Sebastian Montoya

Sebastian Montoya

BESS has become a favourite among many investors, but recent reports and interviews with law firms show that the incentives and strategies the market had been consolidating around are shifting direction in 2026.

This edition of Teaser Energy Europe unpacks what changed, how some investors are already reading the shift and the first signs of margin compression.

Also don’t miss our deals tracker, covering this week’s clean energy transactions across Europe.

Key highlights include:

- Blackstone Infrastructure committed up to €2bn to Eurowind Energy, taking a minority growth stake in the pan-European developer’s wind, solar, BESS and biogas portfolio across 16 markets.

- TotalEnergies closed its 50% acquisition of EPH‘s flexible generation portfolio, forming a new joint platform branded TTEP. The combined entity holds 14 GW installed or under construction plus a 5 GW pipeline across gas, biomass and BESS.

- Copenhagen Infrastructure Partners completed its carve-out of Ørsted‘s European onshore business, launching the assets as Perigus Energy. The new platform takes over 826 MW of operating and under-construction capacity, plus a multi-GW pipeline across Ireland, Germany, the UK and Spain.

Want more insight? Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

The BESS paradox: Why Europe’s fastest-growing energy asset is getting harder to build

You’ve already read in Teaser Energy Europe how the continent’s clean energy market is shifting, with GW capacity sharing more and more space with infrastructure, consolidated revenue streams, and regulatory environment in the decision-making process.

In a scenario like this, we see priorities changing. And BESS sits at the centre of that transformation.

