, supporting growing European demand for CTV services