Sebastian Montoya

Sebastian Montoya

Welcome to the second edition of Teaser Energy Europe in 2026. Our first edition set the macro backdrop for the year ahead. This week, we zoom in, examining how clean energy M&A is beginning to translate from sentiment into deal structures, capital allocation and execution.

That distinction matters, because while optimism is back, capital is moving with discipline. You can see it in the week’s leading transactions:

- A mega offshore wind JV just landed in the UK. KKR and RWE are forming a 50:50 partnership to develop 3 GW across Norfolk Vanguard East & West, a system‑scale build that can meaningfully move the UK decarbonisation needle.

- Europe’s biomethane roll‑up is getting real money behind it. Asterion is committing €1.5bn to scale ABIO into a pan‑European biomethane platform, targeting 3 TWh of production and fast multi‑country expansion.

- UK utility‑scale solar is going into programmatic mode. Downing and Tokyo Century have agreed a £300m+ joint investment programme to acquire and build 500 MW of solar, a repeatable capital engine that can accelerate pipeline delivery (and sets up nicely for solar‑plus‑storage pairing).

Continue reading for more insights and connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

Clean energy M&A in 2026 will reward execution, not optimism

We spoke in our last edition about optimistic expectations for 2026. And yes, they exist. But hold your horses, clean energy dealmaking is still working through a reset. Not a collapse. Not a party. A reset.

