Sebastian Montoya

Sebastian Montoya

In this week’s edition, we explore recent 2025 M&A data from McKinsey and KPMG exploring how regional particularities played a decisive role in deal flow.

But the numbers tell only part of the story. Despite the challenges, this week’s highlights show European dealmakers creating momentum and using strategic transactions to expand the region’s green footprint.

- An infrastructure fund managed by DWS has become the sole shareholder of Cleanwatts. The transaction will give DWS 100% ownership and foresees an investment of approximately €150 million by 2030. Cleanwatts currently holds a total photovoltaic solar capacity of around 30 MWp.

- Engie has acquired UK Power Networks for £10.5 billion ($14 billion). The company delivers 71 TWh of electricity each year and holds three distribution licenses covering London, East of England and the South East.

- Iberdrola France closed a deal with Technique Solaire sold a 118 MW operational wind portfolio and 639 MW onshore wind and solar PV. In a press release, the company says that the transaction forms part of its strategy to focus investments on its core businesses (mainly network and long-term contracts.

Want more insight?

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Energy M&A in the UK: Cocktails & Conversations

The UK energy and infrastructure market continues to command global attention. Robust regulatory frameworks, targeted government backing, and sustained growth across offshore wind, hydrogen and smart grid technologies are fuelling a new wave of M&A activity.

What does this mean for investors, operators and dealmakers?

Meet us at Black Lacquer at Hyde London City for an exclusive evening of high-level networking and sharp market insight.

Deals breakdown

Global energy M&A rebounds 15% as EMEA hits a five-year low

Larger deal values combined with a lower volume of transactions has been a consistent insight across nearly every report we’ve analyzed in recent months.

And even the title of McKinsey’s latest report leaves little doubt that the consultancy has reached the same conclusion.

