Daniel Black

Daniel Black

DCC has rejected a £5bn takeover approach from KKR and Energy Capital Partners, according to the FT. The rejection is the latest example of UK-listed boards holding firm on valuations, even as PE firms push harder to deploy record levels of dry powder.

It comes in a week where EQT is also reportedly preparing an improved bid for Intertek after its initial offer was turned down, and Kone has struck a €29bn deal for TK Elevator in one of the largest industrial transactions of the year.

And in other news this week:

- Eon is nearing a £600m deal to buy UK energy supplier Ovo

- Lloyds profits soared 33% as higher interest rates boosted income

- The RAC has pumped the brakes on its planned £5bn London IPO

Thanks for reading, and connect with me on LinkedIn if you want to discuss how Ideals VDR can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- EQT said to prepare improved takeover bid for UK’s Intertek

- DCC rejects £5bn takeover bid from KKR and Energy Capital

- Investors pull another £1.7bn from Terry Smith’s flagship fund

- Mayer Brown sees London revenue jump 20% to record level

- Vanguard’s UK platform assets swell to £42bn as younger investors fuel growth

- Latham & Watkins London boss eyes City expansion after $1bn year

- IFM to buy Trafigura stake in Nala Renewables to reach 100% ownership

- Aquiline-backed ClearCourse to acquire Kurve

- Lloyds profits soar 33% as higher interest rates boost income

- Barclays takes £228mn hit from collapse of UK mortgage lender MFS

- German energy group Eon nears £600mn deal to buy UK supplier Ovo

- Shell Puts Canada at Heart of Growth Plans in $13.6bn Deal

- Britain’s stealth fighter project faces 10-week funding deadline

- UK car loan companies accept £9bn mis-selling redress scheme

- Man Group hit by single $6.1bn redemption

- DCC considers takeover bid from KKR and Energy Capital

- CVC pumps cash into Lipton as €4.5bn tea deal comes off the boil

- CVC weighs €9bn bid for Italian payments group Nexi

- Lift maker Kone strikes €29bn deal to buy TK Elevator

- Apax possible frontrunner to buy UK’s CloserStill Media from Providence

Industry news

- Bank of England warns ‘higher inflation is unavoidable’ after leaving interest rates on hold

- LSEG boosts 2026 guidance as first-quarter revenue beats estimates

- Small shareholders keep up pressure on UK bank climate policies

- Irish bet on gas from kitchen scraps hits policy snag

- BP warns against windfall taxes as Iran war helps profits hit 3-year high

- Banks brace for tax raid if Starmer is ousted

- UK could save £2.5bn by helping banks to buy gilts, says Barclays

- British retail sales rose 0.7% in March as motorists stocked up on petrol

Salaries and bonuses

- London bankers who’ve gone 4 years without bonuses are possibly in for a pleasant surprise

- Bank of America ups bonuses for top UK investment bankers by 15%

- Goldman Sachs hikes pay for EU hubs by 19% after revenue bounce

Job moves

- Moelis hires Jefferies’ Rosedale to bolster financial sponsors in London

- Boutique bank Rothschild hired a new chief data officer in London

- RBC Capital Markets hires Barclays’ Skilton to lead European insurance

- Citigroup hires Barclays’ Potts to lead activism defence in Europe

- Paul Weiss loses M&A partner to Kirkland in London

- Weil loses three restructuring partners to Akin in London

- Arini hires Brevan Howard portfolio manager to bolster London team

- Barclays taps Jefferies dealmaker Yildiz to co-head European financial sponsors

- JPMorgan promotes London bankers Capper and Pissanos in healthcare shake-up

- Moelis hires Jefferies’ Rosedale to bolster financial sponsors in London

Market trends

Dry powder, cold feet

European PE exit activity slowed sharply in Q1 2026, with deal count falling from 278 to 244 and total value dropping from $58.9bn to $32.3bn, according to White & Case data.

The UK held up better on value, rising modestly from $8.4bn to $8.8bn across 46 transactions, suggesting larger deals are still clearing even as volume thins.