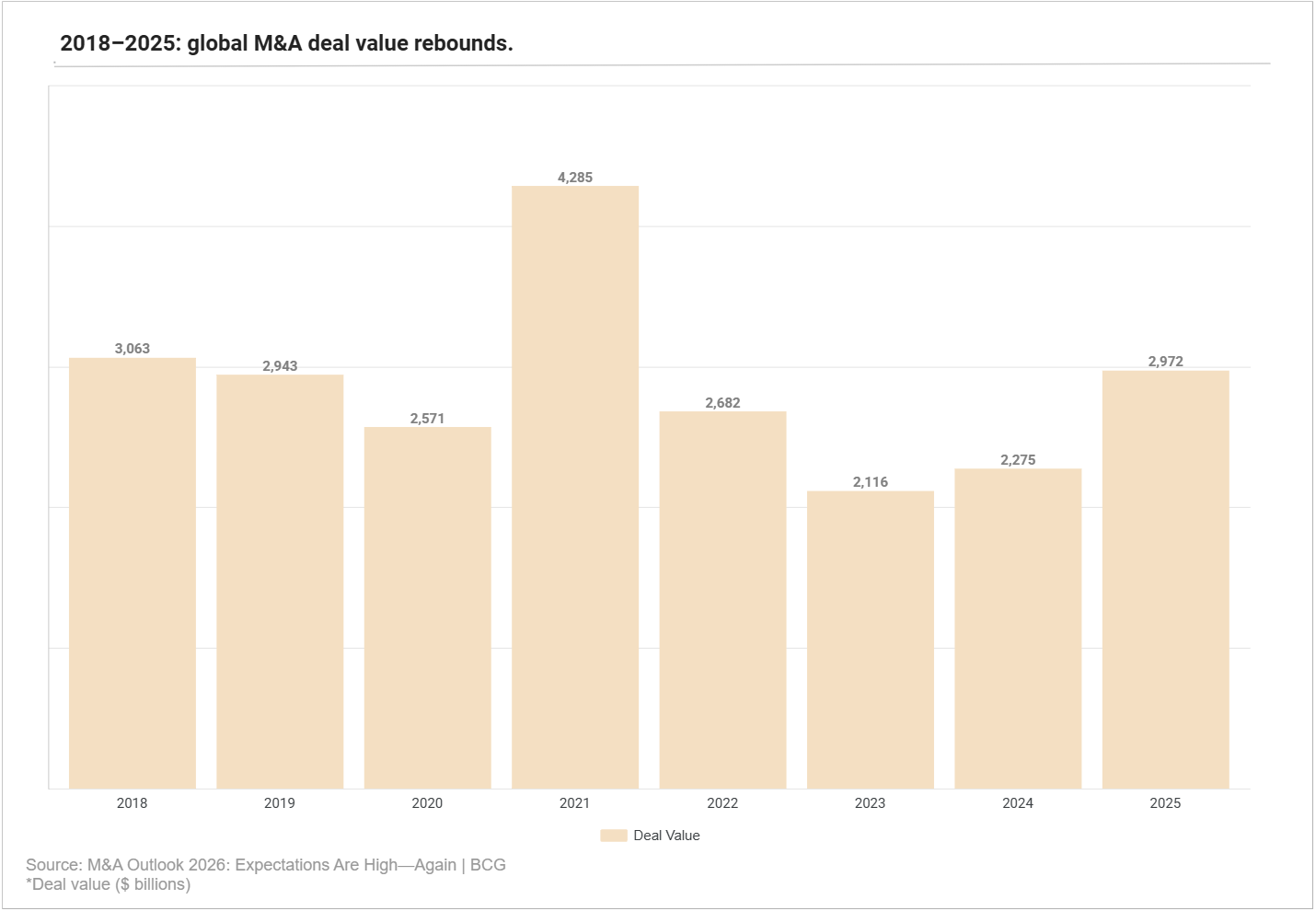

Start with the headline that everyone wants to believe: global M&A is moving again. BCG puts 2025 announced majority-deal value at US$3.0tn, up 31% year-on-year. Yet the rebound is being driven mainly by larger transactions, not a broad-based surge in volumes.

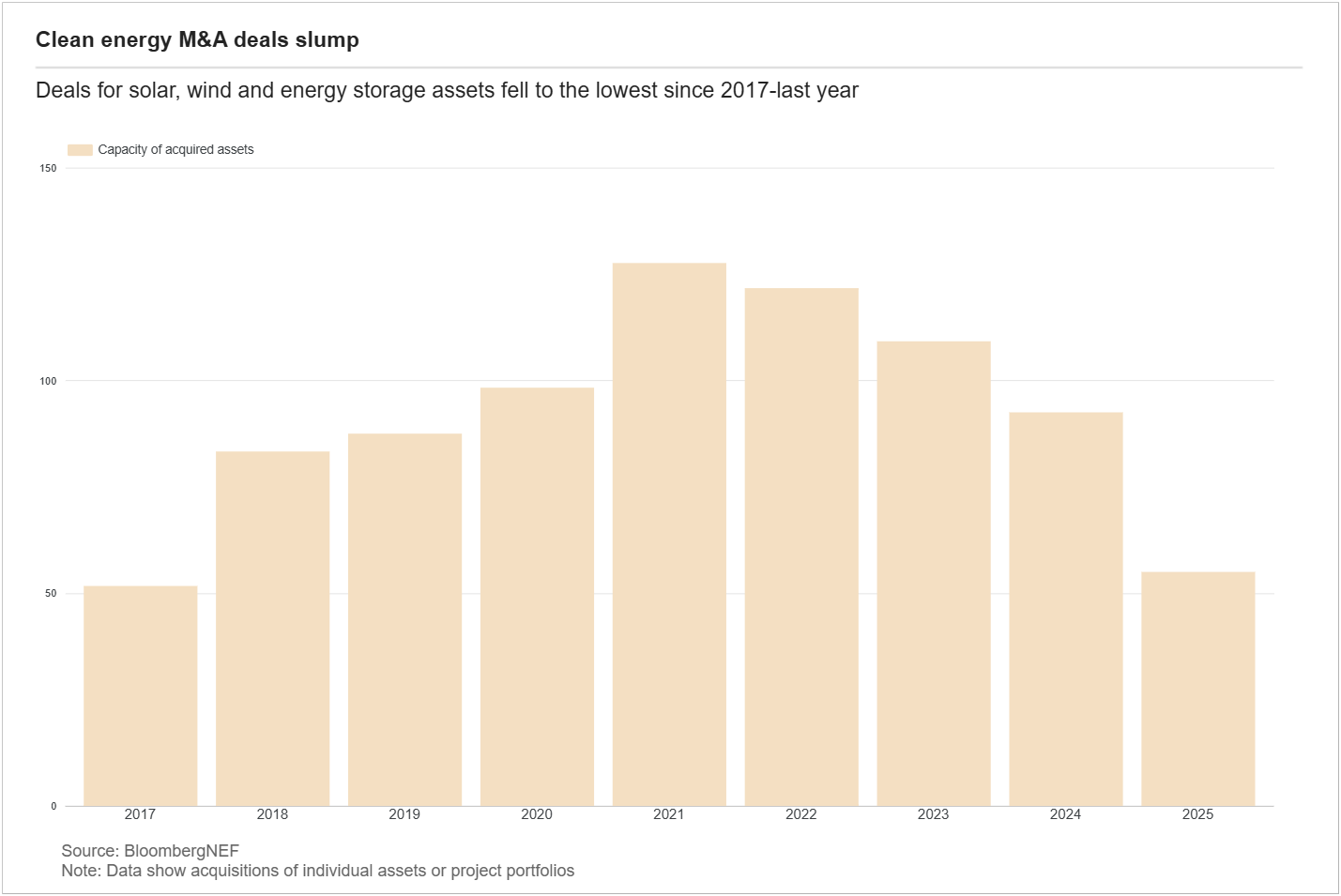

Now the reality check: clean energy didn’t ride that wave in the same way. BloombergNEF data shows that completed acquisitions of solar, wind and energy storage assets totalled 55.3GW in 2025, the lowest since 2017.

