Sebastian Montoya

Sebastian Montoya

For anyone who reads as many reports as I do, understanding the state of European clean energy M&A can feel a lot like piecing together different parts of a puzzle.

This week, we bring data from CBRE that ties together some of those pieces we have highlighted in recent editions within a broader context of transformation: challenges and opportunities are piling up against a sensitive geopolitical backdrop, and the impact will be clearly felt in 2026 deals.

And, of course, we also have this week’s standout deals. Among them are:

- Capital Dynamics and Solo Renewables agreed a £100m JV for a 150 MW long-duration energy storage project in Northern Ireland. The project has 1,200 MWh of capacity and has been described as one of the first large-scale LDES systems in the Irish Single Electricity Market.

- European Energy sold the hybrid Jonava project to Energix for up to €18.9m, with planned capacity of 470 MW. The asset sale covers a ready-to-build hybrid package including around 140 MW of wind, 330 MWp of solar PV and 320 MWh of storage.

- Capital and pipeline come together in EBRD’s €50m investment in Green Genius, which continues to advance a 1.9 GW pipeline across Lithuania, Latvia and Poland. Through the transaction, the EBRD increased its equity stake in the project and supported Green Genius’s growth strategy, with a particular focus on battery projects, including one of the first BESS projects in Lithuania.

Want more insight? Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Energy M&A in Iberia: Cocktails and connections

The Iberian energy market continues to lead the way in the European transition, driven by significant investment in renewables and a robust pipeline of infrastructure projects.

Join the M&A Community and Ideals for an exclusive networking evening at Casa Suecia. We’ll gather to discuss the evolving landscape of the Spanish energy sector at this stylish venue in the centre of Madrid.

Deals breakdown

Where European clean energy fits in a $300 billion infrastructure year

Infrastructure had a record year, and CBRE’s data now points that the question is who actually captured it (and what that tells us about where Europe stands).