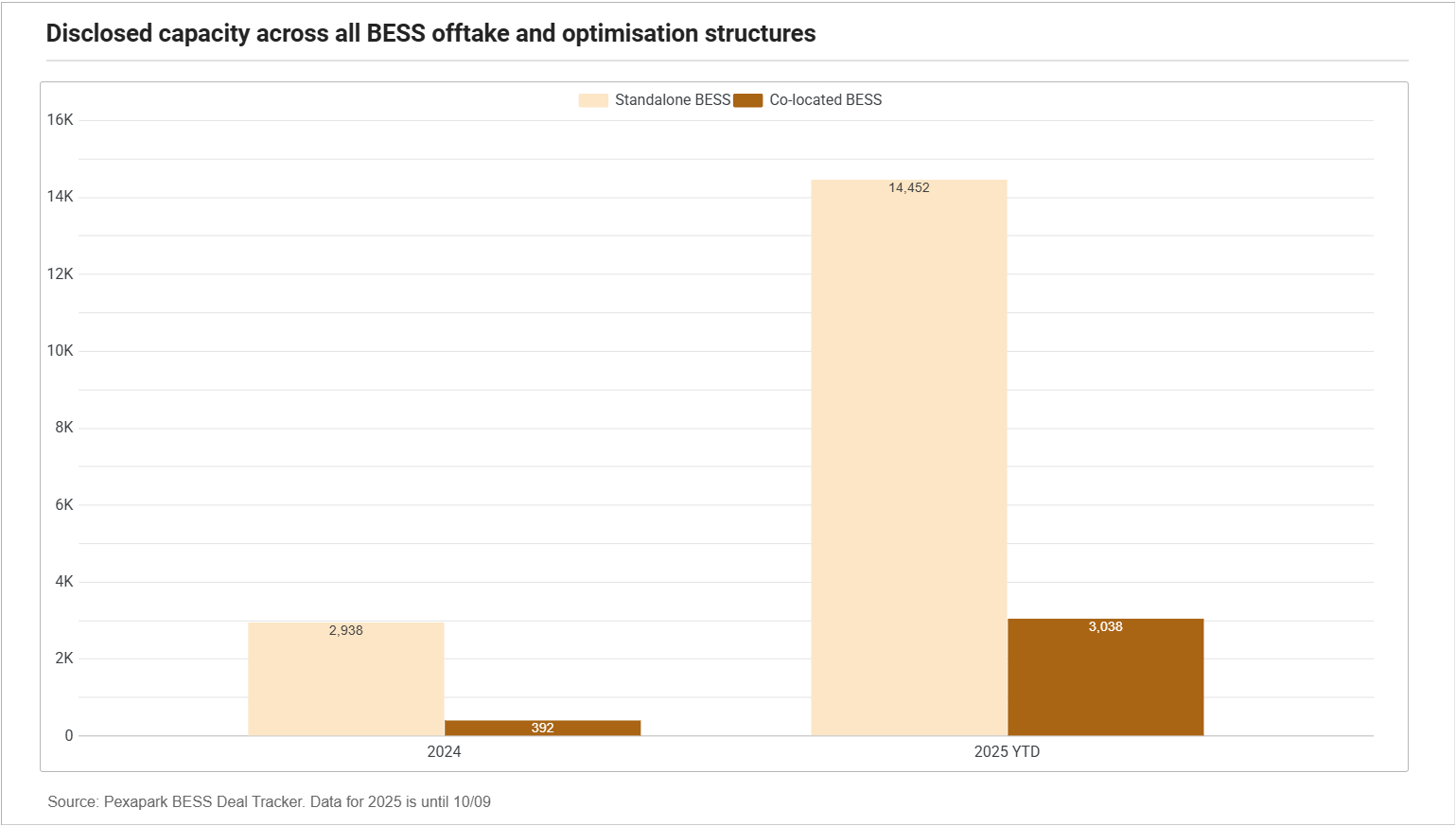

European installed BESS capacity rose by more than 7 GW between 2024 and 2025, reaching just over 17 GW, according to Aurora Energy Research. The consultancy also projects additions of more than 80 GW by 2030. The numbers are encouraging on its face, even more when we take into account the expectations of other reports, such as the EMMES 9.5 report, that expects that BESS capacity can cluster up to around 100 GW by 2030.