So when dealmakers talk about a 2026 revival, what do they actually mean? The Financial Post article gives a very practical answer: price expectations are converging. Sellers have been more willing to come down; buyers have been more willing to pay.

But the important nuance is where buyers are willing to pay. Brookfield’s Daniel Cheng, quoted in the same piece, points to a preference for operational projects with a credible offtake customer, rather than assets still in development, because development risk is still real, and still painful.

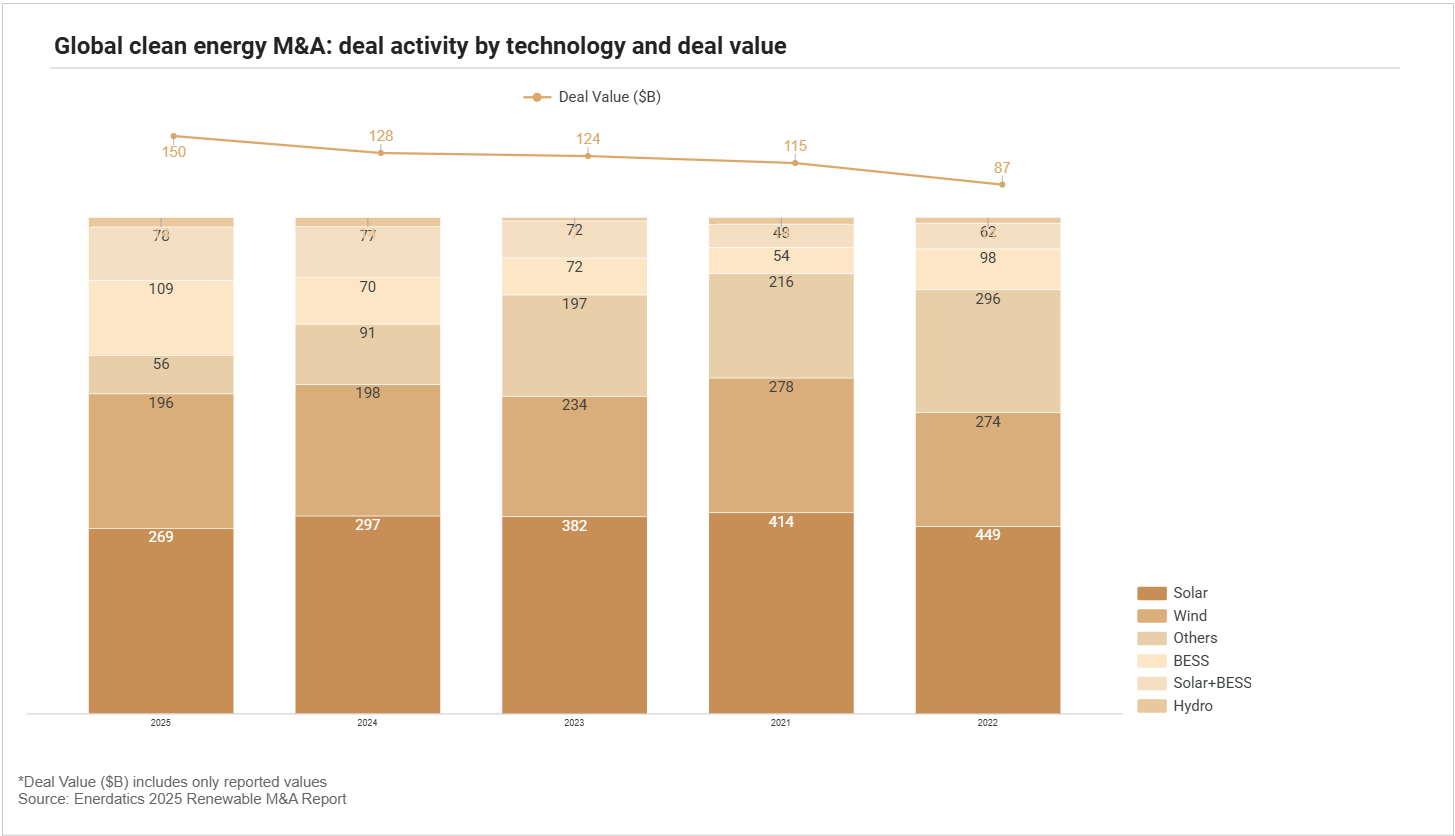

That emphasis on deliverability shows up even more strongly in Enerdatics’ 2025 renewables readout. Their language is blunt: the global renewables M&A market “recalibrated” in 2025, with reported deal value at US$87bn, as tighter financing conditions and policy shifts increased selectivity and dealmaking became increasingly biased towards execution-ready, grid-secured assets.

