Sebastian Montoya

Sebastian Montoya

Europe’s new renewables cycle is being written by the buy side: as negative prices normalise and PPA volumes cool, they’re the ones dictating terms.

This week, we’ve unpacked a handful of recent reports to extract the key signals behind that shift — alongside the week’s standout deals, including:

- Platinum Equity has this week signed a definitive agreement to sell the Urbaser environmental infrastructure platform to funds managed by Blackstone Infrastructure and EQT for US$6.6b. Platinum initially acquired Urbaser in October 2021 for an enterprise value of US$4.2bn. At this size, full-scale platform trades remain rare in today’s market.

- IST3 Infrastruktur Global has acquired a 91MW regulated solar PV portfolio from Bestinver, with the deal valued at an enterprise value of €330m. For IST3, this means regulated revenues with some wholesale upside, signaling that capital remains committed to renewables, but it is flowing most decisively into lower-volatility assets.

- BNP Paribas has taken a strategic equity stake in Eclipse to support its 850MW BESS pipeline across France and Belgium. While the investment size was not disclosed, the partnership combines capital, financing and long-term contracts designed to reduce merchant exposure. Storage? Yes. But structured with revenue stability in mind.

Want more insight?

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

Energy M&A in the UK: Cocktails & Conversations

The UK energy and infrastructure market continues to command global attention. Robust regulatory frameworks, targeted government backing, and sustained growth across offshore wind, hydrogen and smart grid technologies are fuelling a new wave of M&A activity.

What does this mean for investors, operators and dealmakers?

Meet us at Black Lacquer at Hyde London City for an exclusive evening of high-level networking and sharp market insight.

Buyers have all the power, and Europe’s renewable contracts are starting to read like it

In previous editions of Teaser Energy Europe we’ve tried to keep the renewables M&A chessboard as transparent as possible: where demand is turning elastic, where “just add MW” stopped being a negotiating trump card, and where revenue is increasingly written in footnotes (capture, curtailment, shape).

This time, the focus is on the piece that has quietly become the king:

The buyer.

- Not the buyer as a logo on a press release — but the buyer as the organiser of risk, revenue and optionality. The one rewriting term sheets rather than debating whether the project is “subsidy-free”.

Pexapark’s read is blunt — and it confirms a trend that has been building for years: corporates accounted for 83% of all signed PPAs in Europe in 2024, making corporate offtakers the market’s main engine.

The important part is not the percentage itself. It’s what it implies: the centre of gravity has moved from generators needing demand, to demand choosing generators.