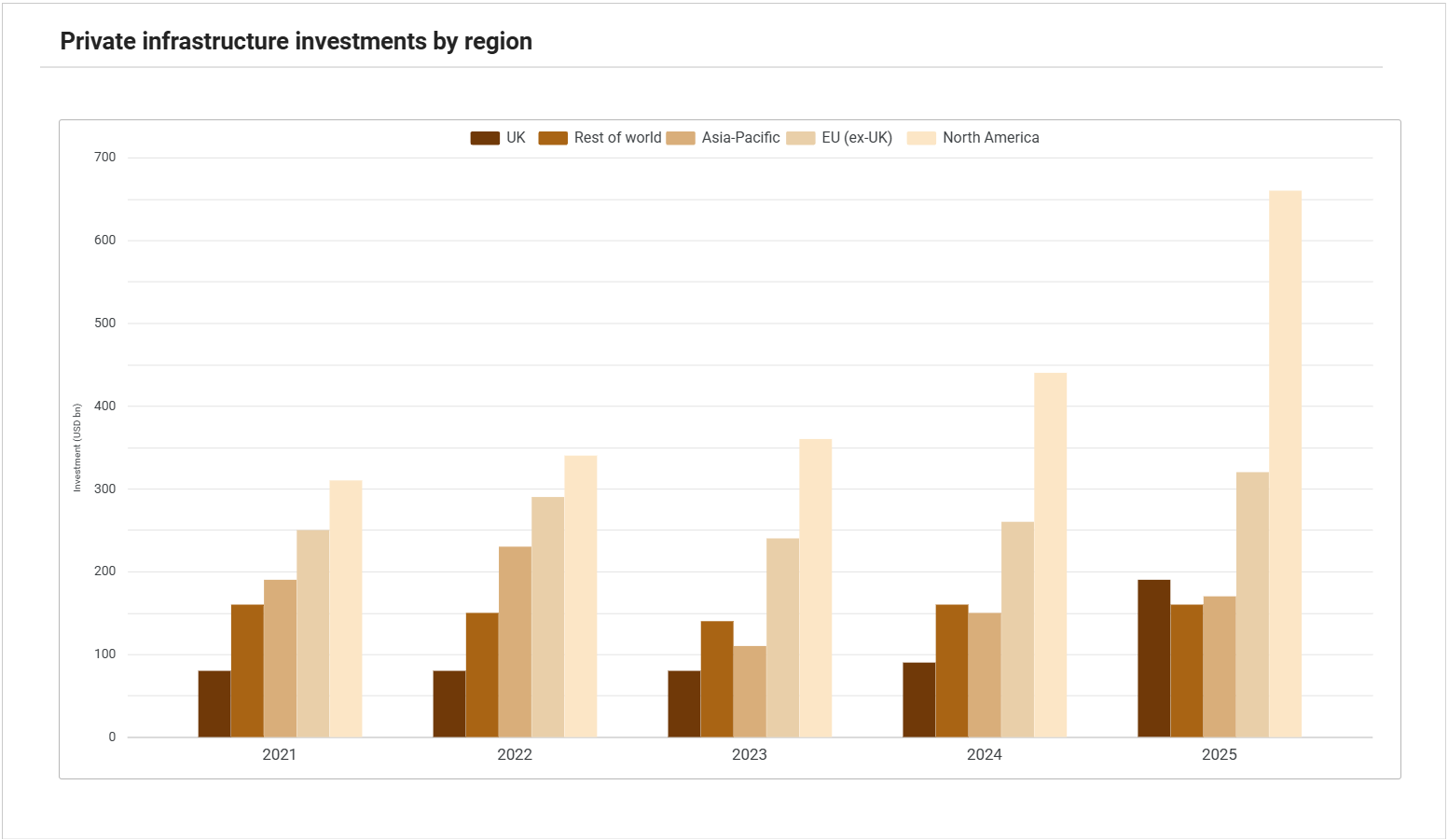

Global private infrastructure fundraising closed 2025 at nearly USD 300 billion, the highest level the asset class has ever seen. Capital is abundant. Conviction is high. And yet, if you zoom into where that capital actually went, the picture becomes more interesting, and far more useful, for anyone focused on European clean energy.

The North America effect (and why it matters to us)

Private infrastructure investments by region do not just show volume. There’s a drop of momentum hidden in the data.

North America dominated 2025 with a 50% year-over-year jump that stands out even against its own strong prior years. Digital infrastructure alone accounted for 26% of total deal flow. The AI-driven power supercycle pulled capital at a scale Europe has not matched, and the mechanism is worth paying attention to: a clear demand signal, federal policy alignment and hyperscaler capex commitments of over $600 billion pencilled in for 2026.

And when demand, policies and rising capex line up, markets move decisively.

Here is my reading of it: North America is not winning because it has better assets. It is winning because the narrative is coherent. Investors know what they are underwriting, what the exit looks like and roughly how long it takes. That coherence is what unlocks large-scale capital deployment. And it is precisely what Europe is still working to build.

The U.K. exception, and what it actually proves

Within Europe, one market stood apart. UK investments more than doubled in 2025. That number deserves unpacking, because it is not just about deal volume.

What the UK demonstrated is that a credible pipeline creates its own momentum. Infralogic counts 190 infrastructure assets due for exit from closed-end UK funds in the next four years. That backlog exists because the market has been consistent enough, for long enough, to generate it. Investors can model the entry, the hold period and the exit. That is an extraordinary advantage in an environment where extended exit timelines are one of the sector’s defining anxieties.

The contrast with continental Europe could not be starker.

The Antwerp Declaration Monitoring Report, that we analysed in our previous edition, found that 83% of the EU’s key competitiveness indicators are either stagnant or deteriorating. Public funding has increased (around €72 billion mobilised between 2021 and 2024) but Europe still faces an annual investment gap of roughly €406 billion to meet its 2030 targets. The EU’s Innovation Fund was oversubscribed by more than 500% in 2024. That is not a sign of weakness in intent. It is a sign of a structural bottleneck between available capital and investable conditions.

The European Commission adopted its Clean Energy Investment Strategy in March 2026, backed by more than €75 billion of EIB financing over the next three years. The ambition is real. But Bloomberg‘s reporting on the draft document puts the cost of the transition at €695 billion per year in the decade after 2030. There is a gap there that public financing alone will never close, which is precisely the point. T

The strategy is designed to de-risk projects so that private capital steps in at scale. Whether that sequencing actually holds is, in my view, the central question for European infrastructure dealmaking in the next two years.

