Daniel Black

Daniel Black

For the first time in weeks, the UK story isn’t just about being bought.

GSK announced a $10.6bn acquisition of US oncology specialist Nuvalent – its biggest outbound deal of the year and a clear signal that the FTSE pharma giant is expanding its oncology pipeline, according to Bloomberg.

In the same week, Ingredion’s $3.6bn purchase of Tate & Lyle was confirmed by the board, another UK consumer icon heading to American ownership. Britain is buying and being bought in roughly the same breath, and UK M&A this year is finally starting to look two-way.

And in other news this week:

- Boots has attracted $10bn of takeover interest as its PE owners pivot away from IPO plans.

- Frasers Group tabled a $2.3bn offer for the rest of Hugo Boss, deepening Mike Ashley’s UK-led roll-up of European retail.

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Claude, ChatGPT, and Copilot inside your VDR: How Ideals MCP changes M&A

On Thursday, June 25, Ideals VDR is hosting a 45-minute live session showing four AI workflows deal teams can run directly inside the data room today.

From assessing strategic fit against a CIM and analyzing bidder engagement, to managing buyer Q&A and running vendor due diligence with the CEO of Emma Legal – you’ll see real prompts and real outputs.

Deal Tracker

Our weekly roundup of confirmed M&A deals in the UK.

The rumour mill

- Blume Equity leads up to €49m investment in Ireland’s CameraMatics

- Inflexion-backed Axiom GRC to acquire assurance firm MHM

- GSK to buy Nuvalent for $10.6bn in oncology push

- Evoke shares rise after board agrees to $326m takeover by Bally’s Intralot

- Ingredion to take over Tate & Lyle in $3.6bn deal

- EasyJet’s share price soared on takeover news. is it a buy?

- Frasers Makes $2.3bn offer to buy rest of Hugo Boss

- VodafoneThree bids for TalkTalk consumer business

- Tate & Lyle Accepts Bid From Ingredion in Loss for London

- UK Payments Firm OpenPayd nears deal to go public via Titan SPAC

- Oxford BioMedica signals potential openness to PE bid despite rejecting EQT offers

- Boots attracts $10bn takeover interest as PE owners pivot away from IPO plans

- Australian broking group that recently expanded in UK gets buyout offer

Industry news

- HSBC fintech venture racks up $21m in losses

- Lex Greensill banned from being UK company director for nine years

Salaries and bonuses

- How much do London’s family offices pay? Very good, or very average

- Ex-Goldman Sachs bankers’ boutique Ardea hikes UK pay after hiring spree

- FCA fines BancTrust CEO £99,600 for failing to disclose penalties

- Katten hands out £10,000 pay rises to newly qualified solicitors in London

- Simmons & Simmons to reward AI adoption in bonus overhaul

Job moves

- Equals appoints COO Edward Chandler following Railsr merger

- Moelis hires Lazard’s Knott to bolster London chemicals coverage

- Standard Chartered hires Deutsche dealmaker McBride to lead consumer M&A

Market trends

Volume is down. Stakes are up.