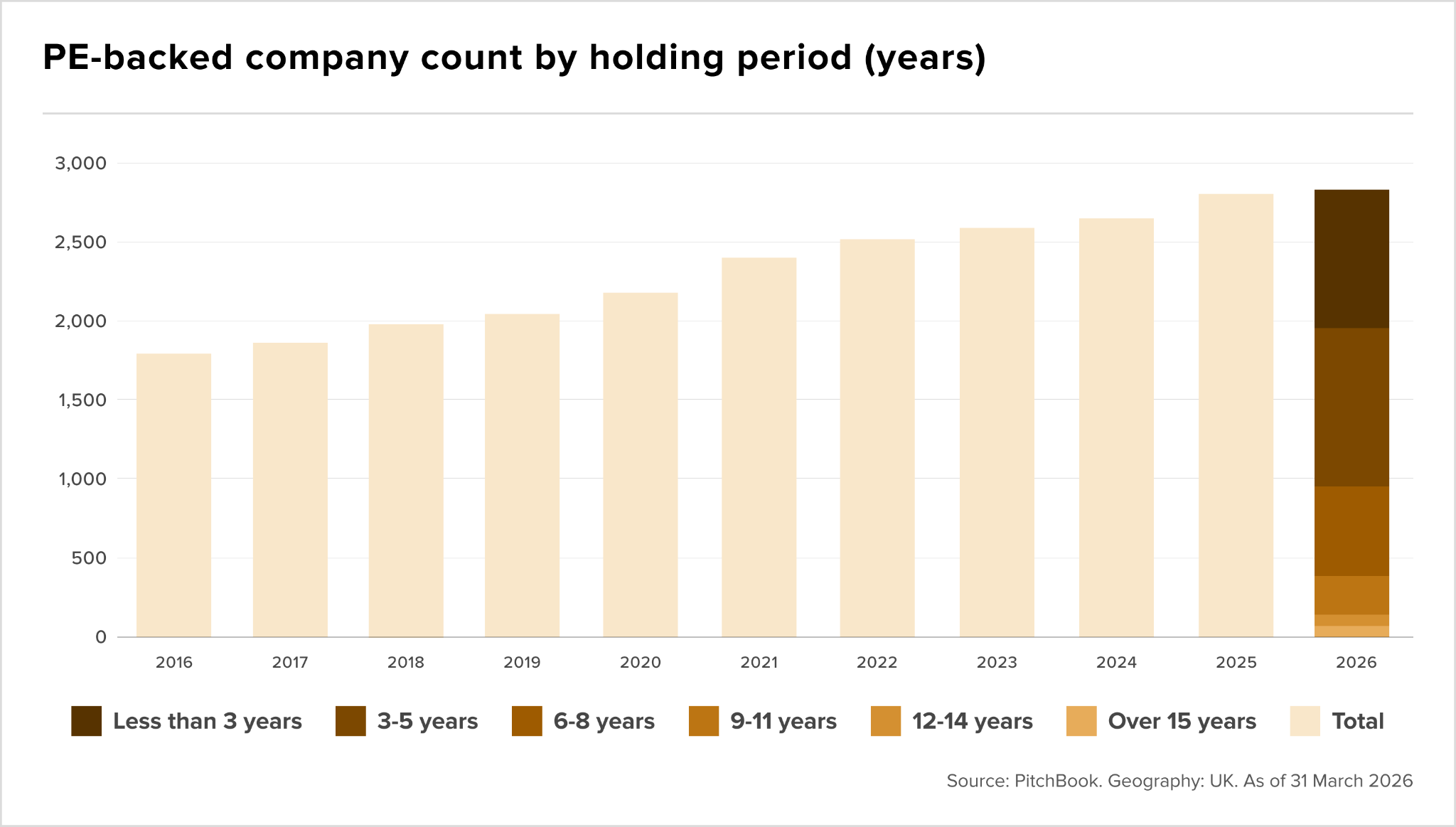

The UK’s PE-backed company count has risen steadily since 2016 and now sits at its highest point on record, with a growing proportion of assets held well beyond the typical fund cycle. Dry powder remains abundant, and with EU merger control reforms potentially broadening the buyer pool, the conditions for a sharp acceleration in activity are taking shape.