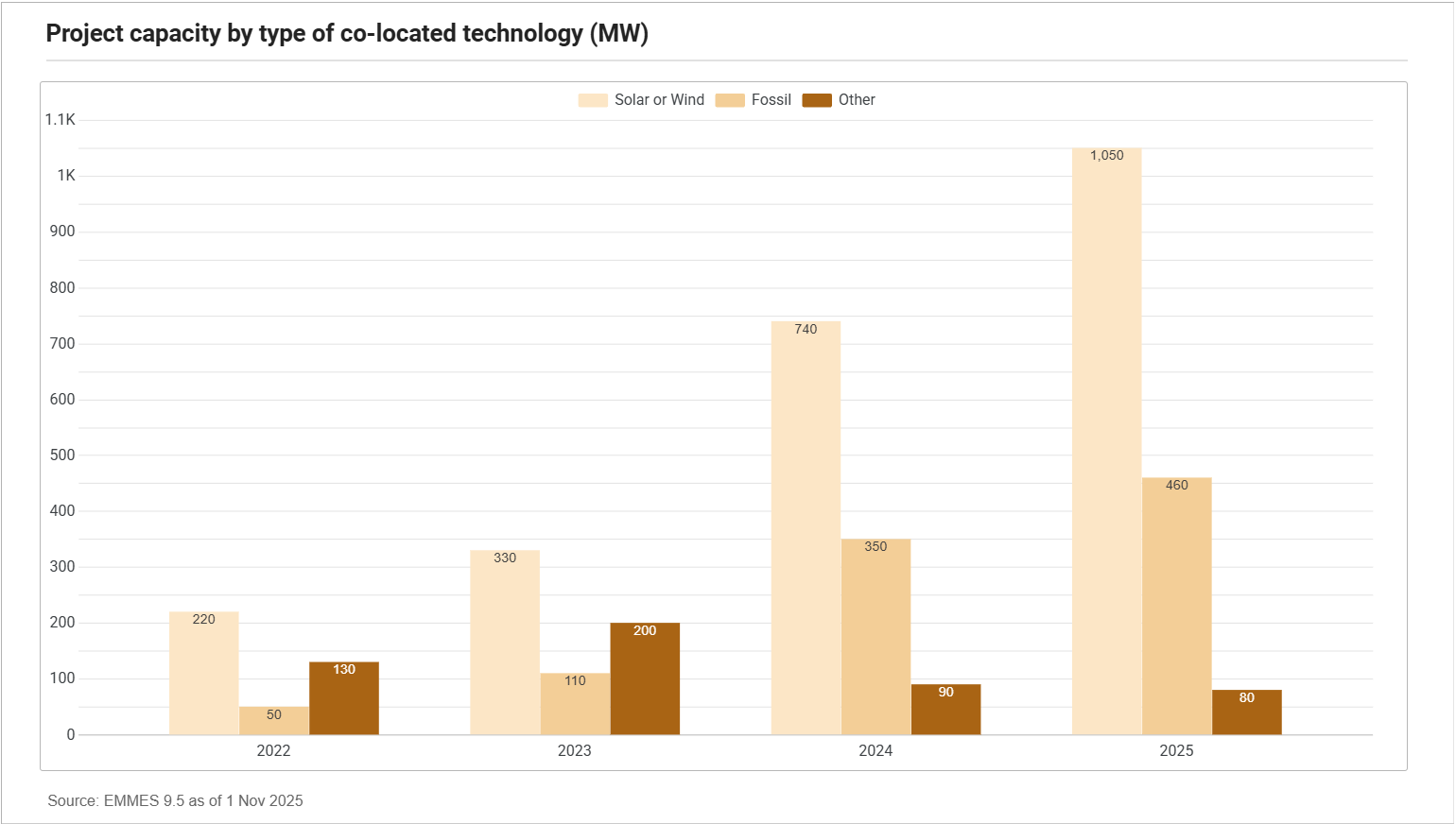

Another signal is that a good share of that capacity is not coming from standalone initiatives: colocation is gaining ground. Pexapark data released in late 2025 estimated the market already counts over 3 GWh of co-located BESS capacity contracted in 2025, with Solar+BESS integration as the highlight.

All of this sounds very optimistic, but different forces are acting under that equation. A recent S&P Global article, based on interviews with Fieldfisher specialists, reinforces the case. BESS is positioning itself as something that goes beyond the logic of risk reduction and enters the territory of CAPEX optimization. But now, grid access and legal frameworks are emerging as increasingly clear barriers.

Would that be enough to pull the brake on such a fast-moving market?

War, commodities and the cost of acceleration

Through the geopolitical lens, the war in the Middle East has indirect impact. With the conflict’s influence on energy, logistics, and commodities markets, the region gains more incentive to reduce exposure to imported fossil fuels and accelerate the transition.

These factors, according to S&P, strengthen the argument for stronger European demand for clean energy and reinforce the BESS case. But the other side has its own narrative. The war increased the internal urgency for alternatives, but this runs into execution.

Supply chains have been disrupted in aluminium, copper, petrochemicals, and other inputs used in solar, wind, and storage. A paradox forms where the war makes BESS more necessary, but also contributes to a scenario where it’s harder and more expensive to deliver.

- On commodities in general, the World Bank projects a 16% rise in global commodity prices in 2026;

- In India, for instance, data already shows aluminium scrap prices up nearly 30% since the start of the conflict, with units cutting production by up to 40%;

- Copper hit USD 13,448.5/t on 22 April, a seven-week high.

