Sebastian Montoya

Sebastian Montoya

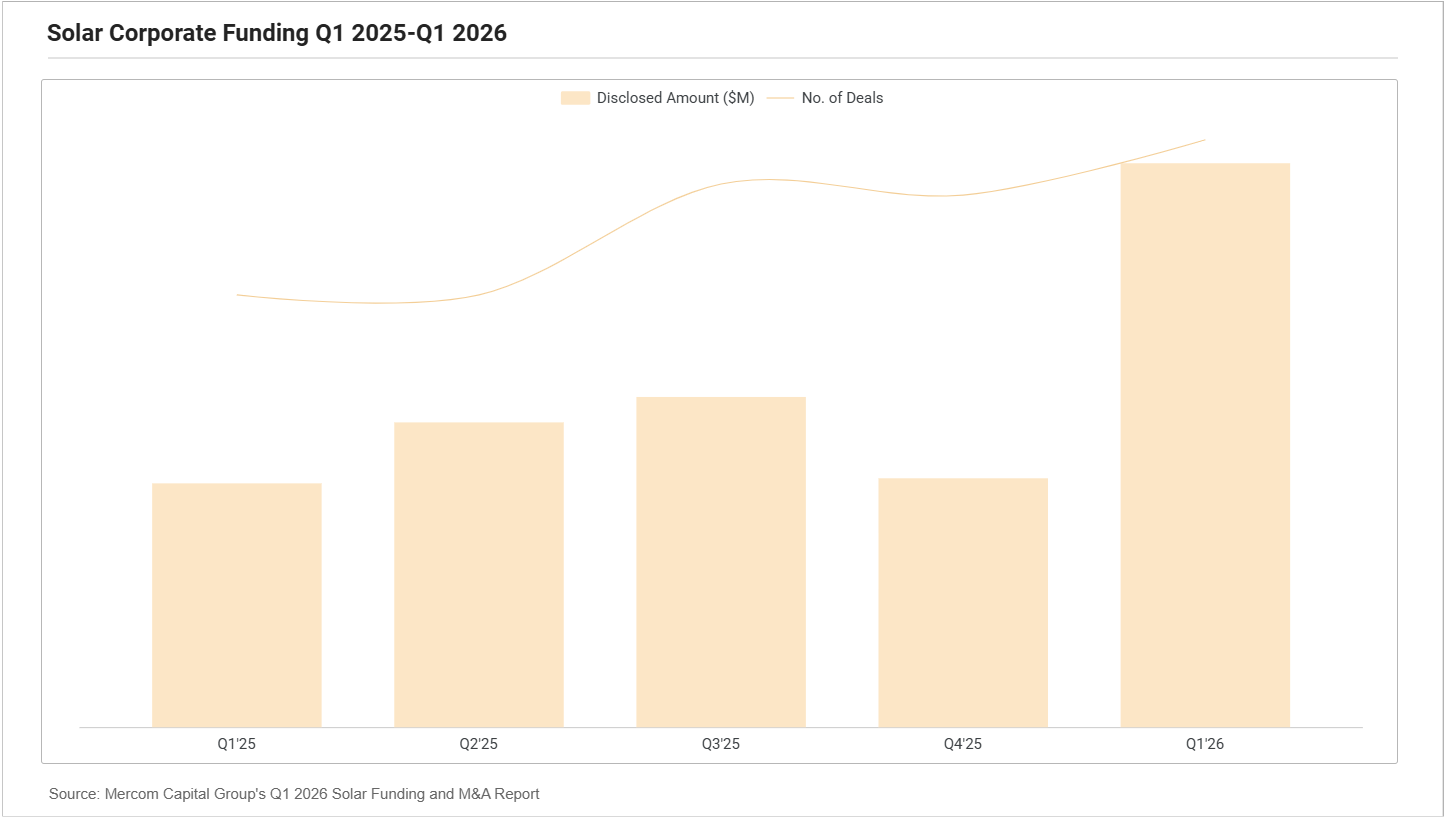

In Q1’26, solar funding grew 131% YoY. In this edition of Teaser Energy Europe, we look at the recently released Mercom Capital data for the period to understand how the composition of financing in the sector reflects market sentiment.

Also, make sure to check out our deals tracker. This week’s highlights are:

- Octopus Energy Generation acquired a 321 MW onshore wind portfolio across France, Germany and Poland in a deal worth nearly EUR 600m. The assets include eight operational wind farms and mark another step in Octopus’ push to scale its European renewables platform.

- Repsol reportedly agreed to sell a 49% stake in its 706 MW Minerva wind and solar portfolio in Spain to Masdar, in a transaction valuing the assets at around EUR 850m. The deal would deepen Masdar‘s Spanish renewables footprint while allowing Repsol to continue rotating capital from mature assets.

