Daniel Black

Daniel Black

What a difference a week makes. Just seven days after Intertek’s board was set to reject EQT’s £8.9bn approach, the FTSE 100 testing group is now recommending the Swedish PE firm’s £9.4bn “final” offer, according to Private Equity Wire.

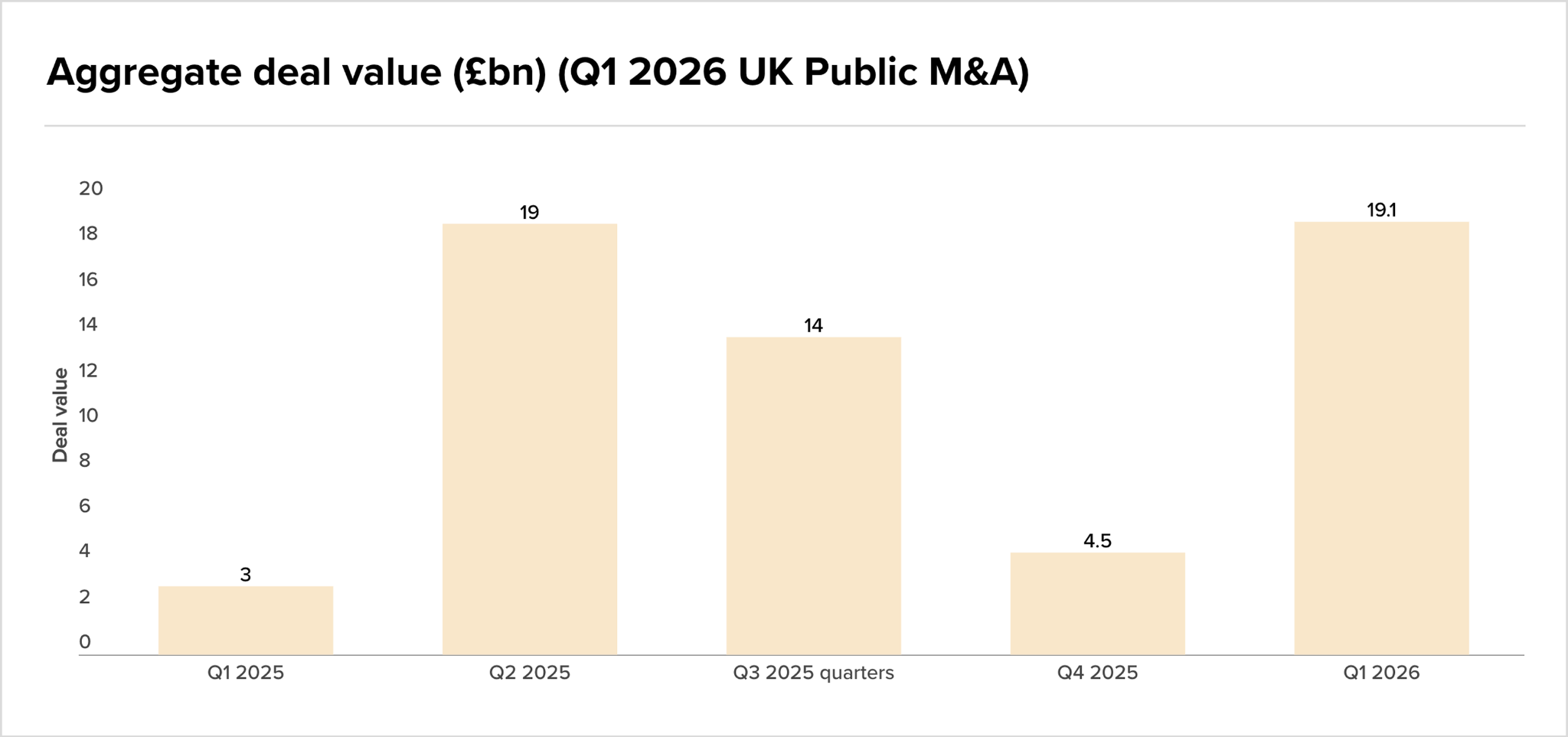

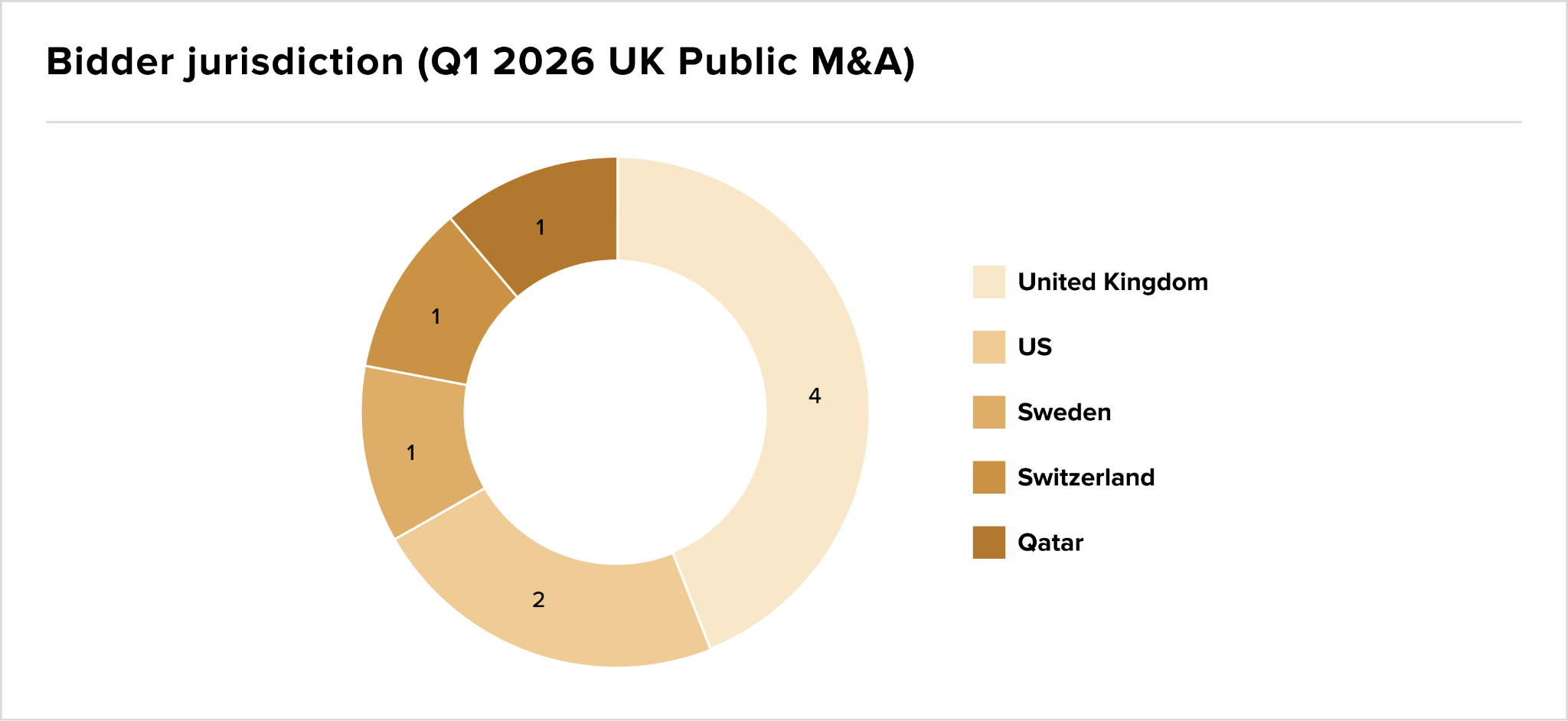

The episode caps a quarter in which two transactions – Nuveen-Schroders and Zurich-Beazley – drove £19.1bn of UK public M&A value, with overseas buyers accounting for 98% of the total. UK assets, it seems, are still cheap enough to be worth chasing.

And in other news this week:

- E.ON has agreed to buy Ovo, creating one of Britain’s largest energy suppliers

- Spire Healthcare shares soared on a £1bn takeover offer, adding another listed UK target to the take-private pipeline

- JPMorgan named new co-heads of investment banking in a wider dealmaking shake-up

Thanks for reading, and connect with me on LinkedIn if you want to discuss how Ideals VDR can help with your next M&A deal.

Deal Tracker

Our weekly roundup of confirmed M&A deals in the UK.