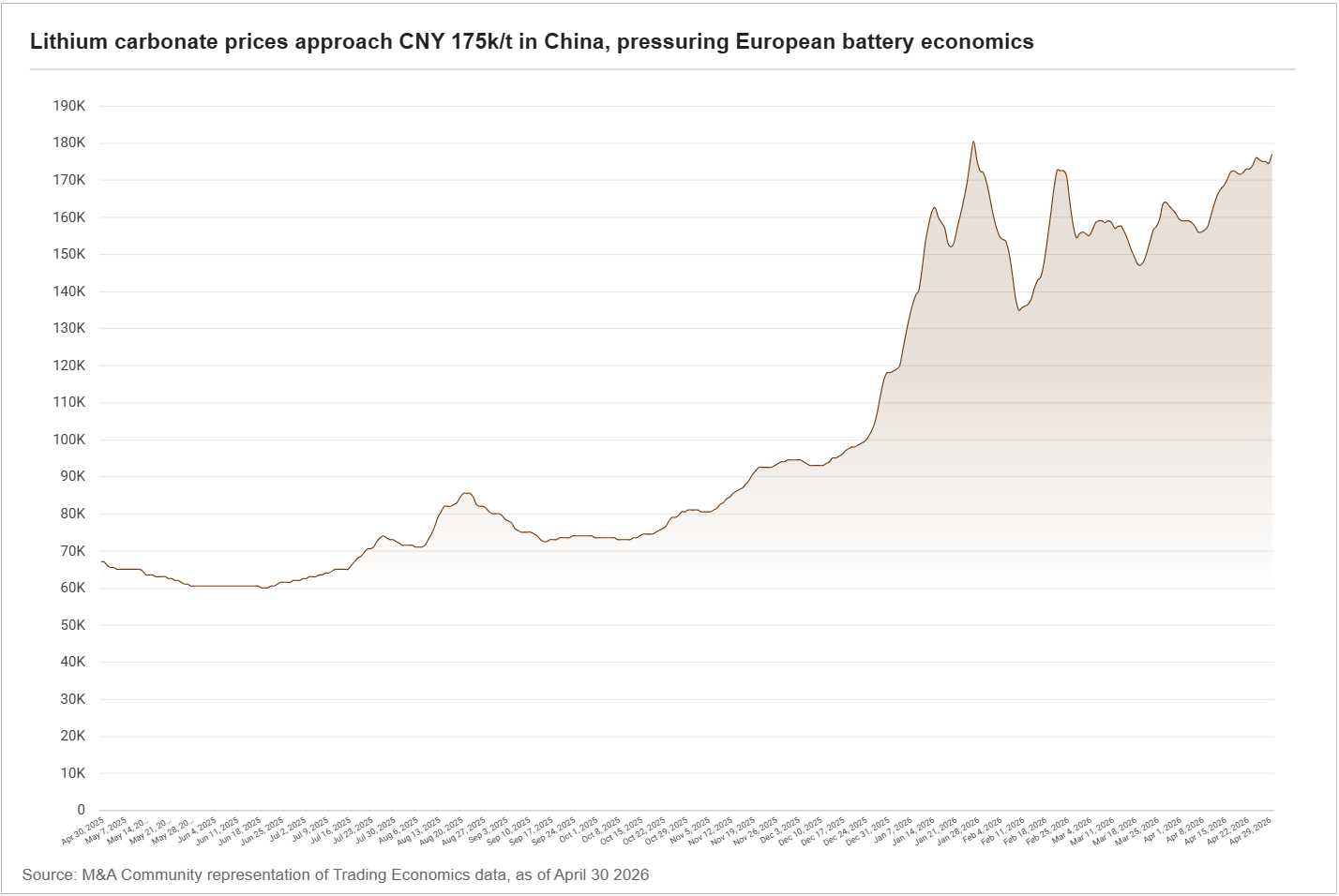

- China’s price for Lithium CFD stood at CNY 177,000/t on 30 April, up 8.59% on the month and 163.79% YoY.

That would be a fast shift from the 2025 scenario, when sources like Bloomberg pointed to costs at record lows.

The regulatory reality check

The second discussion concerns what a battery earns once it connects. The point is mostly regulatory, even more so because the economic model that makes BESS viable today also depends directly on arbitrage, ancillary services, optimisation, and tariff structures.

