Sebastian Montoya

Sebastian Montoya

European renewables M&A in Q1 2026 looks selective on the surface, but underneath, the real story is different. This week, Teaser Energy Europe looks into a report from Enerdatics, and the findings reinforce the view that structure and revenue streams are now dominating the buyer’s mind.

Don’t miss the list of M&A deals that happened this week. The highlights are:

- Airengy signed documents covering roughly €51m of transactions in Poland across three segments: A binding offer for 100% of three solar project companies at €20m, implying €595,000/MW with COD targeted for October 2027. A non-binding MoU for eight standalone BESS projects totalling roughly 100 MWh at about €16m, and a non-binding offer for an 8 MW wind project valued at €15m, or €1.9m/MW.

- L’Energètica shortlisted four ground-mounted solar projects totalling roughly 12 MW across Catalonia (in Les Oluges, Sant Pere Sallavinera, Casserres and Vilanova d’Escornalbou) for a combined €12m in its second public procurement round.

- Zenith Energy acquired a 5 MWp solar development project in Puglia for €575,000, with payment contingent on securing permits and reaching Ready-to-Build status. The five hectare site sits roughly 300 metres from an existing Zenith project with grid connection already accepted, and the deal takes the company’s Italian solar development pipeline to 178.5 MWp, recently valued at €54.7m.

Want more insight? Connect with me on LinkedIn to stay on top of Europe’s latest moves.