The price signal that changed the tone of every negotiation

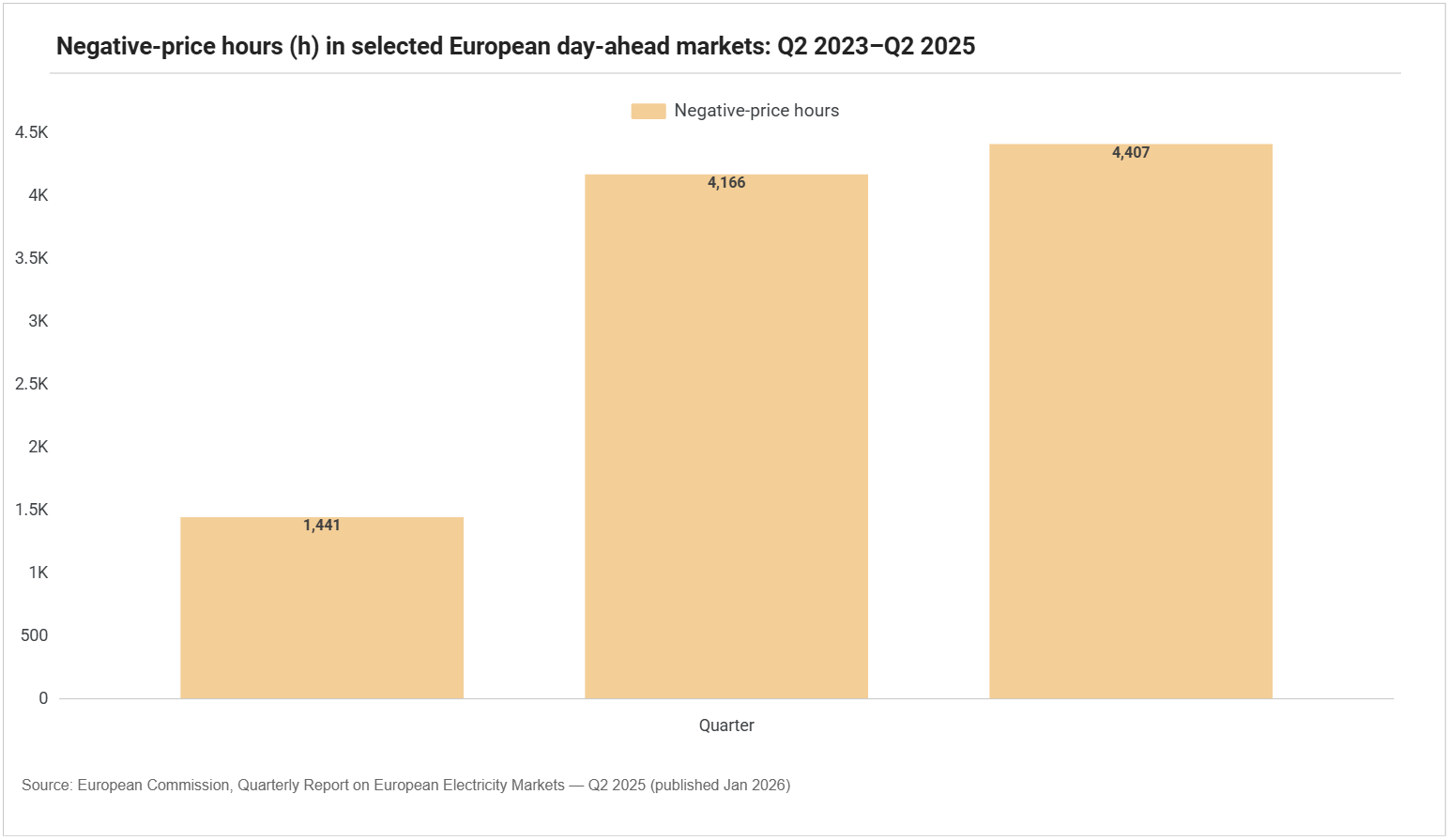

In a market where negative pricing is frequent, “merchant tails” are no longer tail events. They are line items.

The European Commission’s latest quarterly electricity market report (published in January 2026, covering Q2 2025) shows 4,407 hours of negative wholesale prices across selected European day-ahead markets in Q2 2025, up from 4,166 hours in Q2 2024 (and versus 1,441 hours in Q2 2023).

Buyers see it in the tape — and it’s now embedded in their M&A maths. PwC’s 2026 Energy, Utilities & Resources M&A outlook flags a very 2025-shaped pattern:

- Deal values rose 27% while volumes fell 2%, driven by 20 megadeals ($5bn+) versus six in 2024;

- Fewer tickets, bigger cheques, and a sharper preference for assets where downside is contractable (or hedgeable) rather than simply “assumed away” in a merchant model.

And in renewables specifically, our friends at Enerdatics reported 2025 renewable M&A at $87bn globally (about $33bn in Europe) and clearly shows where capital clustered:

- Execution‑ready;

- Frid‑secured portfolios;

- Emphasis on battery storage, hybrids, and platform‑scale consolidation.

These are precisely the structures that turn price volatility into controllable cashflows.

2025 didn’t break the PPA market. It showed who could set the terms.