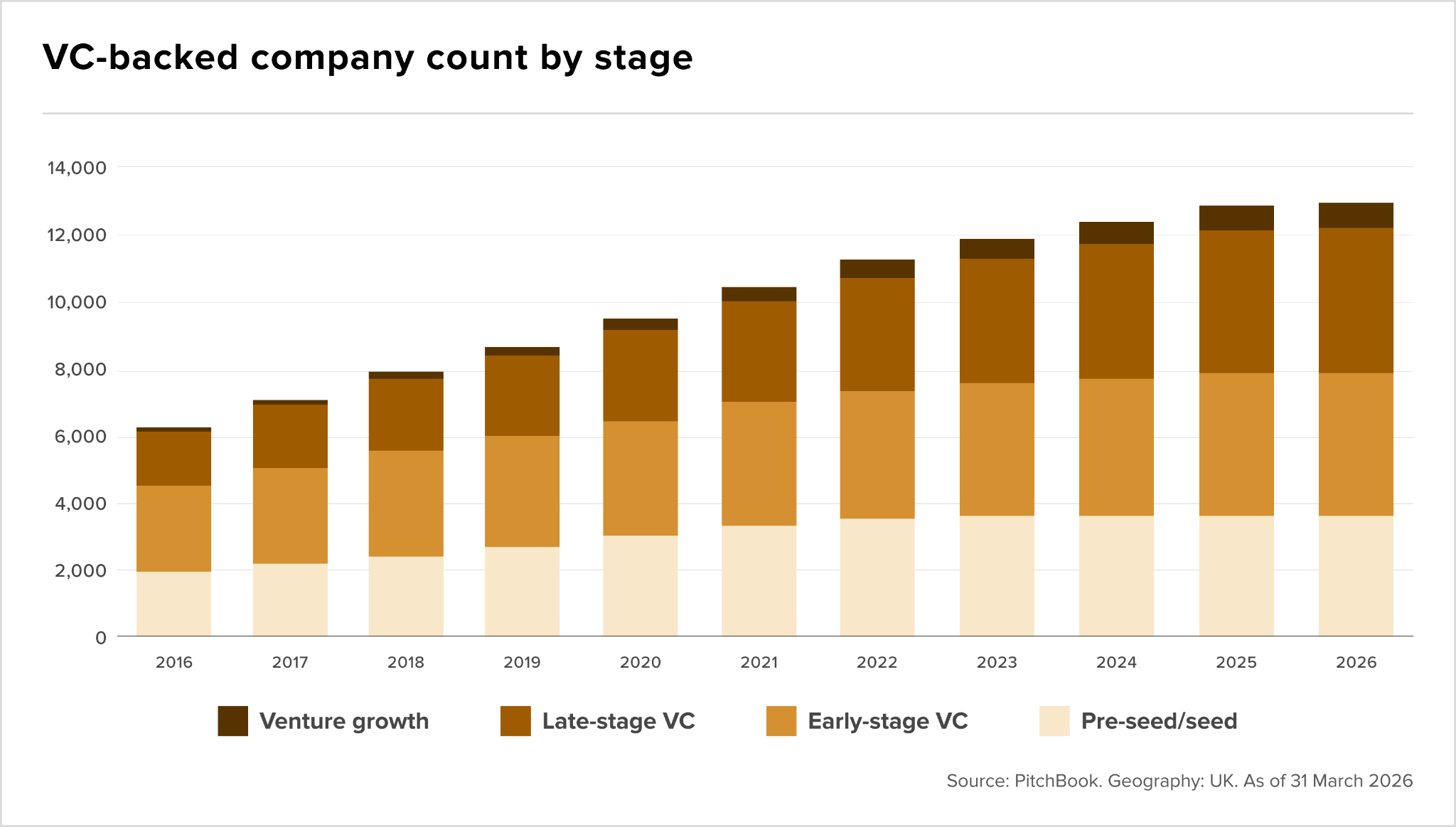

The same growth trajectory extends into venture, where the UK’s VC-backed company count has expanded across every stage since 2016, with late-stage portfolios continuing to expand into Q1 2026. The pipeline, in both PE and VC, is not the problem. What really is becoming harder to ignore is a policy environment that appears to be working against the very firms driving that growth.

A quiet update to Home Office guidance in November 2025 reclassified investment-holding entities, explicitly naming PE funds and VC firms, as non-trading businesses, removing them from eligibility under the UK Expansion Worker visa route.

The route has historically been the primary mechanism through which overseas managers relocate staff to establish a London presence. Firms can still contest the classification by demonstrating active client service, but the burden of proof now rests with the applicant and immigration officers retain considerable discretion.