The rumour mill

- Intertek to recommend EQT’s £9.4bn final bid

- FirstRand picks BofA, RMB to advise on sale of UK Aldermore unit

- Providence Equity considers acquisition of Gamma Communications

- E.ON to buy Ovo, creating one of Britain’s largest energy suppliers

- Vodafone said to weigh move to transfer part of India unit stake

- Pollen Street to acquire a majority stake in new home services provider

- Blackstone to acquire Greek e-commerce platform Skroutz from CVC

- Blackstone and Halliburton to invest $1bn in VoltaGrid

- Barclays’ Kristin Roth DeClark discusses enthusiasm around anticipated IPOs

- UK’s Picton Property agrees $546m all-share takeover by LondonMetric, Schroder

- Spire Healthcare shares soar on £1bn takeover offer

- Amulet Capital to acquire TFP Fertility Group from Benefit Street Partners

- Siris to reap 3x return on Equiniti in sale to Bullish

- UK to take full ownership of British Steel

- M&G buoyed by asset management and Dai-Ichi Life flows during first quarter

- BlackRock’s Rachel Lord says asset manager won’t be moving London office anytime soon

- The HSBC bankers who lost $400m got Apollo to do the work. Safest jobs at the Big Four are no longer safe

- Goldman Sachs’ City revenue jumps 17% on stock trading surge

- Ansor-backed Complii to acquire the Escalator Company

- Biba 2026: SSP targeting growth through new M&A strategy

Industry news

- Britain to strengthen ties with the EU in new legislation

- UK economy grew 0.6% in first quarter despite Middle East energy crisis

- UK first-quarter GDP gives Bank of England no urgency to cut rates

- Britain’s government to update banks’ ring-fencing regime

- UK mid-caps drop as political uncertainty and Middle East concerns hit sentiment

- Sterling drops as markets watch UK politics, PM Starmer’s future

- UK government unit targets £99bn of investment from Australian pension funds

- UK stocks muted as Starmer leadership crisis rattles investor sentiment

- Private equity deals were fewer but bigger in the first quarter

- Datacentres using 6% of electricity supply in UK and US

- Global oil inventories falling at record pace amid Iran war; UK bond recovery fizzles out as Streeting ‘prepares challenges

- London’s top gilts traders should be having a big week. Maybe not

Salaries and bonuses

- Hedge fund pay is doing very well after a bumper 2025

- Grant Thornton partner pay flat following Cinven deal

Job moves

- Hedge fund Millennium hired hedge fund Schonfeld’s top equities recruiter in London

- JPMorgan names new co-heads of investment banking in dealmaking shake-up

- Man Group hires former Eisler money manager to bolster New York office

- Citigroup hires Seifert and Ord to bolster UK dealmaking team

- Jefferies hires real estate dealmaking duo in Europe

- Mayer Brown launches new capital solutions team in London

- London Stock Exchange Group trims remote working for some staff

- Commerzbank to cut 3,000 jobs as it seeks to fend off UniCredit

Market trends

Two deals told the whole story

Nine deals. That’s what UK public M&A produced in Q1 2026, the same number as Q4 2025 and Q1 2025. On paper, the market looks stuck. Look closer, and it’s anything but.

Aggregate deal value hit £19.1bn this quarter, a figure driven almost entirely by two transactions: Nuveen’s £9.9bn acquisition of Schroders and Zurich Insurance’s £8.1bn move on Beazley. Strip those two out and you’re back to a quiet market. Keep them in, and Q1 2026 matches Q2 2025, the strongest quarter of last year.

Why now? Because London is still cheap, and strategic buyers know it.

The Nuveen-Schroders deal didn’t happen in a vacuum. It reflects something that’s been building for two years: a persistent valuation gap between London-listed companies and their US counterparts, wide enough that cross-border acquirers can justify a 33% average bid premium and still walk away with a bargain by their home market’s standards.

Part of that discount is structural. Part of it is political. Economist Dario Perkins coined the term “moron premium” after the Truss mini-budget, and City bankers are dusting it off again as gilt yields breach 5%, the highest in the G7, according to Ion Analytics. For overseas buyers with a long time horizon, someone else’s political discount is their entry point.

Overseas bidders accounted for just 56% of firm offers in Q1 but 98% of total deal value. US buyers alone, with only two deals, represented 53% of aggregate value. That asymmetry tells you everything about where conviction sits right now.