Until now, projects connected in Germany, in instance, before 4 August 2029 could benefit from a 20-year exemption from network tariffs. But the ongoing regulatory discussion already signals that this privilege should not remain indefinitely, creating a rush for connection before the deadline and adding uncertainty to the business case of new projects.

But Germany is not an isolated case. The tension shows up across the region.

- The UK, faced with a connection queue that exceeded 700 GW, closed 2025 by completing the most ambitious overhaul of its grid access process in decades, retaining 83 GW of battery storage in the prioritised pipeline and clearing the rest. This serves as a mechanism to prioritize ready projects, with land rights, planning permission, and alignment with national energy objectives.

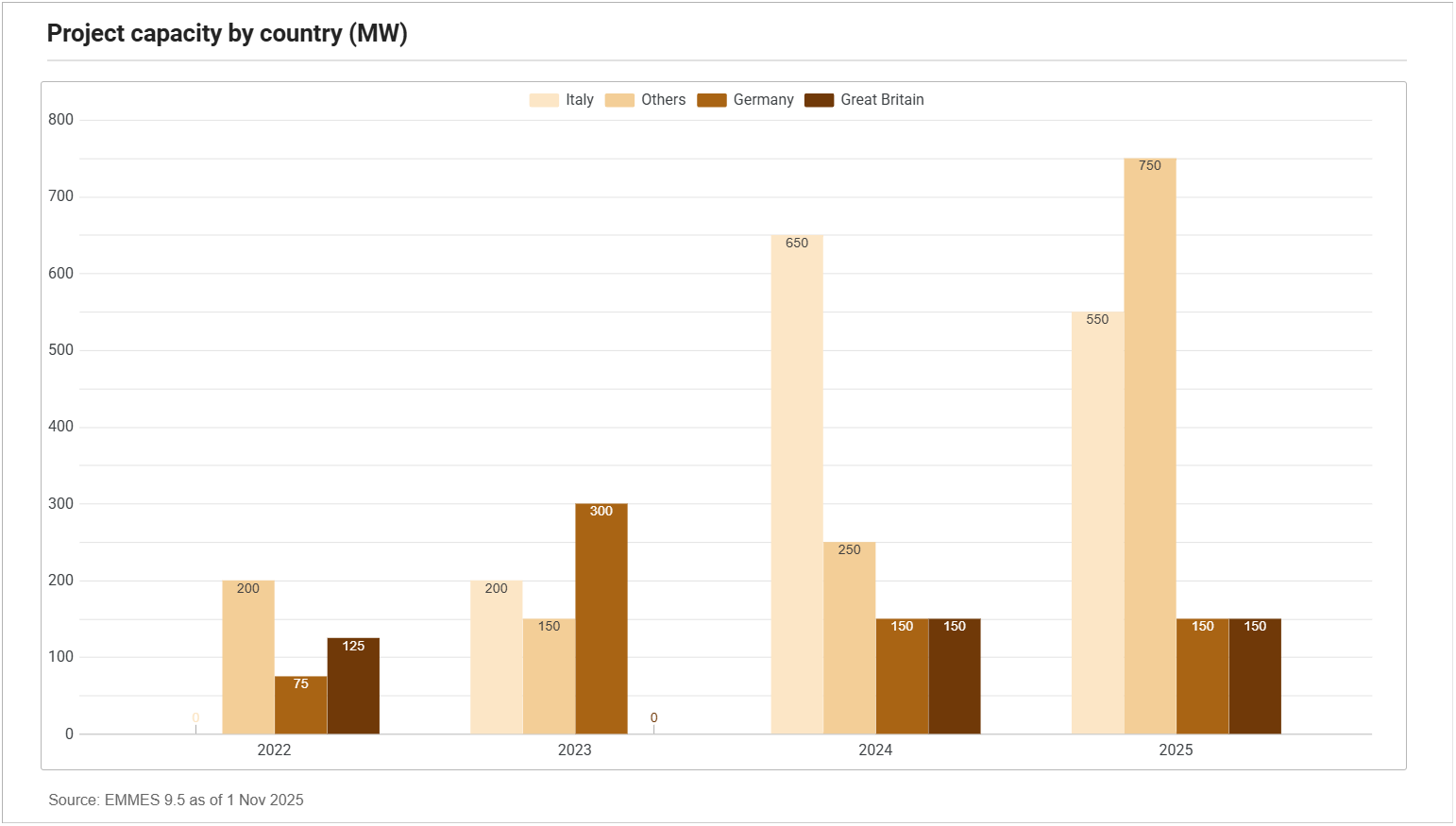

- Italy makes the maturation explicit on the revenue side. Ranked by Aurora as Europe’s most attractive BESS market, the country held its first MACSE capacity auction in late September 2025, awarding all 10 GWh on offer at a weighted average of EUR 12,959 per MWh per year, 65% below Terna’s reserve price

In Italy, bids came in at more than four times the available capacity. The 15-year tolling contracts give awarded projects revenue certainty, but at compressed margins, with most analysts estimating high single-digit IRRs at best.

The sector needs to grow, but the system (from grid availability to capacity) and its logistics chains need to prove capable of keeping pace sustainably.

That transformation should take place under the risk that the paradoxes created in the industry turn investing in the sector into a chess game, rather than the blue ocean that the market narrative had so far encouraged.

Multiple

- Europe | Blackstone Infrastructure Partners agrees up to €2.0B minority investment in Eurowind Energy, accelerating wind, solar and battery expansion across Europe

- Europe | Copenhagen Infrastructure Partners completes acquisition of Ørsted’s European onshore platform and launches Perigus Energy, scaling 826 MW wind, solar and battery portfolio