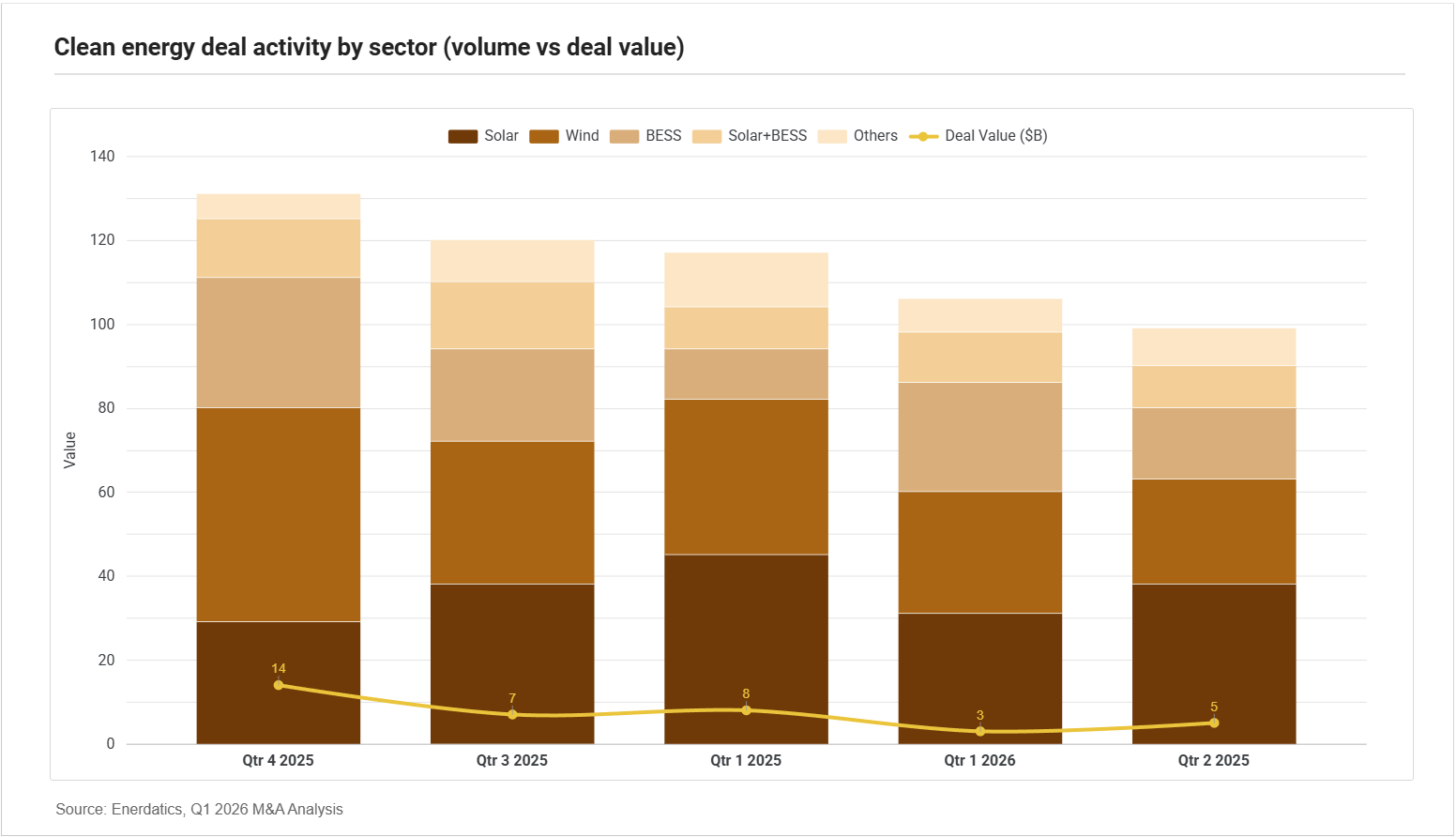

Deals breakdown

The split running through European renewables M&A

The Q1 2026 M&A data points to a market that is not weak so much as increasingly selective.

Recent data published by our friends from Enerdatics shows there was around $3 billion in disclosed European renewable M&A, with solar and wind volumes down 20% to 30% YoY, and 2/3 of deals targeting operational, near-operational or ready-to-build assets.

But that reading misses what is actually moving: not the asset alone, but the combination of execution readiness and revenue architecture.

- BESS deal volume rose 120% year on year to roughly 5.5 GW across 26 deals, with ready-to-build assets emerging as a preferred entry point.

- CfD and FiT-backed solar and wind portfolios are commanding premium valuations across multiple jurisdictions.

- Merchant-exposed assets are facing longer sale processes, heavier diligence and greater pricing friction. The market has not lost appetite. It has reallocated appetite from the asset to the revenue architecture sitting on top of it.

We can find some examples of these movements if we follow the money.

- In Germany, the most recent EEG auction for ground-mounted solar, which closed in December 2025 and was announced in February, cleared at a volume-weighted 5.00 ct/kWh. The three previous rounds had cleared between 4.66 and 4.84 ct/kWh. That puts regulated support in an effective €46.6 to €50/MWh band, locked in for 20 years.

- In Italy, the first FER-X auction awarded 7.7 GW of solar in December 2025 at a weighted average of €56.825/MWh under 20-year contracts for difference, with a second NZIA-restricted round adding 1.1 GW at €66.37/MWh.

- And in the UK, AR7 secured 4.9 GW of solar at £65.23/MWh and 1.3 GW of onshore wind at £72.24/MWh in 2024 prices, indexed to CPI for 20 years.

These benchmarks are not perfectly comparable, given differences in indexation, profile and route-to-market. But directionally they point the same way: regulated or structured revenue is widening its advantage over merchant exposure.

These are not marginal interventions. They’re practical examples of a European market that is once again assigning clear value to revenue certainty.

What does that mean for the merchant side?

The merchant side has moved the other way.

- LevelTen‘s Q4 2025 index puts the continental P25 solar PPA at €57.44/MWh, down about 8% year on year.

- The German P25 sits closer to €52/MWh, down roughly 20% year on year.

- Pexapark recorded disclosed European PPA volumes falling to 13.1 GW across 247 deals in 2025, from 15.3 GW the year before, with Germany suffering the steepest drop among major markets as buyer bids and seller offers stopped overlapping.