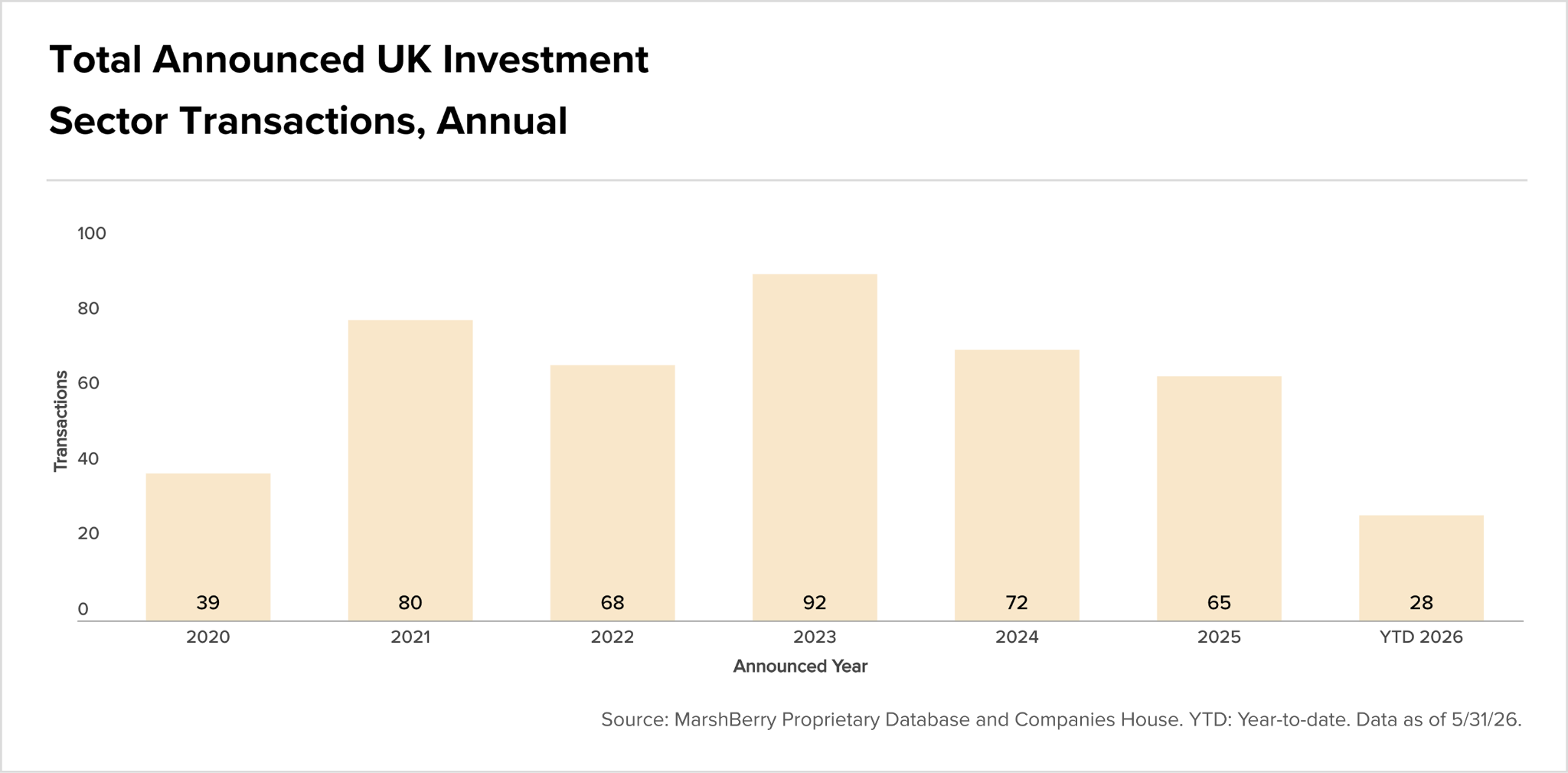

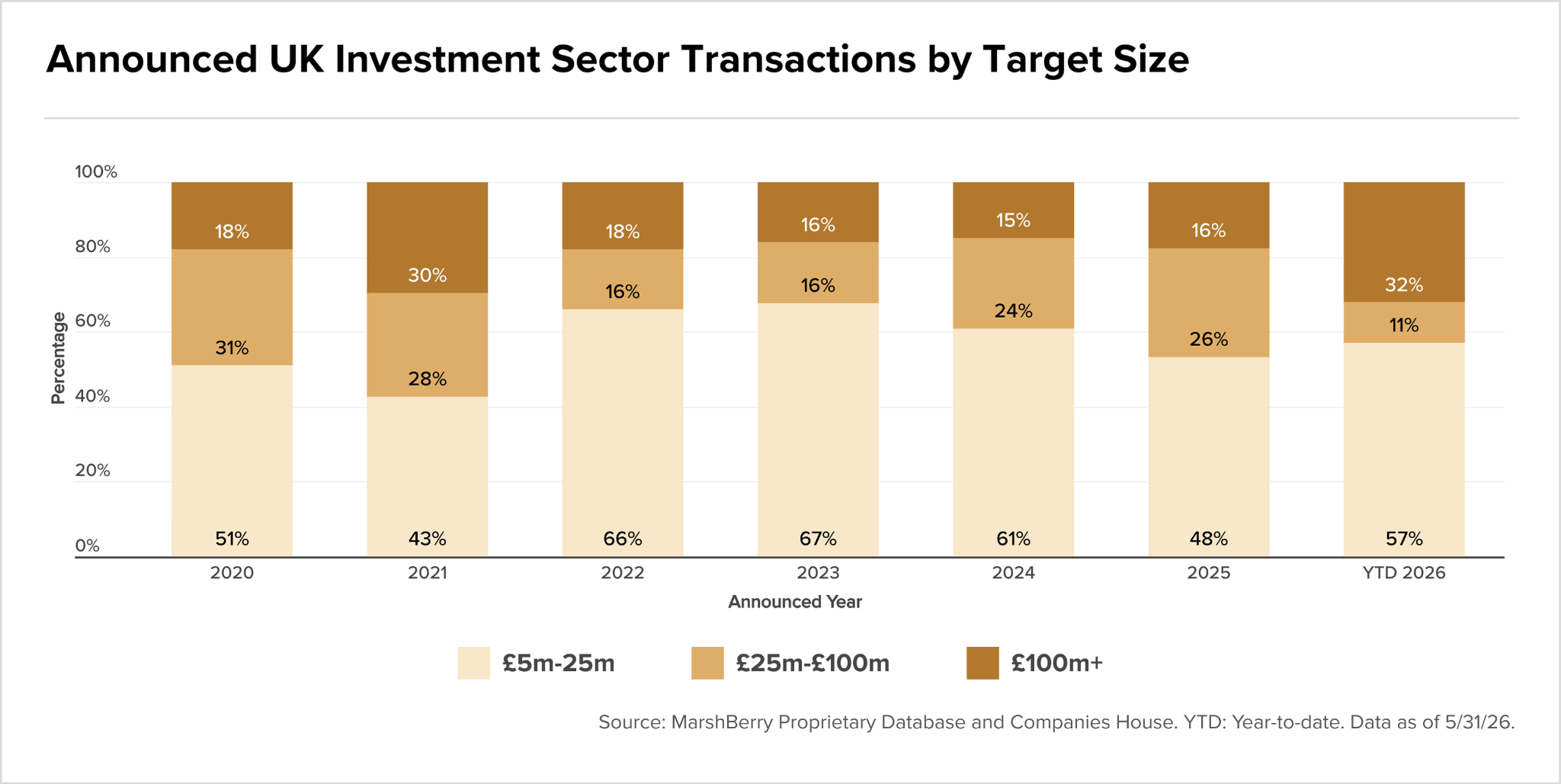

The UK investment sector banked 28 transactions through May. On the surface, that looks like a market cooling off. But count isn’t the story here. MarshBerry’s May 2026 M&A Market Update puts it plainly: 2026 is running the highest share of £100m-plus transactions ever recorded at 32% of total deal volume.

While the number of deals has pulled back since the 2023 peak of 92, the capital concentration tells you where real conviction sits: buyers aren’t stepping back, they’re becoming more selective. Fewer bets, bigger ones.

May itself was unusually quiet, with only three deals above £5m announced and none crossing the £100m mark. One month doesn’t make a trend. What it does signal is that acquirers are not rushing. Diligence timelines are stretching, and price discipline is winning over deal velocity.

For sellers, that’s an important recalibration. The window is still open, but the days of accepting any term sheet are over.

PE is running the show

Look at the deal size breakdown over time and one shift stands out. The mid-market, those £25m to £100m transactions, has been quietly hollowing out. In 2023, it represented 16% of activity. YTD 2026, it’s fallen to 11%. Meanwhile, the large-deal segment keeps expanding and bolt-on acquisitions under £25m continue to dominate volume at 57%.

The market is bifurcating. At the top, PE-backed consolidators are chasing scale with platform acquisitions. At the bottom, those same platforms are vacuuming up smaller IFA and wealth management books to add AUM and geography. The middle is getting squeezed from both ends.

PE’s fingerprints are on nearly two thirds of all deals in 2026, up from around 31% in 2020. That isn’t a side effect of the market. It’s the market. Sponsor-backed buyers have effectively restructured the competitive landscape in UK wealth management, and independent acquirers are increasingly rare in the chair across the table.

IPOs