This is also where the European angle becomes more distinctive and, frankly, more interesting than another generic “rates are easing” story.

Enerdatics says Europe anchored global value in 2025 at around US$33bn, with a “pronounced shift toward flexibility”. They highlight BESS momentum in Europe (up 40% YoY), with 72GW traded across 73 deals, while wind stayed steady across core markets.

These perspectives combined provide an interesting shift. Instead of framing 2026 as a corridor reopening, we can also frame it as a quality filter tightening:

- Grid access and route-to-market are no longer footnotes: they’re value drivers. Enerdatics expects 2026 to be defined by execution certainty, with buyers repricing development risk and leaning harder on structured deals (forward purchases, milestone-based closes, contingent pricing).

- Deal processes are not getting easier, even if the mood is improving. Herbert Smith Freehills Kramer describes 2025 as full of buyers and sellers “hanging out” and stuck in “situationships”, with “heavy lifting” required to get deals done. More diligence, more negotiation around risk, and more creativity to bridge valuation gaps.

- And even the “electricity demand will save everything” story deserves a pause. In a separate angle on AI and electrification, Enverus Intelligence Research flags catalysts that could reset expectations in 2026, including demand moving behind-the-meter and long-term load forecasts being revised down in some US markets. You don’t have to agree with the call to respect the implication: narratives can move faster than realities, and M&A pricing is adjusting accordingly.

Put it all together and the message for clean energy M&A 2026 is straightforward: Yes, there is appetite. Yes, there is capital. But capital is paying for delivery, for assets that are grid-secured, credibly contracted (or close to it), and structurally positioned for a system that increasingly values flexibility.

If you’re looking for the “vibe” of the year: 2026 seems not to be shaping up as a return to speed-dating auctions. It’s closer to what one adviser described as a market learning to go official again: selectively, and with the paperwork in order.

Battery storage

- Czech Republic | Altris and Draslovka form strategic partnership to produce sodium-ion cathode materials at Kolin facility, supporting Europe’s battery supply chain localisation

- United Kingdom | Elements Green acquires 148.8 MW Bolney Green battery energy storage project from Envirotech Energy Solutions, expanding its UK BESS portfolio and grid-scale storage footprint

Bio-fuels

- Europe | Asterion Industrial Partners commits €1.5bn to scale pan-European biomethane platform ABIO, targeting ~3 TWh of production and rapid multi-country expansion

- Spain | Haffner Energy and Ignis P2X launch AeroVerde partnership to develop bio- and e-SAF production, starting with pilot sustainable aviation fuels project

Multiple

- Montenegro | Masdar and state utility EPCG weigh joint venture to develop large-scale multi-technology renewables, targeting domestic supply and regional power exports

- North Macedonia | Stenton Gradba and EDACS-International plan joint venture to develop renewable electricity projects, forming Skopje-based KES Properties

Solar

- Germany | Trianel sells 38.5 MWp Brandenburg solar park to HIH Invest for HIH Green Energy Invest fund, recycling capital after turnkey delivery and commissioning

- United Kingdom | Anesco acquires 36 MWp Beachampton solar farm from One Planet Developments, expanding its UK solar pipeline and supporting delivery of low-carbon power with biodiversity net gains

- United Kingdom | Downing and Tokyo Century agree £300m+ joint investment programme to acquire and build ~500 MW utility-scale solar portfolio, backing UK clean energy growth

Solar + BESS

- Germany | CleanCap advises Spring Creek on investment into 500 MWp+ solar PV and 2.5 GW BESS development portfolio with MEC Energy, backing large-scale hybrid renewables build-out

- Germany | Milvio Energy completes forward sale of 80.4 MWp co-located solar PV and 70.2 MW BESS project in Lower Saxony, highlighting strong investor demand for hybrid developments

Wind

- Germany | Blue Elephant Energy acquires 381 MW onshore wind portfolio in Mecklenburg-Western Pomerania from WIND-projekt, tripling its German wind capacity and strengthening its position in a core market

- Germany | SeaRenergy Offshore Holding acquires 100% of hemmerschütz Solutions, strengthening its integrated service offering and positioning as a one-stop shop for offshore wind projects

- Turkey | RES completes sale of 60 MW Demirli onshore wind project to Reges Elektrik, exiting Turkish asset following permitting and licence award

- United Kingdom | KKR and RWE form 50:50 joint venture to develop ~3 GW Norfolk Vanguard East and West offshore wind projects, backing large-scale UK decarbonisation and capacity growth

- United Kingdom | Triple Point partners with Thrive Renewables and TopCashback Sustainability to arrange construction debt for 57 MW Whitelaw Brae onshore wind project in the Scottish Borders