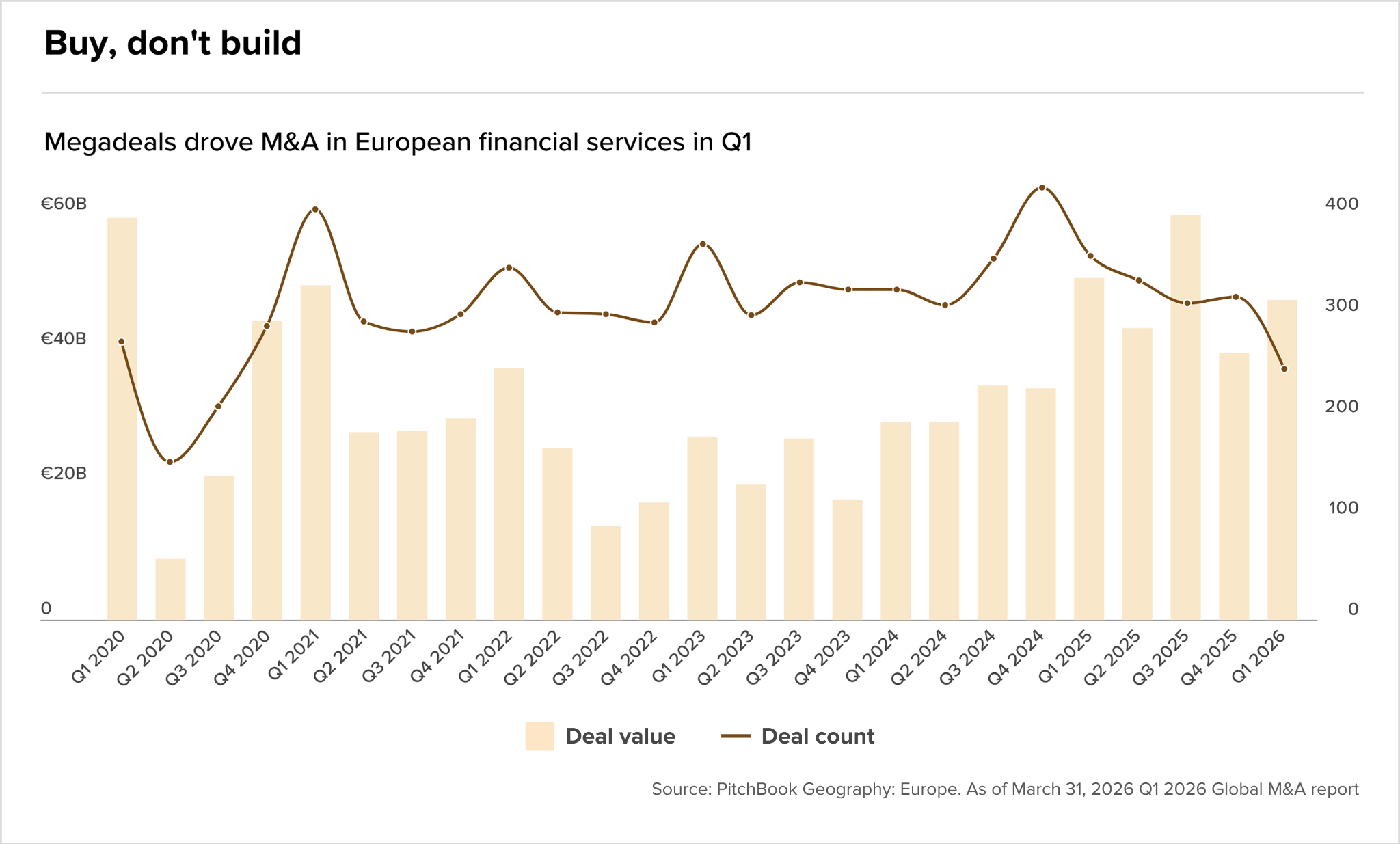

In financial services, the logic is structural, not opportunistic

The two defining deals of the quarter both land in the same sector, and that’s no coincidence. Asset managers across Europe are under real pressure: 89% reported profitability challenges over the past five years, with cost-to-income ratios stubbornly stuck around 68%, according to PitchBook Q1 2026 Global M&A Report.

For mid-sized players, organic growth alone won’t close that gap. Scale through acquisition has become the default strategic response, and Q1’s numbers reflect exactly that. European financial services M&A hit $47.6bn across 235 deals in Q1, with just four transactions accounting for two-thirds of the total. The sector isn’t consolidating gradually. It’s consolidating in bursts.

April, though, tells a more cautious story

After Q1’s megadeal momentum, April brought a noticeable step back. Firm offers fell to four, down from seven in April 2025, and possible offers dropped from nine to six, as reported by Herbert Smith Freehills Kramer.

The Iran conflict and renewed interest rate pressure are part of it, but the domestic backdrop isn’t helping either. With Starmer’s leadership increasingly in question following last week’s election results, the UK is potentially heading towards its sixth prime minister in 10 years since the Brexit vote. Investors don’t price uncertainty kindly, and dealmakers are feeling it.

Interestingly, of the 13 firm offers announced so far in 2026, four used mixed consideration structures, three of which included stub equity. Deal architects are getting creative to bridge valuation gaps rather than walking away from the table entirely.

Fundraising

IPOs