- Acciona Energía reportedly launched the sale of a 361 MW operational wind portfolio in Spain, with the assets potentially valued at up to EUR 400m. The process would support the company’s asset-rotation strategy as Spanish wind portfolios continue to attract infrastructure and strategic investors.

Want more insight? Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

Solar funding grows 131% YoY, but exceeding expectations is becoming increasingly complex

Appetite for solar is back. Data from Mercom Capital Group’s Q1 2026 Solar Funding and M&A Report points to a sector that reached USD 11.1bn globally across 53 deals, a 131% increase YoY and 127% versus Q4 2025.

The volume is impressive, but the real insight lies in the composition.

- The bulk came from debt, with USD 8.9bn invested across 28 transactions.

- Venture capital pulled back, totalling USD 1.1bn across 17 deals and falling 21% YoY.

- In parallel, 28 corporate M&A transactions and 18.4 GW of solar projects changed hands, up 33% compared to 21 solar M&A transactions in Q4 2025.

The drop in risk capital alongside growing debt points to an interesting shift. Solar assets remain a comfort zone for financing and consolidation, but growth is no longer linear. The sentiment here echoes themes that have run through recent editions of Teaser Energy Europe: negative prices, curtailment and pressure on grids, the defining challenges of renewables.

Pure risk is no longer as appealing. The maturity and bankability of the sector remain intact, but the way strategies are being structured is undergoing a relevant shift. Looking at debt and M&A is the most revealing angle. The focus is sliding towards platforms capable of operating portfolios with mitigated risk, greater financing clarity and viability, and controlled complexity.

In Europe, the transition is not only visible but also has deeper roots. The region installed solar at an accelerated pace throughout the decade, with EU solar PV capacity reaching an estimated 406 GW in 2025, nearly tripling since 2020. The result is a cleaner mix, but also a system that is harder to operate and showing mild signs of saturation, signs that contrast with the grid’s ability to accommodate all this new generation.

On days of high irradiation and low demand, solar generation pulls down wholesale prices, pressures dispatchable plants to reduce output and, at times, drives prices into negative territory.

- In Iberia, for example, Spain recorded 397 hours of negative prices between January and March 2026, against 48 hours in the same period of 2025.

The contrast between opportunity and challenge in renewables is complex to navigate, especially considering that these challenges are structural and cross-sectoral, and so are their consequences. Investing in storage and hybrid models, for instance, is seen as an executable way out, but even this approach is gaining complexity.

There is no recipe for this challenge. Capturing opportunity in renewables also means dealing with complexities that demand thinking outside the box. The numbers in the sector are impressive, but strategies need to be even more so.

Battery storage

- Belgium | Aquila Clean Energy divests minority stake in 100 MW / 250 MWh Flanders BESS portfolio to AEB Energy Storage, supporting Belgian grid stability

- Netherlands | Vopak agrees in principle to acquire majority stake in Green Energy Storage, supporting development of Dutch BESS pipeline including 200 MW / 800 MWh Oosterhout project

- Poland | EDF Renewables Polska and Eurus Energy Europe secure European Commission approval for 120 MW Kobiernice BESS JV, advancing Polish battery storage pipeline

- Spain | Acciona Energia reportedly launches sale of 361 MW operational wind portfolio, advancing asset rotation with valuation potentially reaching €400 m

- United Kingdom | Elements Green acquires 300 MW Newarthill BESS project from Geocore, strengthening UK transmission-connected storage pipeline

Multiple

Solar

- France | ENGIE completes sale of residential solar subsidiary Engie My Power to unnamed buyer, refocusing on core large-scale renewables and network assets

- Italy | Altea Green Power acquires 100% of NB5 Srl and 16.75 MW operational photovoltaic plant, strengthening its independent power producer strategy

- Italy | Fervo acquires BayWa r.e. Power Solutions from BayWa r.e., expanding photovoltaic EPC capabilities and strengthening energy services growth strategy

- Italy | Verdian acquires 117 MWp ready-to-build agrivoltaic solar portfolio in Sicily from Genertec International Holding, expanding Italian platform with FER X-backed assets

Wind

- Europe | Octopus Energy Generation acquires 321 MW onshore wind portfolio across France, Germany and Poland, investing nearly €600 m to expand European renewables platform

- Germany | Diehl Group acquires ~25 MW Gundersweiler 2 wind farm from JUWI, expanding its green self-generation portfolio

- Germany | Encavis acquires 80 MW Vietlübbe onshore wind farm from UKA Group, marking its largest German wind acquisition to date