Tech gets stuck in the slow slow lane

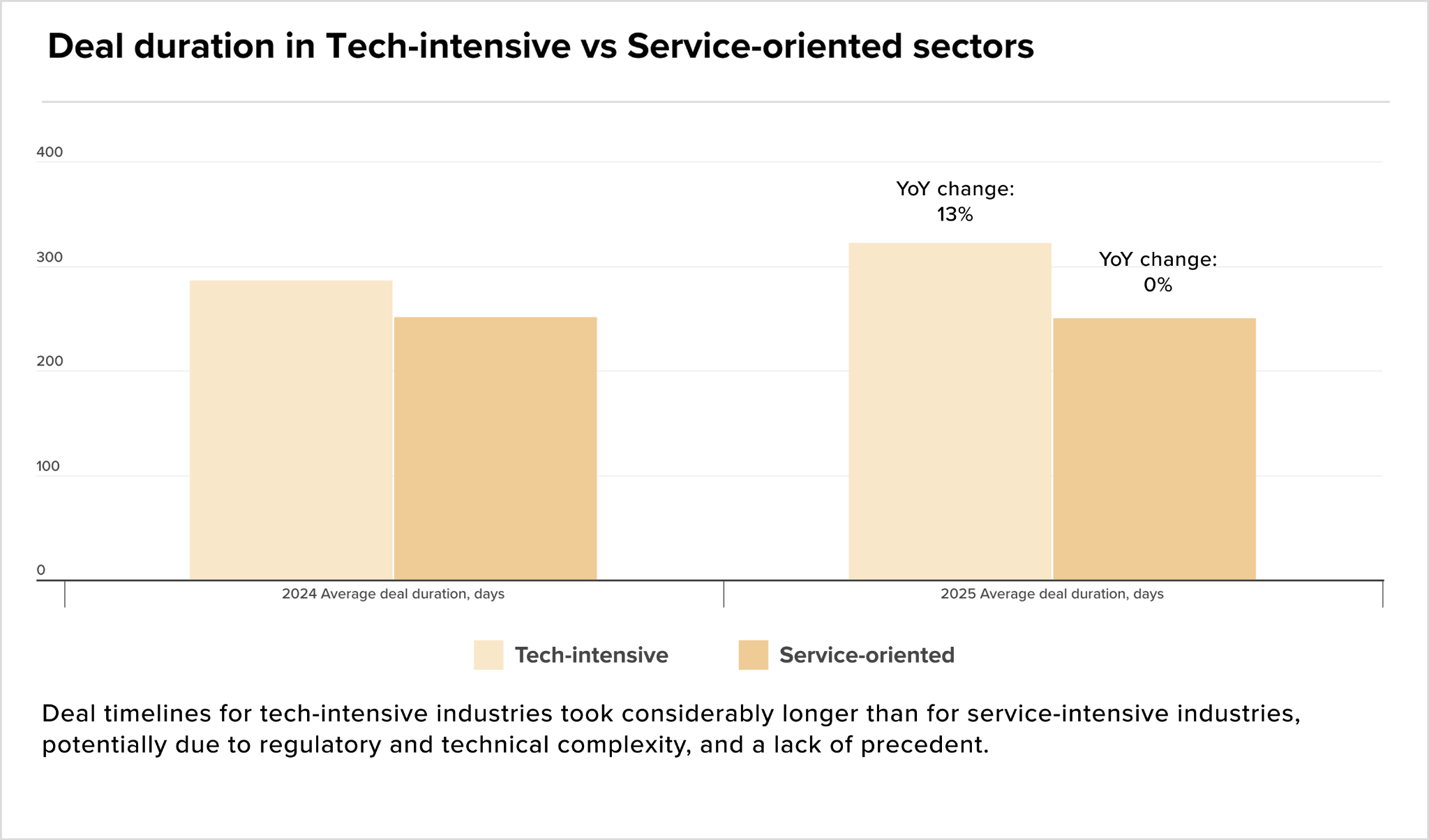

That competitiveness question extends to the mechanics of deal execution itself. A recent Ideals M&A study revealed that across global M&A in 2025, deal timelines remained broadly stable at an average of 264 days, up 3% year-on-year. Tech-intensive deals, spanning biotech, utilities and infrastructure-adjacent assets, averaged 322 days, a 13% increase on 2024, while service-oriented transactions held flat at 250 days.

Regulatory complexity, heavier reliance on forward-looking forecasts and deeper technical diligence all extend the process for tech-centered sectors, even as the tools available to dealmakers have nominally improved. AI adoption in due diligence is rising, but efficiency gains are being absorbed by more rigorous analysis rather than shorter timelines.

For buyers already cautious on software valuations, extended timelines in a volatile rate environment add meaningful execution risk, reinforcing the capital rotation towards industrials and tangible assets that has characterised the opening quarter of 2026.