None of this signals a sector failing to mature, but a predictable consequence of how the merchant case for standalone solar is being eaten by its own success. Germany cleared 470+ hours of negative prices in 2025, with nearly 30% of solar generation occurring during them. Spain is recording structural curtailment.

In practice, one class of assets now arrives with some form of moderable revenue floor, whether through CfD and FiT-style support in solar and wind, or through mechanisms such as MACSE and tolling in storage.

- In Germany, Pexapark points out that there was no PPA pricing overlap at all in Q3 2025.

- In the UK, the same logic: CfD-backed reference revenues are raising seller expectations relative to what purely corporate offtake can support.

Spain has been showing the same logic for longer.

- In September 2025, Velto Renewables agreed to acquire 260 MW of regulated PV from Bankinter Investment and Plenium Partners for approximately €1.1 billion, with closing expected by April 2026, a valuation of around €4.2 million per MW.In February, IST3 Infrastruktur Global acquired a 91 MW regulated portfolio from Bestinver Infra FCR, Acciona’s asset management platform, for more than €330 million, or roughly €3.6 million per MW.

These multiples only make sense in one context: cash flows shaped by the regulatory framework itself, with the operating risk substantially compressed.

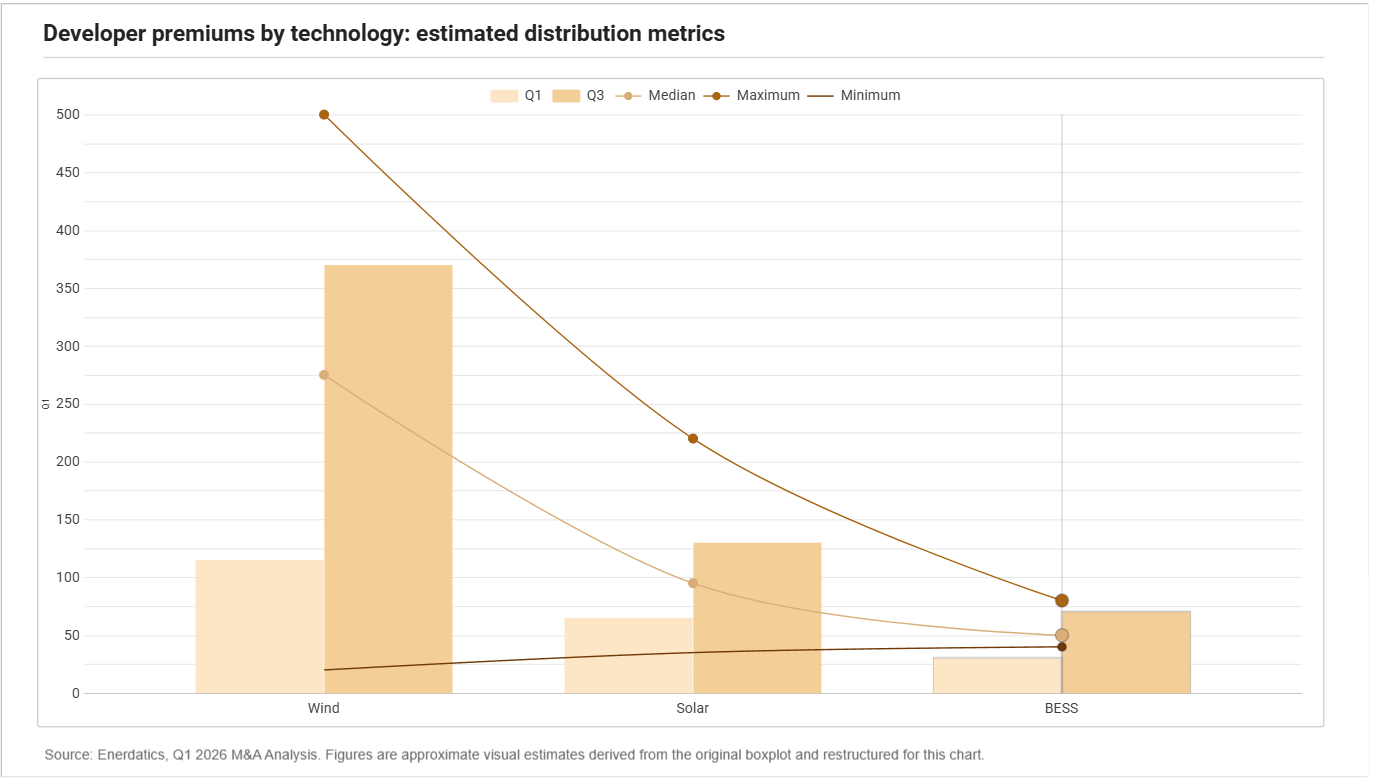

Different mechanics, same shift: how is BESS playing out?

BESS sits inside the same shift, but by a different route.

The mechanics are different from solar CfDs, but the underwriting question is the same: what part of this revenue can a lender model out, and what part is left to the market?

- Italy’s first MACSE auction awarded 10 GWh under 15-year contracts at roughly €13,000/MW/year, well below the €37,000 cap. The clearing price alone does not pay for the asset. What it does is provide a contractual floor that lets developers stack arbitrage and ancillary revenues on top of bankable income.

- In the UK, Drax has signed early 2026 tolling agreements with Fidra Energy for 250 MW and Zenobē for 200 MW.

Subsidy, capacity payment, tolling, FiT legacy. The specific architecture varies by jurisdiction, but the function is the same: provide a revenue floor that survives cannibalization, negative pricing, and capture-rate compression. Renewables stay strong, but investors are retreating from generation as a standalone proposition.