The mid-market signal that most people are underreading

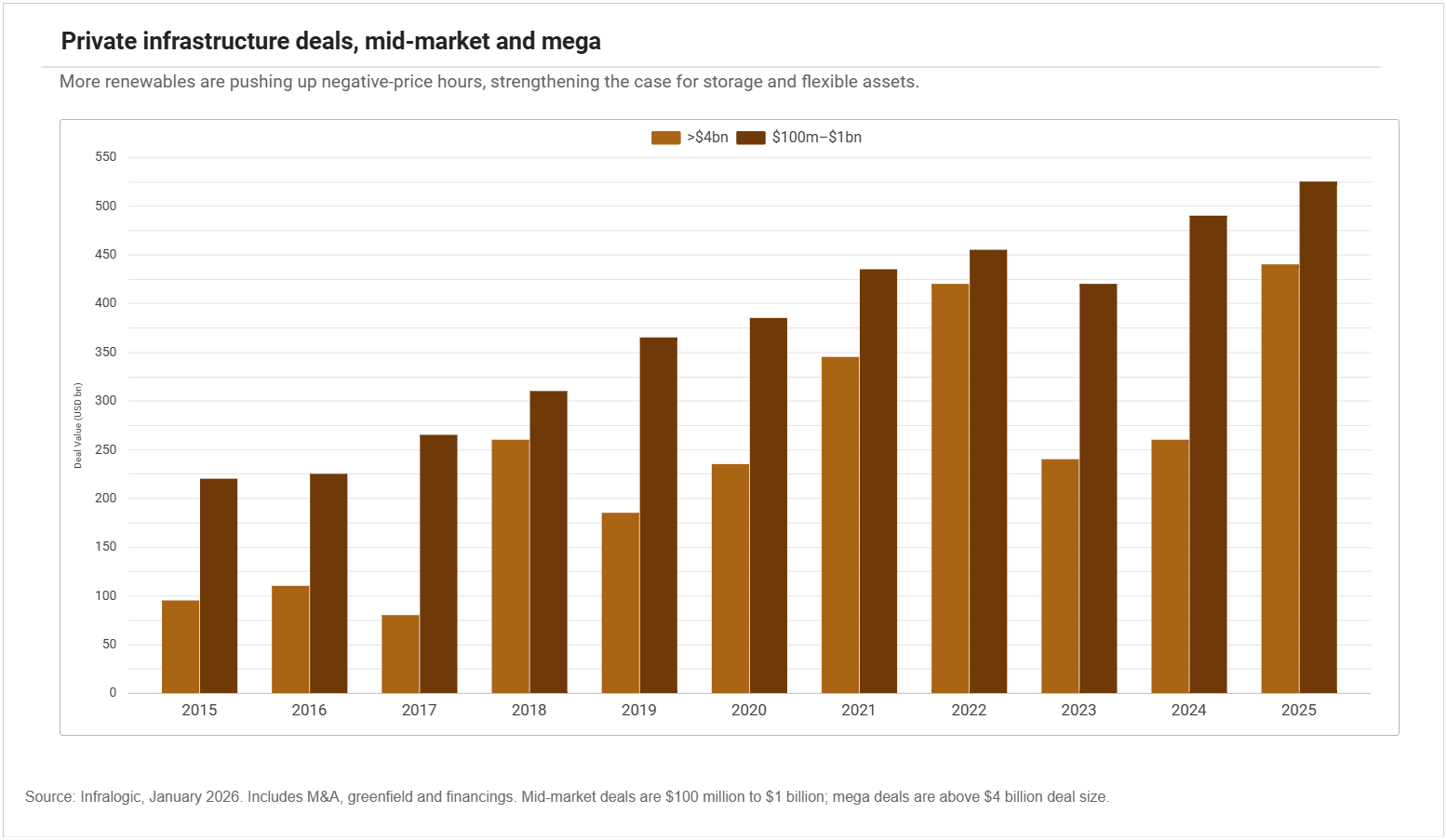

CBRE also bring a very important chart for anyone allocating or deploying capital in European clean energy right now.

From 2022 to 2024, mega deal activity fell sharply as macro uncertainty pushed financing costs higher and exit timelines stretched. Mid-market transactions (the USD 100 million to USD 1 billion range) rose by 8% over the same period. In 2025, mid-market volume reached a new peak. The divergence has been consistent and structural, not a temporary adjustment.

What I find most interesting here is not the volume. It is what that volume is made of.

Repowered onshore wind platforms. Contracted solar with storage. Hybrid projects combining generation and BESS on a shared grid connection. These are mid-market transactions. They are closing. And the reason they are closing, while mega deals stall, comes down to something that sounds almost boring until you think about what it means for valuation: exit optionality.

A €400 million contracted solar-plus-storage platform in Spain or Poland has multiple potential buyers. A strategic, a utility, an infrastructure fund, a secondaries vehicle. A €5 billion offshore wind megaproject requires a very specific type of buyer at a very specific moment in the market cycle. In a world where 21% of investors are now considering secondaries allocations (up from 9% the prior year) the mid-market is not a compromise. It is the rational choice.

The geopolitical layer that changes the calculus

One thing the CBRE report captures clearly, and that I think deserves more attention in the clean energy context specifically, is how the conflict in the Middle East is accelerating certain structural decisions in Europe.