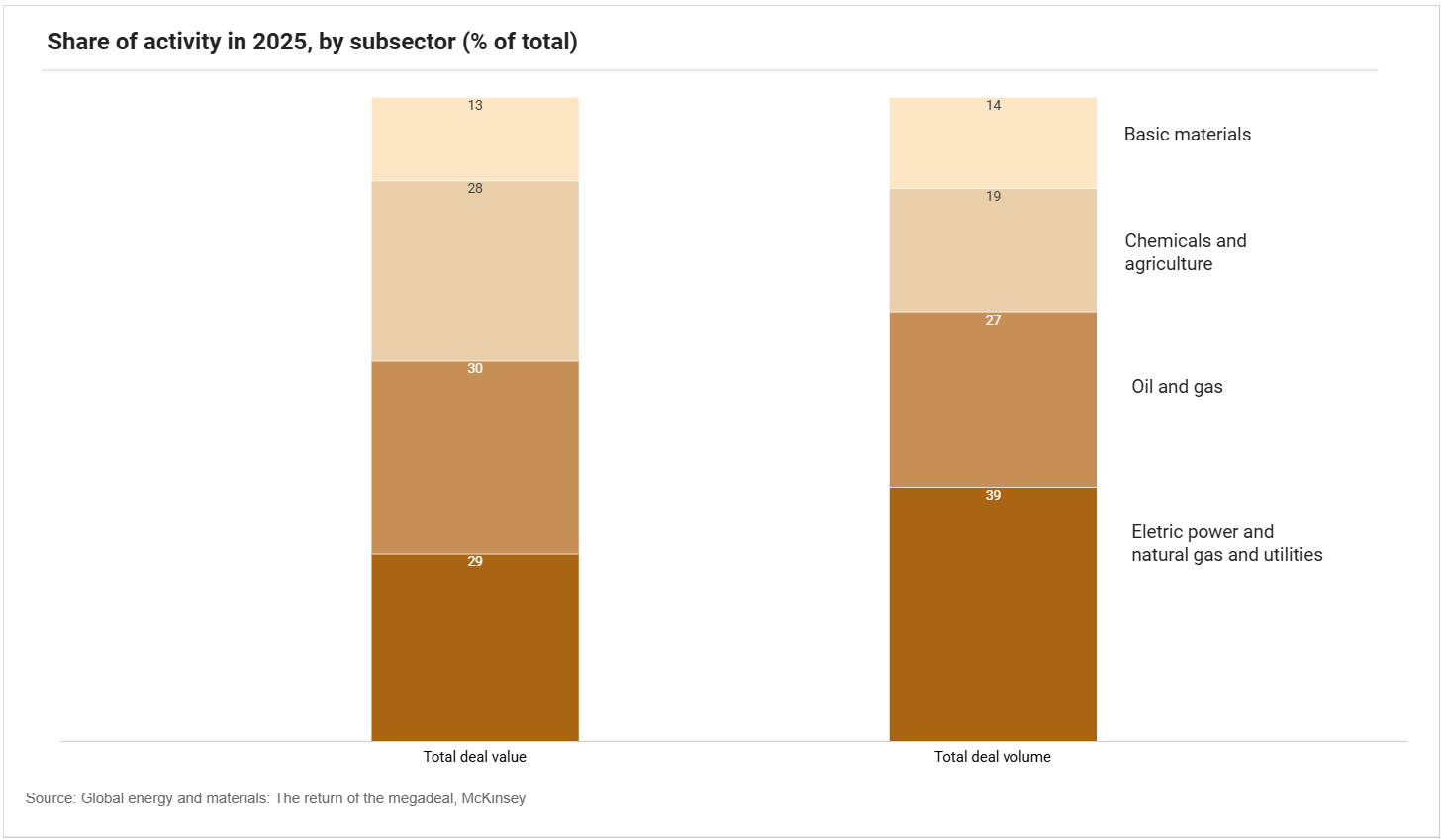

In Global Energy and Materials: The Return of the Megadeal, the data points to M&A across global energy and materials rebounding sharply by 15% versus 2024 and delivering the highest total deal value seen in the past five years. A wave of megadeals returned to the market, restoring momentum after a period characterized by smaller transactions and consolidation.

Within that rebound, electric power and natural gas was the largest subsector by deal value, with value up 75% to $253 billion.

How did Europe’s story diverge from the global headline?