For sellers, the implication runs through the entire transaction. An asset arriving in the data room without a clear revenue narrative is now in a different process from one that arrives with contracted income attached. The diligence is longer, the price discovery is harder, and the binding offer is less likely to come at all.

In Q1 2026 eyes turn to the structure that explains how that power gets monetised through the cycle. If you’re still looking only for megawatts, maybe it’s time to review the mindset.

Battery storage

- Finland | FP Lux European Battery Storage Fund acquires 95 MW/220 MWh BESS project from SMA Altenso and partners, expanding Nordic storage portfolio ahead of construction phase

- Germany | AllianzGI acquires 51% stake in battery storage platform GESI with 2.6 GW pipeline, expanding exposure to large-scale grid flexibility infrastructure

- Spain | Reden partners with Circle Energy to co-develop up to 200 MW standalone BESS pipeline, marking entry into Spanish storage market and supporting grid flexibility

Multiple

- Europe | Masdar and EPCG agree to form 50/50 joint venture to develop multi-technology renewable energy projects, supporting domestic supply and regional electricity expor

- Poland | Airengy explores €51 m acquisitions across solar, 100 MWh BESS and 8 MW wind projects, building multi-technology renewables platform

Solar

- France | Girasole Energies acquires 30 MWp portfolio of photovoltaic carport projects, expanding distributed solar footprint to support growth towards 500 MWp target

- Italy | Zenith Energy acquires 5 MWp photovoltaic development project in Puglia for ~€0.6 m, expanding Italian solar pipeline

- Spain | L’Energètica launches €12 m programme to acquire 1–5 MW photovoltaic plants, expanding public renewable portfolio in Catalonia

Solar + BESS

- Austria | Wien Energie acquires 11.8 MWp Stans solar farm from GEG Ökostrom with plans for co-located 12 MWh BESS, expanding domestic renewable portfolio

- Denmark | Alight acquires 79 MWp solar and 55 MW BESS project from GreenGo Energy, expanding hybrid renewables pipeline through first integrated solar-plus-storage asset in Denmark

Wind

- France | Banque des Territoires sells 49.9% stake in 107 MW onshore wind portfolio to Octopus Energy Generation, continuing portfolio rotation strategy

- United Kingdom | Fred Olsen Seawind agrees to acquire Vattenfall’s 50% stake in Muir Mhòr floating offshore wind project, taking full ownership to advance development off Scotland