The Strait of Hormuz facilitates roughly 20% of global crude oil and LNG shipments. Its effective closure is not just a transport problem. It is a reminder, arriving on top of the Russia-Ukraine precedent, that energy sovereignty is not a policy preference. It is an economic necessity. As the US reinforces its position as a petrostate and China accelerates as an electrostate, Europe is caught in the middle, and the policy choices made in 2026 will determine which path it takes.

This pressure does not automatically translate into faster clean energy deployment.

Grid bottlenecks, permitting delays and fragmented regulation are not resolved by geopolitical urgency alone. But it does change the political economy around infrastructure investment. It gives policymakers a more compelling argument to accelerate permitting reform, push grid investment and unlock private capital. Germany’s €500 billion fund for infrastructure, defence and climate is a signal that contracting demand in Europe will be larger for longer.

That is the kind of visibility infrastructure investors need.

What does all of this mean?

Infrastructure had a record year. North America captured most of the AI-driven upside. The UK built enough consistency to generate a pipeline. Continental Europe is still working on converting policy intent into investable conditions, but the pressure to do so has never been higher, from multiple directions simultaneously.

Within that context, European clean energy in 2026 is not a market in trouble. It is a market in transition to a new definition of value.

The deals that are closing are mid-market, contracted and flexible. They reduce system risk rather than simply adding capacity. They fit portfolios that need liquidity, not just exposure. And they are being done by managers who understood early that the premium was shifting, away from abstract green megawatts, and towards practical utility.

We saw data that has been signalling this for three years. The question now is whether the rest of the market catches up in 2026, or waits one more year.

Battery storage

- Bulgaria | GEN-I Invest seeks approval to acquire BESS operators VANKO-K-2008 and F Energy Solutions from Power Profit, expanding battery storage footprint

- Germany | Foresight Energy Infrastructure Partners II invests in battery storage developer Mirai Power, backing 12.5 GW BESS pipeline to support platform expansion

- United Kingdom | Capital Dynamics and Solo Renewables form £100m joint venture to develop 150 MW / 1,200 MWh long-duration energy storage project in Northern Ireland, supporting grid flexibility

- United Kingdom | Drax completes acquisition of flexible energy platform Flexitricity from Quinbrook, strengthening BESS optimisation and grid services capabilities

- United Kingdom | InfraVia acquires Mercia Power Response and Balance Power to form Supernova Power, creating integrated flexible power and 1.8 GW+ battery storage platform

Bio-fuels

- Croatia | Ancala’s Croatian Biomass Platform acquires three 5 MW biomass plants from The Sherif Group, doubling capacity and expanding national footprint through bolt-on growth

- France | INERATEC and TERTU form T.H2 joint venture to develop synthetic fuel plant in Normandy, advancing biomass-to-fuels production for aviation and industrial decarbonisation

Multiple

- Europe | Bankinter to sell 27.5% stake in investment arm to Plenium Partners, merging platforms to create €5.3bn multi-sector infrastructure and renewables investment manager

- Europe | EBRD invests additional €50m in Green Genius, increasing stake to support renewables expansion and battery storage pipeline across the Baltics

- Europe | Volue acquires scheduling and nomination platform dispoEnergy, expanding software offering for power and gas market participants across Europe

- Italy | Crédit Agricole Assurances acquires minority stake in Whysol Renewables from Whysol Investments, backing 1.2 GW renewables and BESS pipeline to support energy transition growth

- Lithuania | European Energy completes sale of 470 MW hybrid wind, solar and BESS Jonava project to Energix for up to €18.9m, advancing ready-to-build asset monetisation

Solar

- Ukraine | Kyivstar cleared to acquire six solar power plants exceeding 100 MW in Lviv region, expanding energy resilience strategy amid ongoing infrastructure challenges

- Ukraine | Scatec acquires remaining 40% stake in Ukrainian solar power plant from FMO for nominal €1, taking full ownership amid challenging market conditions

Wind

- Germany | European Energy sells 50% stake in 32.8 MW onshore wind project to QEEE fund, recycling capital while retaining construction and asset management roles

- Norway | Unitech acquires Source Galileo’s Norwegian offshore wind development unit, forming Nordrenergi to expand into BESS and offshore energy infrastructure

- Sweden | Aneo completes acquisition of RWE’s Swedish wind portfolio including 1.8 GW pipeline and 172 MW operational capacity, expanding Nordic renewables footprint

- United Kingdom | egg Power acquires Chirmorie onshore wind project in Scotland from Coriolis Energy and ESB, expanding UK renewables portfolio to meet rising data-driven energy demand