- Europe | IFM Investors agrees to acquire Trafigura’s remaining 50% stake in Nala Renewables, taking full ownership of multi-technology renewables platform

- Europe | TotalEnergies completes acquisition of 50% of EPH’s 14 GW flexible power platform, creating TTEP to scale flexgen and battery storage

- Global | Kyotherm acquires 155 MW operational portfolio from SEIT for €120 m, expanding biomass, geothermal, co-generation and energy savings assets across six markets

Solar

- Germany | clearvise sells 8.6 MW small-scale PV portfolio to GSP GmbH, reducing operational complexity and refocusing on larger wind and solar parks

- Germany | RP Global acquires and secures bridge financing for 50 MWp Harbke solar PV project, advancing its first German solar development with MaxSolar

- Poland | Greenvolt sells 69 MWdc Skarszewy I photovoltaic project to The Dillinger Group, adding planned solar and BESS expansion under development services agreement

Solar + BESS

- Romania | Vertex Energy takes 49% stake in Kraftfeld Energy’s 61 MWp Măruntei-Vest solar-plus-storage project, backed by €50.4 m financing from Kommunalkredit

- United Kingdom | L&G NTR Clean Power Fund secures 75.4 MWp solar and 49.9 MW/99.8 MWh BESS project from Ridge, expanding hybrid clean energy exposure in England

Wind

- Germany | PNE sells 25.2 MW Bokel wind farm to Union Investment-managed fund, strengthening financial flexibility while retaining operational management through energy consult

- Germany | Stadtwerke Stuttgart acquires 14.4 MW Creußen wind farm repowering project from SOWITEC, expanding own generation portfolio in Bavaria

- Italy | BayWa r.e. sells 48.8 MW Vallelunga wind project to Alerion Clean Power, transferring Sicilian development rights for final design and construction

- Poland | ENGIE Zielona Energia acquires 30 MW Kamionka wind farm from BayWa r.e., expanding its Polish renewables portfolio and onshore wind footprint

- Poland | Greenvolt sold 83.2 MW Pelplin wind farm to Enea Nowa Energia for €174.4 m, contributing to nearly €250 m in Polish asset-rotation proceeds

- United Kingdom | North Star acquires four offshore service operations vessels from Edda Wind, expanding fleet capacity for European offshore wind support services