Domestic capital

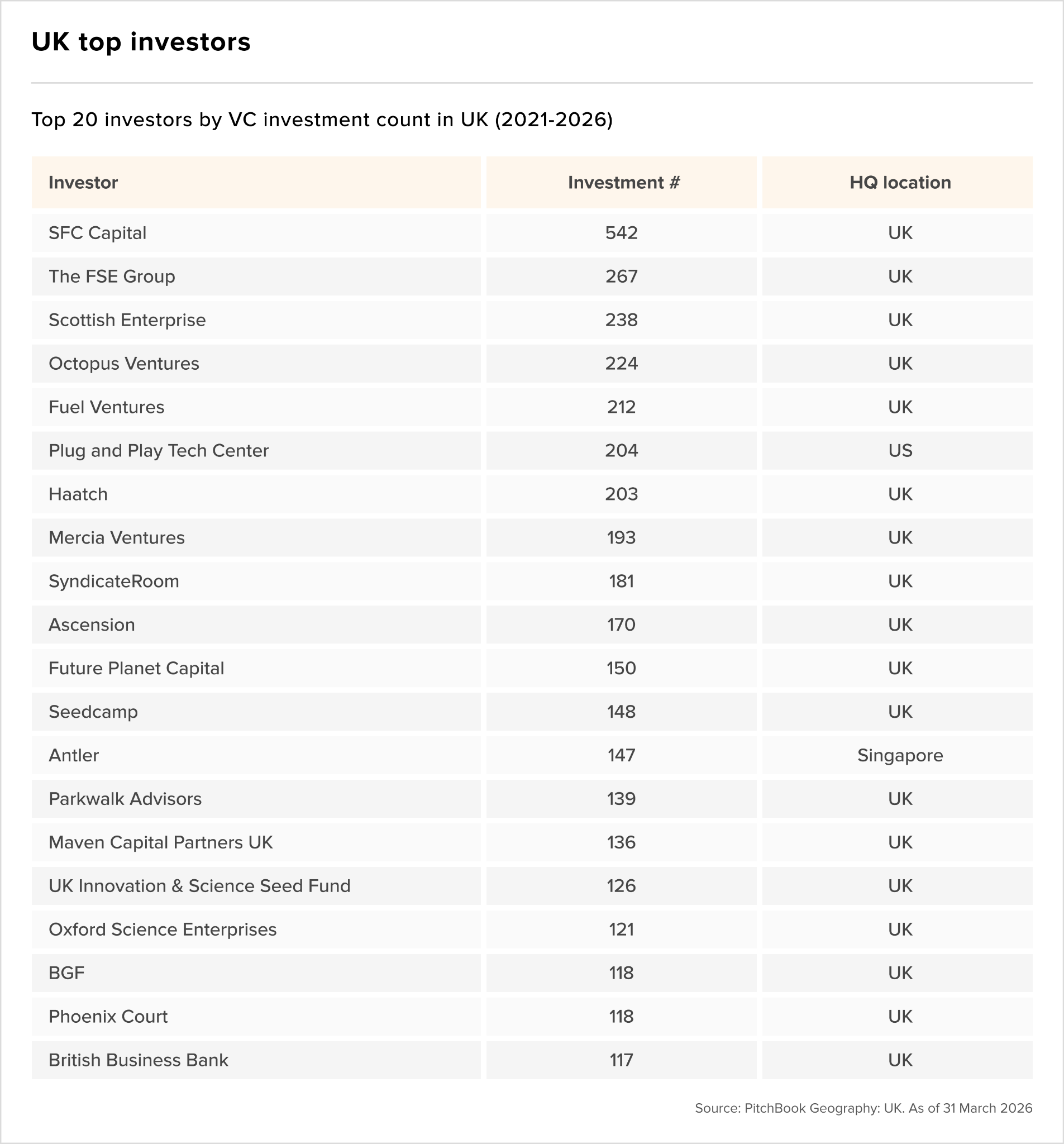

Eighteen of the UK’s top 20 most active VC investors by deal count since 2021 are domestic, with SFC Capital leading at 542 investments, nearly double the second-placed FSE Group.

The list is dominated by early-stage and regional vehicles rather than large institutional names, reflecting a market where volume is being driven by seed and pre-seed activity rather than later-stage conviction capital.

Fundraising

IPOs

- RAC pumps the brakes on £5bn London IPO

- UK proposes cutting IPO timetable by a week to boost listings

- Airtel eyes $2bn London IPO of Mobile Money Unit

- UzNIF’s London IPO set to value Uzbekistan fund at $1.95bn