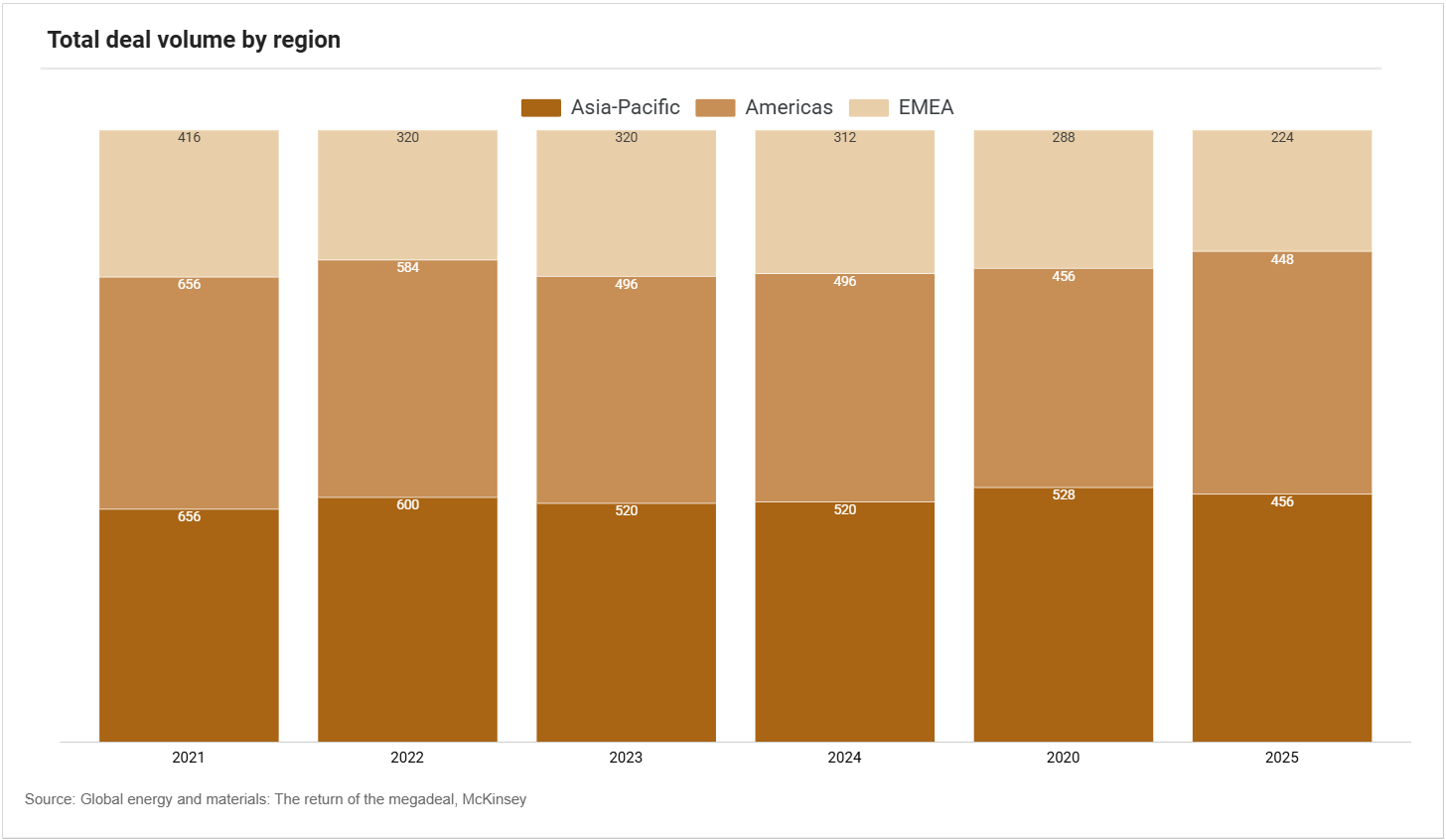

The EMEA region recorded its lowest absolute deal value in five years, reflecting a challenging environment for large-scale transactions. And this pressure is most visible in renewable-energy sources.

McKinsey’s data shows that, in EMEA, deal volume in electric power and natural gas fell 50% compared with 2024, and the drop was most pronounced in renewables, where activity declined 55%.

The downturn was largely driven by a sharp reduction in photovoltaic deals and a 35% decrease in average deal size. McKinsey points that this decline is directly linked to lower market valuations, influenced by a less optimistic outlook on capture prices.

Across the Atlantic, the contrast is clear. US activity in the same subsector reached its highest deal volume in four years. Although the number of renewable transactions declined by more than half, average deal size was driven up by a handful of megadeals.

During the period, KPMG’s H2 2025 M&A trends reports shows that renewable M&A value rose by +173.3% in the region, while volumes fell by -4.1% vs 2024.

- In total, the Americas continued to lead M&A activity, accounting for 65% of global deal value.

- By contrast, Asia experienced a mild downtick from the previous year, with deal value falling by approximately 3%, to $143 billion.

Another pattern in the US, mirrored to a similar extent in Europe, is the performance in H2. In the US, H2 deal value fell by -63.7%, with volumes down -12.9%.

- Globally, Private equity has also become a central force, with its share of total deal value jumping to 19% in 2025, according to McKinsey, often targeting infrastructure and data-centre supply chains.

In Europe, renewables M&A market is being repriced and filtered through tougher expectations (especially on capture prices)

In the US, biggest motors were primarily driven by growing power demand from data centers and higher energy prices.

And in a global perspective, capital increasingly followed scale, certainty, and the ability to underwrite large deals.In 2026, the challenge is to find a way to address these challenges and opportunities in a regional perspective. You can do it, with the right strategy.

Hydrogen

- Greece | Hellenic Hydrogen seeks minority partners for 50 MW North-1 green hydrogen project in Amyntaio, advancing Balkans’ first off-grid renewable hydrogen site

- Netherlands | Power2X acquires hydrogen developer HyCC to scale clean molecule and green hydrogen projects across the Netherlands and Germany, accelerating industrial decarbonisation delivery

Retail/Grid Network

- France | Alterna énergie acquires Vattenfall’s French supply operations, doubling portfolio to 10 TWh and 350,000 customers to become fourth largest electricity supplier

- Spain | Marubeni secures EU approval to acquire Catalan supplier Factorenergia via SmartestEnergy, advancing global electricity and gas retail expansion strategy

- United Kingdom | Engie agrees to acquire UK Power Networks from CKI for £10.5 bn ($14 bn), expanding regulated electricity distribution footprint serving 8.5 million customers

Solar

- Italy | Korkia sells 10.7 MW fully permitted solar PV portfolio in Lombardy through Biko Renewable Energy JV, advancing ready-to-build assets amid strong investor demand

- Portugal | DWS-managed infrastructure fund acquires 100% of Cleanwatts from Verdane, backing €150 m investment plan to scale photovoltaic energy communities platform

- United Kingdom | Ampyr Solar Europe acquires consented 530 MW East Yorkshire Solar Farm from Boom Power, expanding UK PV pipeline ahead of planned 2029 grid connection

Wind

- Portugal | Exus Renewables agrees to acquire 60% stake in Masdar’s 164 MW repowering wind portfolio, expanding European footprint while advancing hybrid wind and solar integration

- Romania | Spanish-based international investor acquires 50% stake in 389 MW Constanța wind portfolio from developer, forming joint venture to advance large-scale projects