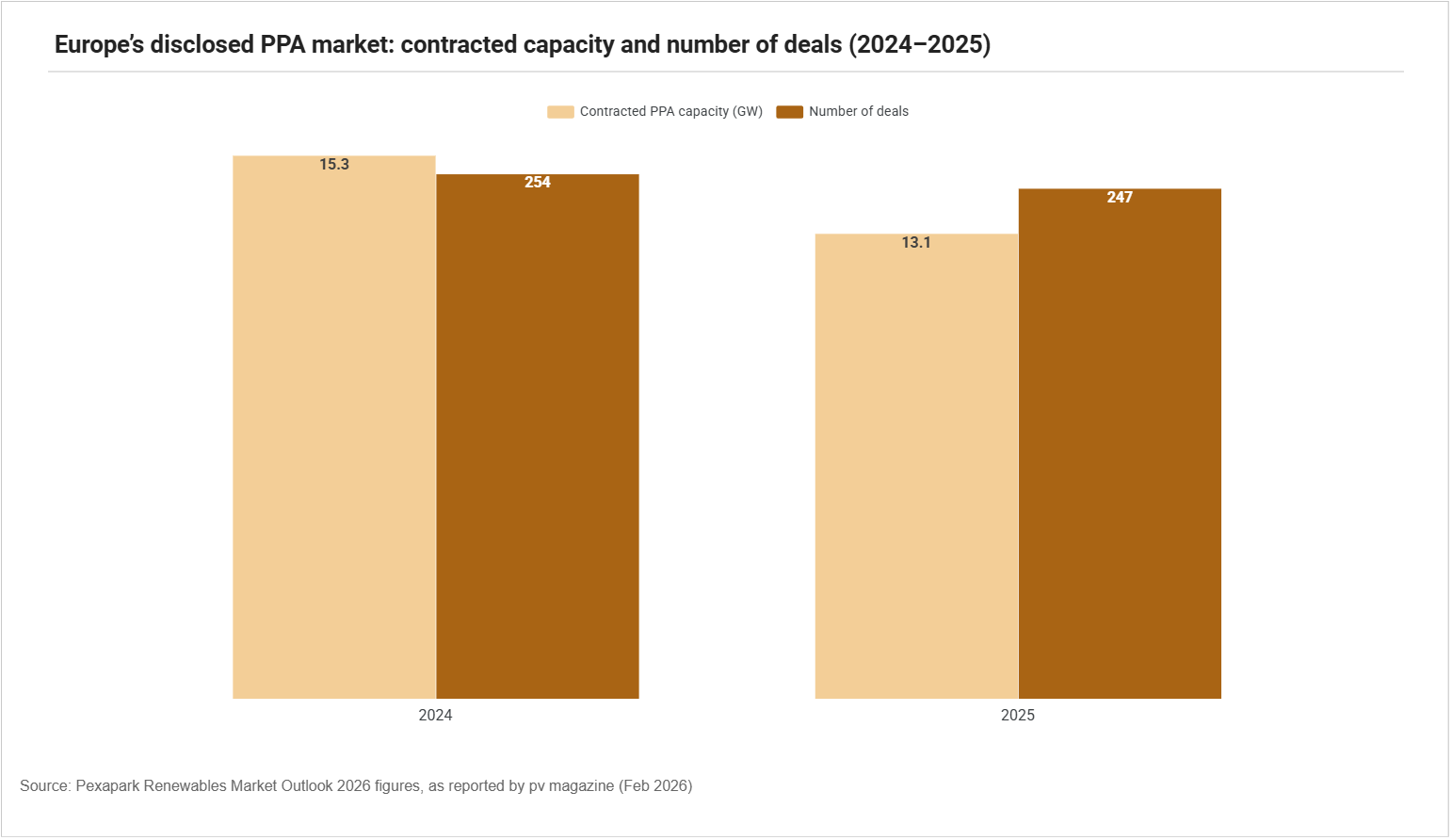

If you want the clearest signal of control, look at volumes — and what happens when the market cools.

According to Pexapark’s Renewables Market Outlook 2026, disclosed contracted PPA capacity in Europe fell to 13.1 GW across 247 deals in 2025, down from 15.3 GW across 254 deals in 2024.

- In a seller-led market, falling volumes would signal shrinking opportunity.

- A buyer-led market reads it differently: when supply keeps expanding but contracted volumes soften, the buyer can be patient.

And patience, in markets like this, is leverage.

Buyer power is no longer only corporate. It’s becoming systemic.

Another change in Europe is who “the buyer” is.

It’s no longer only a company signing a long-term contract. More and more, it also includes households and service providers that can shift electricity use to different times, and even make money by doing so. Delta’s Market Monitor 2025 shows that buyer optionality is already material in parts of the region.

- In Finland, smart meters are fully rolled out and about 25% of customers use prices that change during the day.

- In the Netherlands, smart meters are widespread (89%), but only a small share of customers use variable pricing: 4% of households and 9% of business customers.

- Germany is at the other end: only 4% smart meter rollout and just 1% using dynamic tariffs.

The data reveals an old truth — now with renewed urgency: buyer power grows where the tools and market access exist.

Where the “menu” is richer (variable tariffs, consumption management services, multiple flexibility revenue streams ) buyers don’t just negotiate. They compare, arbitrage and wait.

Once buyers can do that, price-setting power shifts structurally.

Battery storage

- France | BNP Paribas takes equity stake in Eclipse to finance and commercialise 850 MW battery storage pipeline across Europe

- Germany | Masdar and RWE sign MoU to invest in up to 2 GW of BESS projects, expanding battery storage to support energy transition in Germany and Europe

- Germany | ZE Energy signs agreement with SPP for 145 MW / 300 MWh BESS portfolio, expanding large-scale battery storage footprint

Multiple

- Europe | Platinum Equity agrees $6.6bn sale of Urbaser to Blackstone and EQT, exiting Madrid-based environmental infrastructure platform after multi-year transformation

- Spain | Cemex Ventures increases stake in WtEnergy to scale waste-to-fuel and clean hydrogen technology, backed by €4.4m EU Innovation Fund grant

- Spain | Pamesa owner Fernando Roig to take stake in Umbrella via €5.7m debt-for-equity swap, strengthening clean energy developer’s balance sheet

Solar

- Azerbaijan | bp sells 10% stake in 240 MW Shafag Jabrayil solar project to MVM, reshaping shareholder structure ahead of 2027 completion

- France | Sonnedix acquires six operating PV plants and 50% stake in high-voltage substation, expanding French portfolio towards 400 MWp

- France | TSE acquires 108 MWp of ground-mounted solar projects across multiple regions, positioning as consolidation platform in French PV sector

- Ireland | ib vogt completes sale of 272 MWp solar portfolio to international investors, advancing Ireland’s renewable energy transition with three major projects

- Spain | IST3 acquires 91 MW regulated solar portfolio from Bestinver for over €330m, expanding Swiss pension-backed footprint in Spanish renewables

- Sweden | Alight acquires 23 MWp solar project from Better Energy, expanding domestic pipeline with Rabobank-backed financing and planned 2027 grid connection